Global Bakery Packaging Market By Product Type(Bread, Cakes, , Biscuits, Breakfast cereals, Frozen bakery, Frozen desserts), By Type of Material(Flexibles, Rigid plastic, Metal),By Packaging Technique(Modified atmosphere packaging, Vacuum packaging, Flushing with inert gas, Gas Packaging, Active Packaging)By End User, By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends And Forecast 2023-2032

-

11026

-

May 2023

-

185

-

-

This report was compiled by Kalyani Khudsange Kalyani Khudsange is a Research Analyst at Prudour Pvt. Ltd. with 2.5 years of experience in market research and a strong technical background in Chemical Engineering and manufacturing. Correspondence Sr. Research Analyst Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

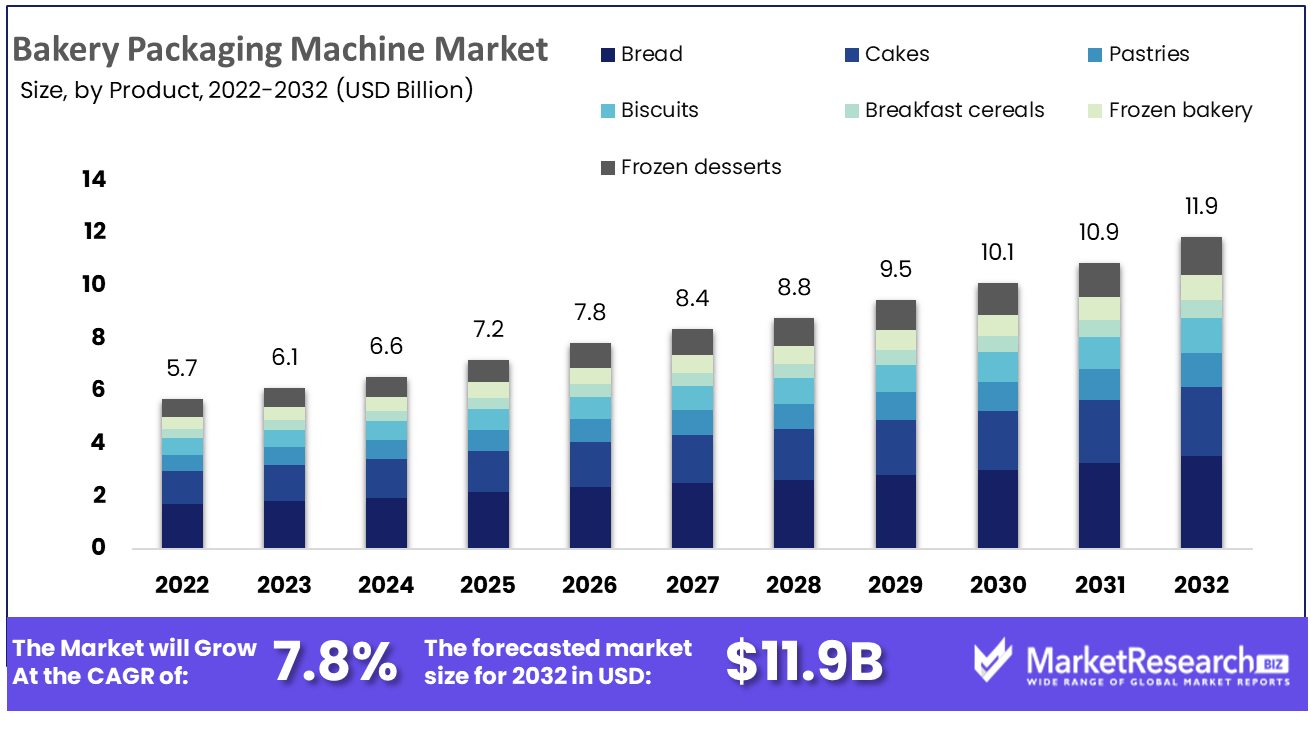

The Bakery Packaging Machine Market was estimated at USD 5.7 billion in 2022 and is expected to reach USD 11.9 billion by 2032, growing with a CAGR of 7.8% during the forecast period 2023 to 2032.

Consumer dietary choices and the growing demand for convenience foods are the main driving factors for the market expansion. Additionally, there has been a substantial change toward processed, packaged, and readymade baked products due to the upsurge in consumer expenses, enhancing living standards, and growth in urbanization. For example, In North America, doughnuts are considered the most preferred food at any time and it is generally eaten as a meal alternative, whereas cakes are consumed as tea snacks.

Bread is considered an anytime food due to its high intake among consumers. The bread market is estimated to be growing at a demand of around 9% P.A in the volume terms. Earlier, the bread was packed in a waxed paper wrapper, whereas now the packing system has been advanced and is packed in plastic films such as LDPE, LLDPE-LDPE, and PP.

A lot of studies and innovations are taking place in the bakery packaging market. For example, the Italian Journal of Food Safety did a research analysis about various bread packing strategies which included modified atmosphere packaging (MAP), active packaging (AP), intelligent packaging (IP), biosensors, and Nano packaging. Among these, MAP and active packaging are the most effective packing strategies, due to the long-term advantages in delaying fungal contamination. Moreover, bread packaging has been receiving a lot of attention in terms of production aspects which leads to the increase of consumers as well as the growth in market expansion.

Furthermore, technological advancement has expanded beyond accuracy and design, as bakery manufacturers are now getting into sustainability and automation. The new emerging trend in the market to attain sustainable packaging materials is paper packaging solutions. Likewise, Automation plays a significant role in the packaging prospect by including dry ingredient packaging which will become a norm. As technology is advancing to improve seal integrity, such as through ultrasonic and three-sided seal packaging, the demand for manual supervision diminishes, allowing workers to be directed toward other production areas.

Due to the Russia and Ukraine war impact, the bakery packaging industry has witnessed a significant impact in terms of the supply of raw materials and ingredients. Russia and Ukraine are the major producers of wheat, maize, and barley. The war has adversely affected the import and export of these important ingredients which has led to rising expenses as well as the bakery production.

Driving Factors

Packaging Film Properties Drive Bakery Packaging Market Growth

The properties of packaging films are of significant importance in driving the bakery packaging market's growth. Innovations in film technology that improve barrier properties, extend shelf life, and enhance product freshness are critical for bakery items. These films are designed to be heat-sealable, durable, and often transparent, allowing consumers to view the product within, which can be a significant climatic factor in the purchasing decision.

Advancements in biodegradable and recyclable films also cater to the increasing consumer demand for sustainability. The ability of these films to maintain the integrity and freshness of bakery goods while also reducing environmental impact is a substantial selling point. As manufacturers continue to develop films with better mechanical properties, such as puncture resistance and flexibility, along with improved environmental profiles, the market for bakery packaging is expected to expand. In the long term, these advancements in film properties could become industry standards, given the rising consumer and regulatory demands for sustainability.

Retail Revolution Sparks Bakery Packaging Demand

The rise in sales of patisserie and bakery items through retail outlets is a significant catalyst for growth in the bakery packaging market. The convenience of purchasing high-quality bakery products from retail outlets has led to an increase in demand for packaging solutions that are both protective and attractive. Retailers are seeking innovative packaging that preserves the freshness of the products while also enabling ease of transport and display.

As retail chains expand and the number of specialty bakery stores within supermarkets grows, the need for distinct packaging that can enhance brand recognition and product differentiation becomes more pronounced. This retail shift is pushing packaging companies to create designs that can stand out in competitive shelf space and appeal to the consumer's eye. The continued growth in sales of retail bakeries is anticipated to have a lasting impact on the packaging market, as brands compete not only on product quality but also on the visual appeal and convenience of their packaging.

Sustainable Solutions Revolutionize Bakery Packaging

The industry development of resourceful alternatives in bakery packaging materials is driving market growth by meeting the demand for sustainability. Consumers and regulators are increasingly aware of the environmental impact of packaging waste, pushing for eco-friendly options. Packaging made from plant-based polymers, recycled materials, and those that are biodegradable or compostable are gaining traction in the market.

The integration of these resourceful materials must be balanced with the functional requirements of bakery packaging, such as moisture control, durability, and food safety. Manufacturers that innovate in creating sustainable packaging without compromising on these essential properties are poised for growth. The long-term implications include a potential shift in industry standards towards more sustainable practices, and packaging innovations that could redefine product offerings in the bakery sector.

Restraining Factors

Environmental Concerns Restrain Bakery Packaging Market Growth

The bakery packaging market faces considerable restraint due to increasing environmental concerns. Packaging materials traditionally used in the bakery sector often include plastics and non-biodegradable elements which contribute to pollution and are subject to scrutiny by regulatory bodies and environmental groups. The rising demand for sustainable packaging solutions that minimize ecological footprints is a challenge that traditional bakery packaging must adapt to. The pressure to innovate towards eco-friendliness can result in increased costs and operational complexities, potentially slowing market growth as manufacturers struggle to balance sustainability with functionality and cost.

Limited Shelf Life of Bakery Products Restrains Market Growth

The limited shelf life of bakery products presents a significant challenge to the packaging market. Packaging must not only protect the product from environmental factors that hasten spoilage but also appeal to consumers' growing preference for freshness and minimal preservatives. The need for advanced packaging technologies that extend shelf life, such as modified atmosphere packaging or active packaging, often comes with higher costs and technological barriers. These requirements constrain the market as packaging solutions must continually evolve to meet these dual demands, which can be particularly difficult for smaller players with limited R&D capabilities.

By Product Type

Bread, as a staple food, holds the largest share of the bakery packaging market due to its widespread consumption across various demographics and cultures. The packaging of bread requires maintaining its freshness and preventing microbial growth, which drives the demand for advanced packaging solutions. Innovations in packaging technology that extend shelf life without the use of preservatives are key growth drivers for this segment.

The other sub-segments, while not as dominant, play a significant role in the market. Cakes and pastries require protective packaging to maintain their aesthetic and structural integrity, driving demand for custom packaging solutions. Biscuits and breakfast cereals leverage packaging for branding and convenience with resealable options. The frozen bakery and frozen dessert segments are expanding due to the rising demand for bakery products and convenience foods, requiring durable and moisture-resistant packaging.

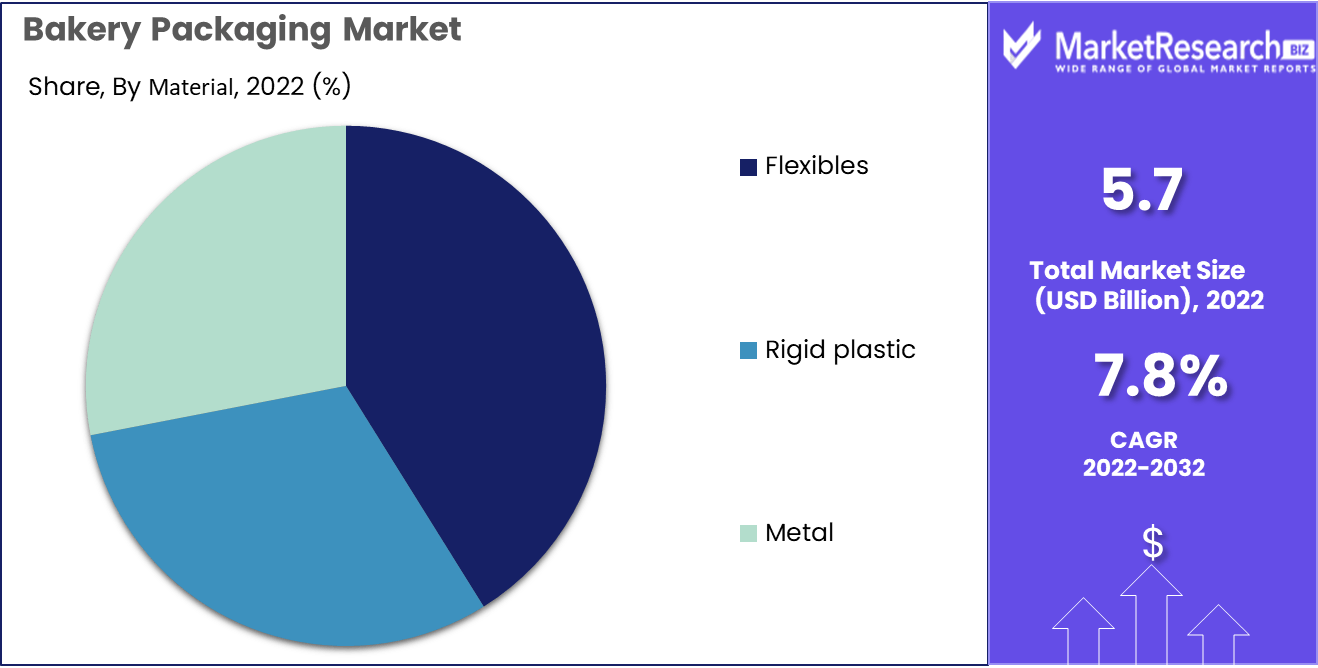

By Type of Material

Flexible materials are the cornerstone of the bakery packaging market, favored for their versatility, lightweight, and cost-effectiveness. They adapt easily to various shapes and sizes, providing efficient barriers against contaminants and extending the product’s shelf life. The rise of bio-based and biodegradable flexible materials aligns with the increasing environmental sustainability Industry Trend.

Rigid plastics offer durability and are often used where a firm structure is needed, such as for cakes and delicate pastries. Metal, less common in bakery packaging, is typically reserved for long shelf life products or premium packaging due to its strength and barrier properties.

By Packaging Technique

Modified atmosphere packaging (MAP) is the leading technique in bakery packaging, enhancing the shelf life of baked goods by altering the internal atmosphere of the packaging. This method is integral for bread and other bakery products that are sensitive to spoilage. MAP's ability to significantly prolong freshness while maintaining product quality has made it a staple in the industry.

Vacuum packaging is utilized to remove air and protect products from oxidation and spoilage. Inert gas flushing is often used in conjunction with MAP for products that are sensitive to crushing. Gas packaging uses specific gas mixtures to inhibit microbial growth, while active packaging incorporates components that actively maintain or extend the product's shelf life. These techniques are essential for catering to diverse product needs and enhancing the appeal of bakery items.

The bakery packaging market is driven by the need to maintain product freshness, extend shelf life, and meet consumer demands for convenience and sustainability. Dominant sub-segments have evolved in response to these Major factors, with each contributing to the overall growth of the market through innovations and adaptability to changing consumer preferences.

Key Market Segments

By Product Type

- Bread

- Cakes

- Pastries

- Biscuits

- Breakfast cereals

- Frozen bakery

- Frozen desserts

By Type of Material

- Flexibles

- Rigid plastic

- Metal

By Packaging Technique

- Modified atmosphere packaging

- Vacuum packaging

- Flushing with inert gas

- Gas Packaging

- Active Packaging

Growth Opportunities

Eco-Friendly Packaging Materials Offer Growth Opportunity

The shift toward eco-friendly packaging materials is a major driver of growth in the bakery packaging market. As consumers become more environmentally conscious, there's a rising preference for sustainable solutions. Data indicates that eco-friendly packaging is not just a trend but a growing expectation. Bakery businesses adopting biodegradable, recyclable, or compostable materials can differentiate themselves and potentially command premium pricing, broadening market reach and fostering customer loyalty.

Emerging Markets Present Expansive Opportunities for Bakery Packaging

Tapping into emerging markets offers significant growth prospects for the bakery packaging industry. These markets are characterized by rapidly growing middle-class populations with increasing disposable incomes and a growing inclination toward convenience foods, including baked goods. The expansion into these markets, where urbanization and changing lifestyles drive the demand for glass packaging foods, can result in a substantial increase in the volume of bakery packaging required, thus expanding the market footprint.

Advances in Packaging Technology Propel Market Growth

Technological advancements in packaging are key to the evolution and expansion of the bakery packaging market. Innovations such as improved barrier properties, enhanced sealing techniques, and smart packaging that extend shelf life are critical in meeting the demands for freshness and quality. The global smart packaging market size is expected to reach $26.7 billion by 2024, indicating a growing intersection between technology and packaging, which can be leveraged for market growth.

Flexible and Transparent Packaging Innovation Opens New Market Avenues

The increasing use of flexible and transparent packaging, as well as innovations in bioplastics, are carving new opportunities in the bakery packaging sector. Transparency in packaging allows visual quality assurance for consumers, while flexibility can offer convenience in transport and display. The global flexible packaging market is expected to grow from $160.8 billion in 2020 to $200.5 billion by 2025, reflecting consumer preferences that could drive similar trends in bakery packaging, thus expanding market potential.

Regional analysis

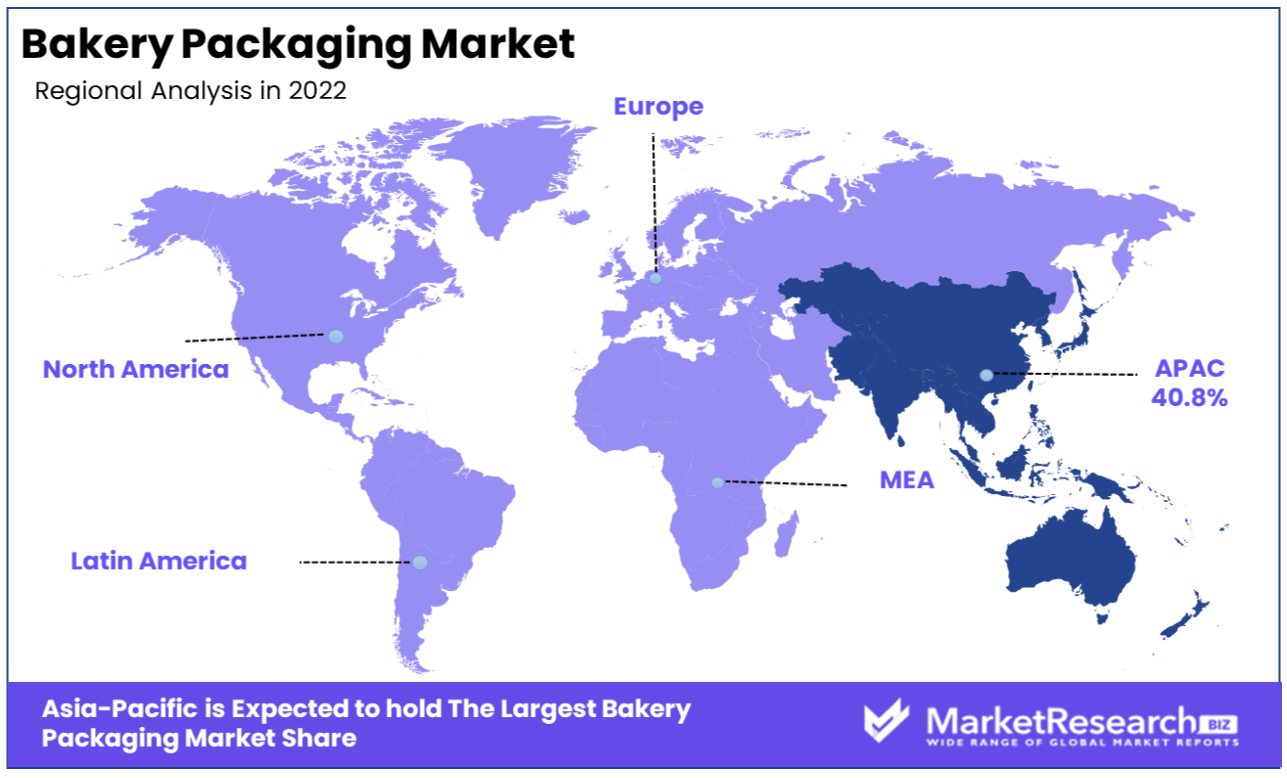

Asia Pacific Dominates with 40.80% Market Share in the Bakery Packaging Market

The Asia Pacific region dominates the bakery packaging market, holding a 40.80% share. This is a reflection of the region's expanding consumer base, rapid urbanization, and evolving retail landscape which heavily favors packaged goods for their convenience and longevity.

The high market share in Asia Pacific is driven by the proliferation of bakery chains and the growing affinity for Western-style baked goods among the region's populous countries, such as China and India. Additionally, the rising disposable incomes in these nations contribute to increased consumer spending on packaged foods. The region's vast agricultural sector provides a readily available supply of raw materials for bakery products, which, when coupled with a robust manufacturing base, supports the growth of bakery packaging solutions.

Regional dynamics are characterized by the presence of a large number of small and medium-sized enterprises (SMEs) alongside big players, which fosters a competitive environment conducive to advancements in packaging solutions. The region's diverse cultural palate also demands a variety of bakery products, which requires versatile packaging solutions capable of maintaining product freshness and integrity.

Moreover, the e-commerce boom in Asia Pacific has significantly impacted the bakery packaging market, as online food delivery services require robust and reliable packaging for transportation. This has led to a surge in demand for innovative packaging that meets the logistic requirements of the online food market.

The future influence of Asia Pacific in the bakery packaging market is poised to grow even more significantly. With technological advancements, increasing environmental awareness, and the continuous growth of the middle class, the demand for sustainable and sophisticated packaging solutions is expected to rise.

Bakery Packaging Market by Region

North America

- The US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of Asia Pacific

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of the Middle East & Africa

Key Player Overview: Bakery Packaging Market

The bakery packaging market is characterized by the strategic initiatives and market presence of prominent companies, each contributing to the industry's evolution. Amcor Limited and Bemis Company, Inc. have established themselves as leaders through their focus on innovation in sustainable packaging solutions, thereby influencing environmental standards and consumer expectations. Smurfit Kappa Group and Mondi Group leverage their global footprint and commitment to recyclable materials to drive the market towards sustainability.

The market presence of companies like Genpak, LLC and Reynolds Group Holdings Limited is marked by their extensive range of packaging options catering to various bakery needs, from artisanal to industrial scale. Sydney Packaging Pty Limited and WestRock Company distinguish themselves with customized packaging solutions, enhancing brand value for bakery businesses.

Benson Box Company Ireland Ltd. and A S Food Packaging address niche segments, offering specialized packaging that complements the artisanal and gourmet product lines. NAPCO, Inc. and Stora Enso are recognized for their eco-friendly materials and process innovations, responding to the call for green packaging. Ball Corporation's foray into the market with metal packaging options diversifies the industry's material portfolio.

Collectively, these key players are shaping the bakery packaging market through strategic positioning that emphasizes sustainability, customization, and innovative design. Their influence extends beyond mere packaging, impacting the broader trends of environmental responsibility and technological integration within the market.

Major Companies in the Bakery Packaging Market

- Amcor Plc

- Bemis Company, Inc.

- Smurfit Kappa Group

- Dupont Teijin Films

- Mondi Group

- Berry Global Inc.

- Brow Packaging, Genpak, LLC

- Reynolds Group Holdings Limited

- Sydney Packaging Pty Limited

- WestRock Company

- Benson Box Company Ireland Ltd.

- A S Food Packaging

- NAPCO, Inc.

- Stora Enso

- Ball Corporation

Recent Developments

- In 2023, there is a growing focus on the use of agri-food waste and by-products, such as bagasse, pulps, roots, shells, straws, and wastewater, as valuable resources for creating biopolymers for food packaging materials. These materials are used to produce bioplastics, biofilms, paper, and cardboard, among other sustainable packaging options.

- In 2023, Bakeries explore incorporating smart packaging technologies, like QR codes, NFC tags, or RFID, to provide customers with information about product freshness, ingredients, and allergen details.

- In 2022, IFP relies on smart components such as sensors, indicators, and electronic tags to monitor food quality, package integrity, and food authenticity. These components are crucial for ensuring the safety and quality of food products.

- In 2022, The EU Green Deal continued to target waste exports and extended producer responsibility. Regulations for biodegradable and bio-based plastics were set to be implemented as part of the effort to improve waste management and promote recycling processes.

- In 2022, Antimicrobial nanomaterial-based packaging systems have gained attention in the food packaging industry. These nanomaterials are designed to inhibit microbial growth on food surfaces, thus enhancing food stability and quality.

Report Features Description Market Value (2022) USD 5.7 Bn Forecast Revenue (2032) USD 8.9 Bn CAGR (2023-2032) 7.8% Base Year for Estimation 2022 Historic Period 2016-2022 Forecast Period 2023-2032 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product Type(Bread, Cakes, , Biscuits, Breakfast cereals, Frozen bakery, Frozen desserts), By Type of Material(Flexibles, Rigid plastic, Metal),By Packaging Technique(Modified atmosphere packaging, Vacuum packaging, Flushing with inert gas, Gas Packaging, Active Packaging) Regional Analysis North America - The US, Canada, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Amcor Plc, Bemis Company, Inc., Smurfit Kappa Group, Dupont Teijin Films, Mondi Group, Berry Global Inc., Brow Packaging, Genpak, LLC, Reynolds Group Holdings Limited, Sydney Packaging Pty Limited, WestRock Company, Benson Box Company Ireland Ltd., A S Food Packaging, NAPCO, Inc., Stora Enso, Ball Corporation Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Amcor Plc

- Bemis Company, Inc.

- Smurfit Kappa Group

- Dupont Teijin Films

- Mondi Group

- Berry Global Inc.

- Brow Packaging, Genpak, LLC

- Reynolds Group Holdings Limited

- Sydney Packaging Pty Limited

- WestRock Company

- Benson Box Company Ireland Ltd.

- A S Food Packaging

- NAPCO, Inc.

- Stora Enso

- Ball Corporation

Our Clients

View Our Licence Options