Car Sensors Market By Type (Temperature Sensors, Pressure Sensors, Motion Sensors, Speed Sensors, Gas Sensors), By Vehicle Type (Passenger Cars and Commercial Vehicles), By Application (Powertrain, Chassis, Exhaust, Security, Telematics, ADAS), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

48178

-

June 2024

-

300

-

-

This report was compiled by Kalyani Khudsange Kalyani Khudsange is a Research Analyst at Prudour Pvt. Ltd. with 2.5 years of experience in market research and a strong technical background in Chemical Engineering and manufacturing. Correspondence Sr. Research Analyst Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

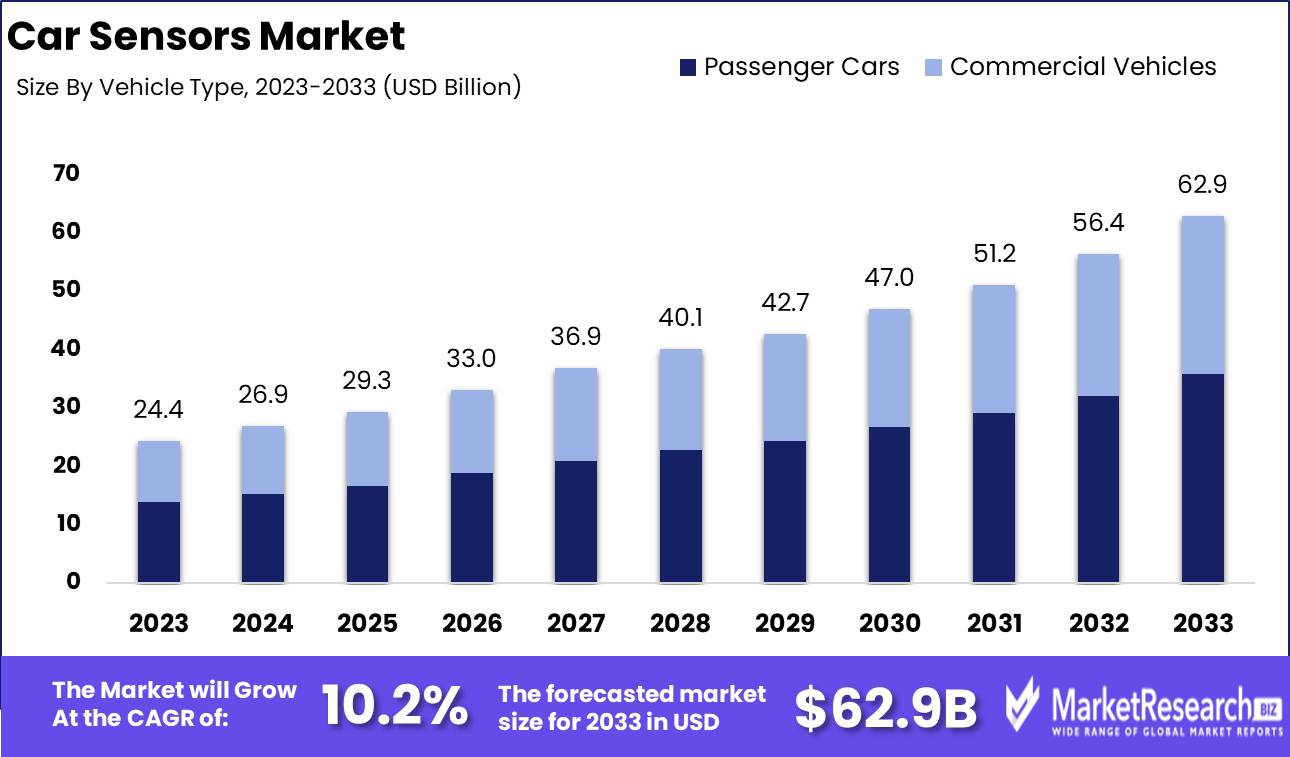

The Car Sensors Market was valued at USD 23.4 billion in 2023. It is expected to reach USD 62.9 billion by 2033, with a CAGR of 10.2% during the forecast period from 2024 to 2033.

The Car Sensors Market encompasses a wide range of sensor technologies used in automotive applications to enhance safety, efficiency, and performance. These sensors, including proximity, temperature, pressure, and motion sensors, are integral to advanced driver-assistance systems (ADAS), autonomous driving, and vehicle diagnostics. As vehicles become more sophisticated, the demand for innovative sensing solutions grows, driven by regulatory mandates for safety and emissions, consumer demand for enhanced driving experiences, and the automotive industry's shift towards electrification and automation.

The car sensors market is experiencing robust growth, driven by a confluence of technological advancements and stringent regulatory standards. Innovations in sensor technologies, particularly miniaturization and enhanced accuracy, are revolutionizing the automotive industry. These advancements are enabling the development of more sophisticated safety and driver-assistance systems, which are increasingly becoming standard in modern vehicles. The precision and reliability of these sensors are critical for the effective operation of advanced driver-assistance systems (ADAS) and autonomous driving technologies.

Furthermore, global regulatory bodies are imposing increasingly stringent emissions and safety regulations, compelling automakers to integrate advanced sensors to comply with these standards. This regulatory pressure is accelerating the adoption of cutting-edge sensor technologies across various vehicle segments.

Despite these advancements, the initial high costs of advanced sensors present a significant barrier to widespread adoption, particularly in cost-sensitive markets. However, continuous investment in research and development is essential to overcoming this challenge. Leading market players are focusing on reducing production costs while enhancing the functionality and performance of their sensor offerings. This ongoing innovation is expected to drive down costs over time, making advanced sensors more accessible to a broader range of automotive manufacturers.

Key Takeaways

- Market Growth: The Car Sensors Market was valued at USD 23.4 billion in 2023. It is expected to reach USD 62.9 billion by 2033, with a CAGR of 10.2% during the forecast period from 2024 to 2033.

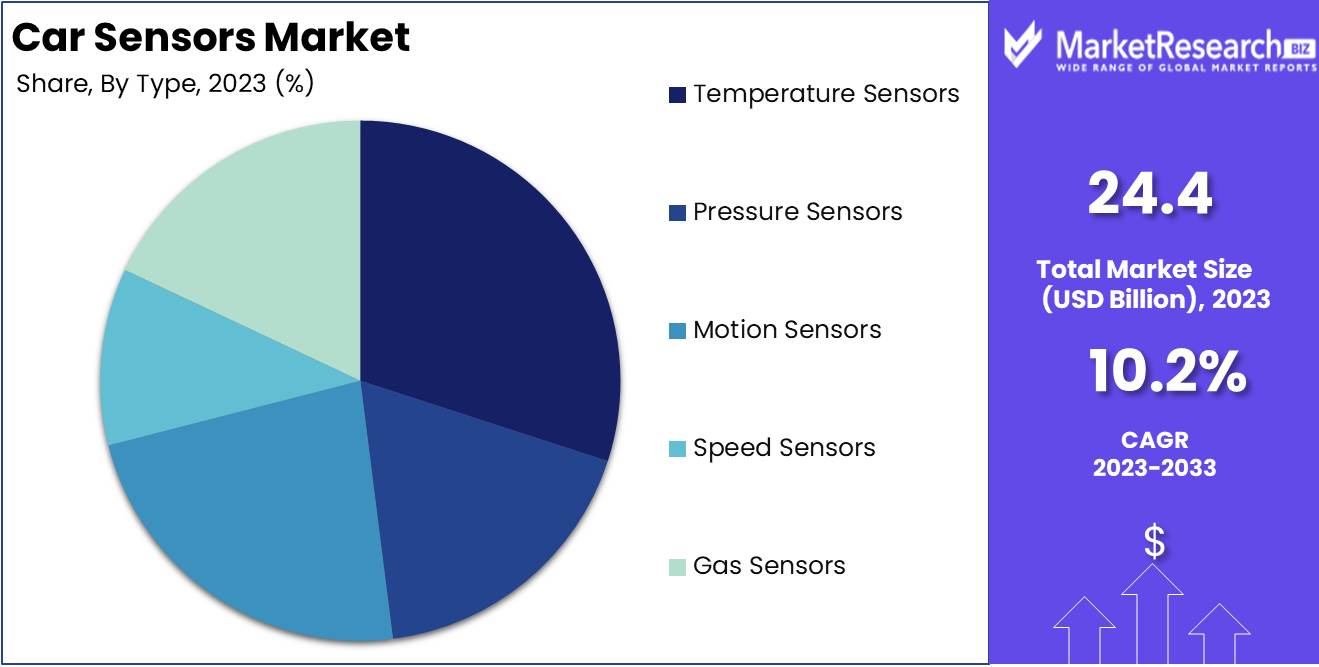

- By Type: Temperature Sensors dominated the Car Sensors Market by type.

- By Vehicle Type: Passenger Cars dominated the Car Sensors Market by vehicle type.

- By Application: Powertrain dominated due to enhanced vehicle performance and fuel efficiency.

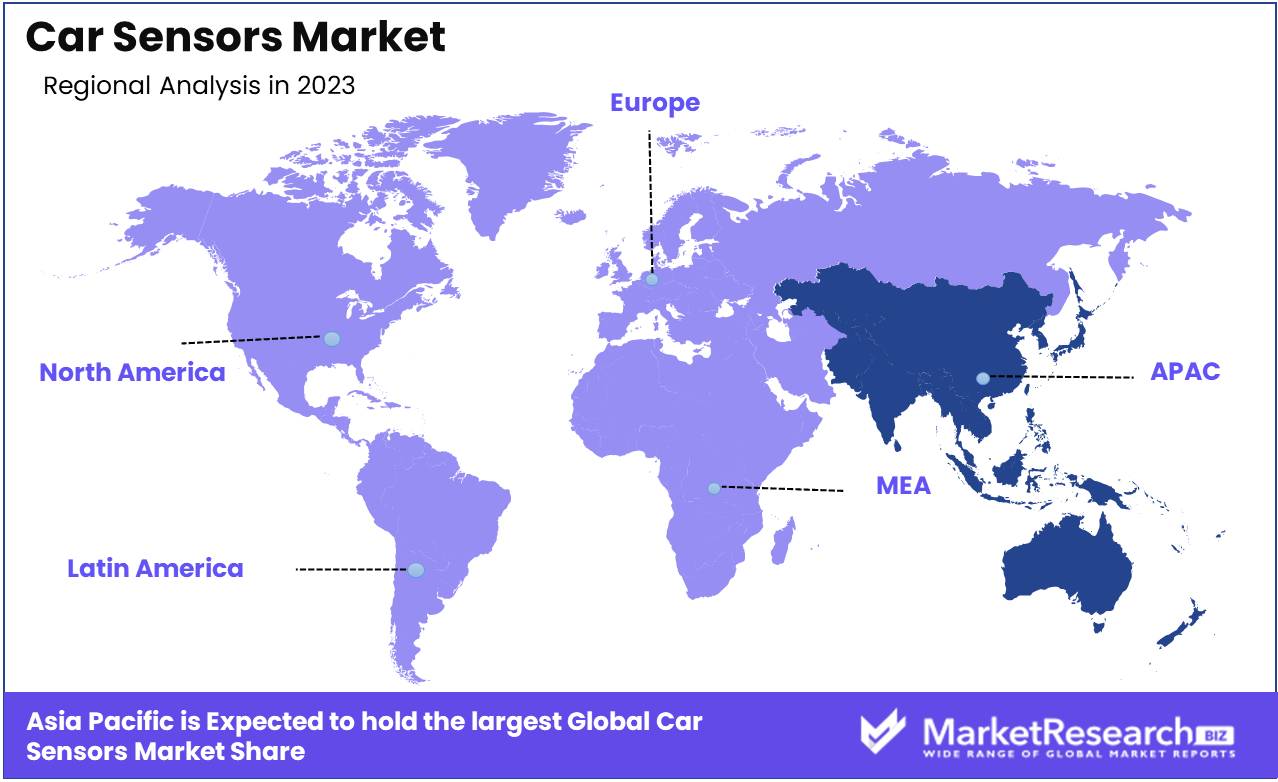

- Regional Dominance: The Asia Pacific region dominates the global car sensors market with a 40% largest market share.

- Growth Opportunity: The global car sensors market growth is driven by sensor fusion, integration advancements, and increasing IoT connectivity adoption.

Driving factors

Consumer Shift Towards Alternative Fuel Vehicles Enhances Demand for Advanced Car Sensors

The growing consumer inclination toward alternative fuel vehicles (AFVs), driven by the need to reduce greenhouse gas emissions, is significantly bolstering the car sensors market. AFVs, which include electric vehicles (EVs) and hybrid vehicles, require sophisticated sensor systems to manage and optimize battery performance, energy consumption, and overall vehicle efficiency. As governments worldwide implement stricter emissions regulations and offer incentives for the adoption of AFVs, the demand for high-quality, precise sensors is increasing. According to a report the market for electric vehicles alone is projected to grow at a CAGR of 21.7% from 2023 to 2030, highlighting a substantial opportunity for car sensor manufacturers to cater to this expanding segment.

Enhanced Vehicle Safety and Comfort Drive Sensor Innovation

The rising focus on vehicle safety and comfort features is a pivotal driver for the car sensors market. Modern vehicles are increasingly equipped with advanced driver-assistance systems (ADAS), which rely heavily on sensors such as radar, lidar sensors, ultrasonic sensors, and cameras to ensure functionalities like collision avoidance, lane-keeping assistance, and adaptive cruise control. Additionally, comfort features like automatic climate control, seat adjustments, and infotainment systems also depend on a variety of sensors. The global ADAS market, valued at approximately USD 24.3 billion in 2021, is expected to grow at a CAGR of 11.9% from 2022 to 2030, underscoring the expanding role of sensors in enhancing vehicle safety and passenger comfort.

A surge in Vehicle Production and Sales in Emerging Economies Fuels Sensor Market Expansion

Increasing vehicle production and sales, particularly in emerging economies, are significantly propelling the car sensors market. Countries such as China, India, and Brazil are witnessing robust growth in automobile manufacturing and sales due to rising income levels, urbanization, and improving infrastructure. In 2022, China's vehicle production reached 26 million units, accounting for nearly 30% of global vehicle production. This surge necessitates the integration of various sensors to meet both regulatory standards and consumer expectations for safety, efficiency, and enhanced driving experience. As these economies continue to grow, the automotive industry's expansion will inevitably lead to greater adoption of sophisticated sensor technologies, thereby driving market growth.

Restraining Factors

Increasing Demand for Advanced Driver Assistance Systems (ADAS): A Double-Edged Sword

The increasing demand for Advanced Driver Assistance Systems (ADAS) is a significant driver of innovation and growth in the car sensors market. ADAS technology relies heavily on a variety of sensors to function effectively, including radar, lidar, ultrasonic, and camera-based systems. These sensors enhance vehicle safety and driver convenience by enabling features such as adaptive cruise control, lane-keeping assistance, automatic emergency braking, and parking assistance.

However, while the demand for ADAS drives the need for advanced sensor technologies, it also introduces several restraining factors that impact market growth. One primary challenge is the high cost associated with developing and integrating these sophisticated sensor systems into vehicles. Manufacturers must invest heavily in research and development to meet the performance and reliability standards required for ADAS applications, which can limit the scalability of production and increase the overall cost of vehicles. This cost barrier can slow market penetration, particularly in price-sensitive regions.

Moreover, the complexity of ADAS systems necessitates rigorous testing and validation to ensure safety and compliance with regulatory standards. This requirement can lead to longer development cycles and delays in bringing new sensor technologies to market.

Autonomous Driving Technology: Catalyzing Market Growth Amidst Technical and Regulatory Hurdles

Autonomous driving technology represents a transformative force in the automotive industry, with the potential to revolutionize transportation by enhancing safety, reducing traffic congestion, and improving mobility. The development of fully autonomous vehicles relies on an extensive array of sensors, including lidar, radar, cameras, and ultrasonic sensors, to provide the necessary data for real-time decision-making and navigation.

The push towards autonomous driving has accelerated advancements in sensor technologies, thereby expanding the car sensors market. Companies are investing heavily in improving sensor accuracy, range, and reliability to meet the stringent demands of autonomous vehicle operation. As a result, the market has seen significant innovation and increased demand for high-performance sensors.

Despite these positive impacts, several restraining factors influence the growth of the car sensors market in the context of autonomous driving. One major challenge is the high cost of autonomous vehicle sensors, particularly lidar systems, which remain prohibitively expensive for mass-market adoption. This cost issue is compounded by the need for multiple redundant sensors to ensure safety and reliability, further driving up the overall expense of autonomous vehicles.

By Type Analysis

In 2023, Temperature Sensors dominated the Car Sensors Market by type.

In 2023, Temperature Sensors held a dominant market position in the "By Type" segment of the Car Sensors Market. Temperature Sensors led the market due to their critical role in maintaining optimal engine performance and enhancing vehicle safety by monitoring various temperature levels within the vehicle system. Their integration into battery management systems in electric vehicles further solidified their market leadership.

Pressure Sensors ranked second, essential for applications such as monitoring tire pressure, fuel system pressure, and engine oil pressure. Their contribution to safety and efficiency made them indispensable in modern vehicles.

Motion Sensors, positioned third, are pivotal in advanced driver-assistance systems (ADAS) and autonomous driving technologies. They detect and measure vehicle movement, contributing to enhanced navigation and safety features.

Speed Sensors, closely following, are vital for transmission control, anti-lock braking systems (ABS), and electronic stability control (ESC). Their role in ensuring vehicle stability and performance consistency is crucial.

Gas Sensors, although smaller in market share, are increasingly important due to stringent emission regulations. They monitor exhaust gases to ensure compliance with environmental standards, thus contributing to reduced vehicle emissions.

By Vehicle Type Analysis

In 2023, Passenger Cars dominated Car Sensors Market by vehicle type.

In 2023, Passenger Cars held a dominant market position in the by-vehicle type segment of the Car Sensors Market. This preeminence is primarily attributed to the burgeoning demand for advanced driver-assistance systems (ADAS) and increasing consumer preference for enhanced safety features and in-car connectivity. Passenger cars, equipped with sophisticated sensor technologies, account for the largest share due to the escalating production volumes and the continuous advancements in sensor integration.

Conversely, Commercial Vehicles also contribute significantly to the market, albeit at a smaller scale compared to passenger cars. The adoption of car sensors in commercial vehicles is driven by the need for improved fleet management, safety, and efficiency. Innovations in telematics and the integration of sensors for predictive maintenance are pivotal in this sector, fostering operational cost reductions and enhancing vehicle longevity. While the market for sensors in commercial vehicles is expanding steadily, the rate of adoption is moderated by higher implementation costs and longer replacement cycles compared to passenger cars.

By Application Analysis

In 2023, Powertrain dominated due to enhanced vehicle performance and fuel efficiency.

In 2023, Powertrain held a dominant market position in the By Application segment of the Car Sensors Market. The Powertrain segment’s dominance is driven by increasing demand for enhanced vehicle performance and fuel efficiency. Car sensors in this segment are critical for monitoring and optimizing engine performance, fuel consumption, and transmission efficiency. As automakers strive to meet stringent emission regulations and consumer demand for high-performance vehicles, the integration of advanced powertrain sensors becomes essential. These sensors provide real-time data, allowing for precise control and adjustment of the engine and transmission systems, leading to better fuel economy and reduced emissions.

Chassis sensors are integral for vehicle stability and control, directly impacting ride quality and safety. These sensors monitor and manage systems such as anti-lock braking, electronic stability control, and suspension systems, ensuring a balanced and secure driving experience. Exhaust sensors, particularly oxygen sensors, play a vital role in emission control by ensuring the optimal air-fuel mixture. This helps in reducing harmful emissions and improving overall engine efficiency, which is critical for compliance with environmental regulations.

Security sensors, including those for theft prevention and collision detection, are increasingly in demand due to rising concerns over vehicle safety. These sensors enhance vehicle security by providing real-time monitoring and alerts. Telematics sensors facilitate connectivity and communication within the vehicle, supporting navigation, vehicle tracking, and infotainment systems. The growing consumer preference for connected cars drives the adoption of telematics sensors.

Advanced Driver Assistance Systems (ADAS) rely heavily on an array of sensors, including radar, lidar, and cameras, to enhance driving safety and convenience. These sensors enable features such as adaptive cruise control, lane-keeping assistance, and automatic emergency braking, contributing to the increasing adoption of ADAS in modern vehicles.

Key Market Segments

By Type

- Temperature Sensors

- Pressure Sensors

- Motion Sensors

- Speed Sensors

- Gas Sensors

By Vehicle Type

- Passenger Cars

- Commercial Vehicles

By Application

- Powertrain

- Chassis

- Exhaust

- Security

- Telematics

- ADAS

Growth Opportunity

Sensor Fusion and Integration

The rapid evolution of sensor fusion and integration technologies presents a significant growth opportunity in the global car sensors market. Sensor fusion combines data from multiple sensors to improve the accuracy and reliability of information, which is critical for advanced driver-assistance systems (ADAS) and autonomous vehicles. This integration enhances vehicle safety, navigation, and performance by providing a comprehensive view of the car's surroundings. The demand for integrated sensor systems is expected to surge, driven by the automotive industry's push towards higher levels of automation and enhanced safety standards. Automakers and suppliers investing in sensor fusion technologies are well-positioned to capitalize on this trend, as they can offer more sophisticated and reliable systems to OEMs and consumers.

Connectivity and Internet of Things (IoT)

The convergence of car sensors with IoT technology is another key driver of market growth. IoT-enabled car sensors facilitate real-time data exchange between vehicles, infrastructure, and cloud-based systems, fostering the development of smart transportation ecosystems. This connectivity supports various applications, including predictive maintenance, remote diagnostics, and enhanced infotainment services, which improve the overall driving experience and operational efficiency. With the growing adoption of 5G networks, the potential for IoT in automotive sensors will expand, enabling faster and more reliable communication. Companies that leverage IoT for innovative sensor solutions will gain a competitive edge by offering enhanced functionalities and seamless integration with broader smart city initiatives.

Latest Trends

Advancements in Sensor Technologies

The car sensors market is poised for significant growth, driven by notable advancements in sensor technologies. Innovations in miniaturization, improved accuracy, and enhanced connectivity are transforming automotive sensors, enabling more sophisticated applications. LiDAR, radar, and ultrasonic sensors are becoming more reliable and cost-effective, providing critical data for vehicle systems. Additionally, advancements in artificial intelligence and machine learning are optimizing sensor data processing, leading to improved decision-making and predictive maintenance capabilities. These technological strides are essential for supporting the evolving needs of modern vehicles, particularly in safety, efficiency, and user experience.

Rising Demand for Autonomous and Electric Vehicles

The increasing adoption of autonomous and electric vehicles is a key driver for the car sensors market. Autonomous vehicles (AVs) rely heavily on an array of sensors to navigate and make real-time decisions. The need for precise environmental mapping and obstacle detection has accelerated the development of advanced sensors such as high-resolution cameras, LiDAR, and radar systems. Concurrently, the electric vehicle (EV) market is expanding rapidly, with sensors playing a crucial role in battery management systems, energy efficiency, and safety features. The integration of these sensors ensures optimal performance and longevity of EV components, thereby enhancing overall vehicle reliability.

Regional Analysis

The Asia Pacific region dominates the global car sensors market with 40% largest market share.

The global car sensors market demonstrates varied growth trajectories across different regions, driven by distinct economic, technological, and regulatory factors. North America leads with a substantial market share, underpinned by high automotive production and a strong emphasis on advanced driver-assistance systems (ADAS). The region boasts robust R&D investments, with the U.S. contributing significantly through its extensive automotive sector.

Europe follows closely, driven by stringent safety regulations and the presence of major automotive manufacturers in countries like Germany and the UK. The European car sensors market is bolstered by the EU's regulatory framework promoting vehicular safety and environmental sustainability.

Asia Pacific emerges as the fastest-growing and dominating region, accounting for approximately 40% of the global market share. This is attributed to the rapid expansion of the automotive industry in countries such as China, Japan, and South Korea. China's dominance in electric vehicle (EV) production and adoption further accelerates sensor demand, supported by government initiatives and favorable policies.

Latin America and the Middle East & Africa exhibit moderate growth, driven by increasing automotive sales and gradual economic improvements. Brazil and Mexico are key contributors in Latin America, while the UAE and South Africa lead in the Middle East & Africa, leveraging investments in smart infrastructure and connected vehicles.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

The global car sensors market in 2024 is poised for substantial growth, driven by advancements in autonomous driving, stringent safety regulations, and the increasing integration of sophisticated electronics in vehicles. Key players in this market, such as Robert Bosch GmbH and DENSO Corporation, continue to dominate through extensive R&D investments and diversified product portfolios. Bosch, leveraging its strong market presence and technological innovations, is expected to maintain its leadership position. DENSO, with its robust focus on automotive electronics, remains a critical player, driving innovation in sensor technology.

Infineon Technologies AG and NXP Semiconductors are anticipated to expand their influence by leveraging their expertise in semiconductor solutions, essential for developing advanced driver-assistance systems (ADAS) and electric vehicles (EVs). STMicroelectronics, known for its sensor solutions, is likely to capitalize on the increasing demand for integrated circuits and MEMS technology.

Valeo and Continental AG are also significant contributors, benefiting from their strategic partnerships and comprehensive sensor offerings that support the automotive industry's shift toward automation and electrification. Sensata Technologies and Delphi Automotive are enhancing their market positions by focusing on sensor integration and system-level solutions.

Texas Instruments and ELMOS Semiconductor SE are expected to leverage their semiconductor prowess to meet the evolving requirements of automotive sensors, contributing to the market's competitive landscape. Overall, the continuous innovation and strategic collaborations among these key players are set to drive the global car sensors market's dynamic growth and technological evolution.

Market Key Players

- Robert Bosch GmbH

- DENSO Corporation

- Infineon Technologies AG

- NXP Semiconductor

- ST Microelectronics

- Valeo

- Continental AG

- Sensata Technologies

- Delphi Automotive Company

- Texas Instruments Incorporated

- ELMOS Semiconductor SE

- Other Key Players

Recent Development

- In April 2024, Bosch unveiled a new suite of advanced sensors designed specifically for autonomous vehicles. These sensors include state-of-the-art LiDAR, radar, and camera systems, providing higher resolution and greater range. This development is expected to significantly enhance the safety and reliability of autonomous driving systems.

- In February 2024, Continental introduced a smart brake sensor system to improve vehicle safety. This system features real-time monitoring and predictive maintenance capabilities, enabling early detection of brake wear and potential failures. The innovation enhances vehicle safety and reduces maintenance costs for fleet operators.

- In January 2024, Texas Instruments launched new semiconductors to enhance automobiles' intelligence and safety. Notably, the AWR2544 77GHz mm-wave radar sensor chip is designed for satellite radar architectures, improving sensor integration and ADAS decision-making. This advancement is showcased at the Consumer Electronics Show (CES) in the U.S..

Report Scope

Report Features Description Market Value (2023) USD 23.4 Billion Forecast Revenue (2033) USD 62.9 Billion CAGR (2024-2032) 10.2% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Type (Temperature Sensors, Pressure Sensors, Motion Sensors, Speed Sensors, Gas Sensors), By Vehicle Type (Passenger Cars and Commercial Vehicles), By Application (Powertrain, Chassis, Exhaust, Security, Telematics, ADAS) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Robert Bosch GmbH, DENSO Corporation, Infineon Technologies AG, NXP Semiconductor, ST Microelectronics, Valeo, Continental AG, Sensata Technologies, Delphi Automotive Company, Texas Instruments Incorporated, ELMOS Semiconductor SE, Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Robert Bosch GmbH

- DENSO Corporation

- Infineon Technologies AG

- NXP Semiconductor

- ST Microelectronics

- Valeo

- Continental AG

- Sensata Technologies

- Delphi Automotive Company

- Texas Instruments Incorporated

- ELMOS Semiconductor SE

- Other Key Players

Our Clients

View Our Licence Options