Global Artificial Kidney Market By Device Type(Wearable Artificial Kidney, Implantable Artificial Kidney), By End User(Hospitals, Specialty Clinics, Ambulatory Surgical Centers), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

45912

-

May 2024

-

300

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

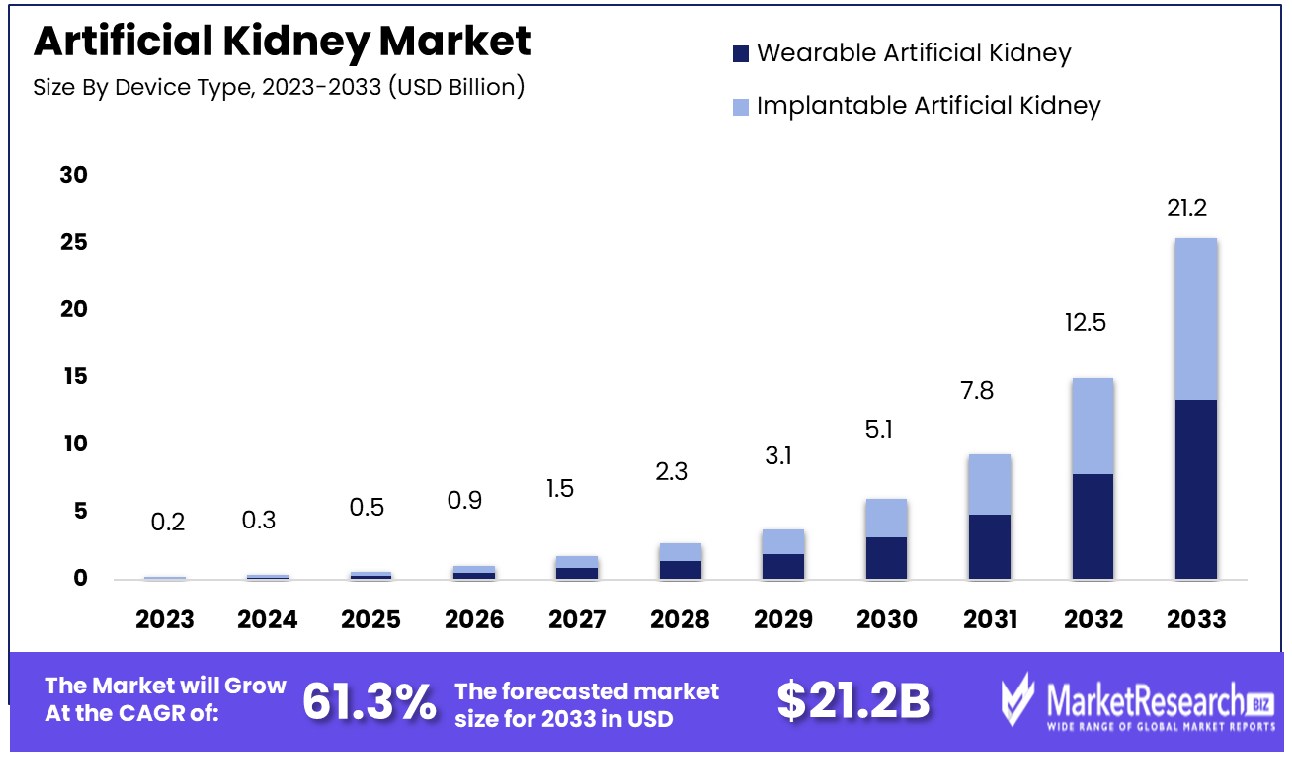

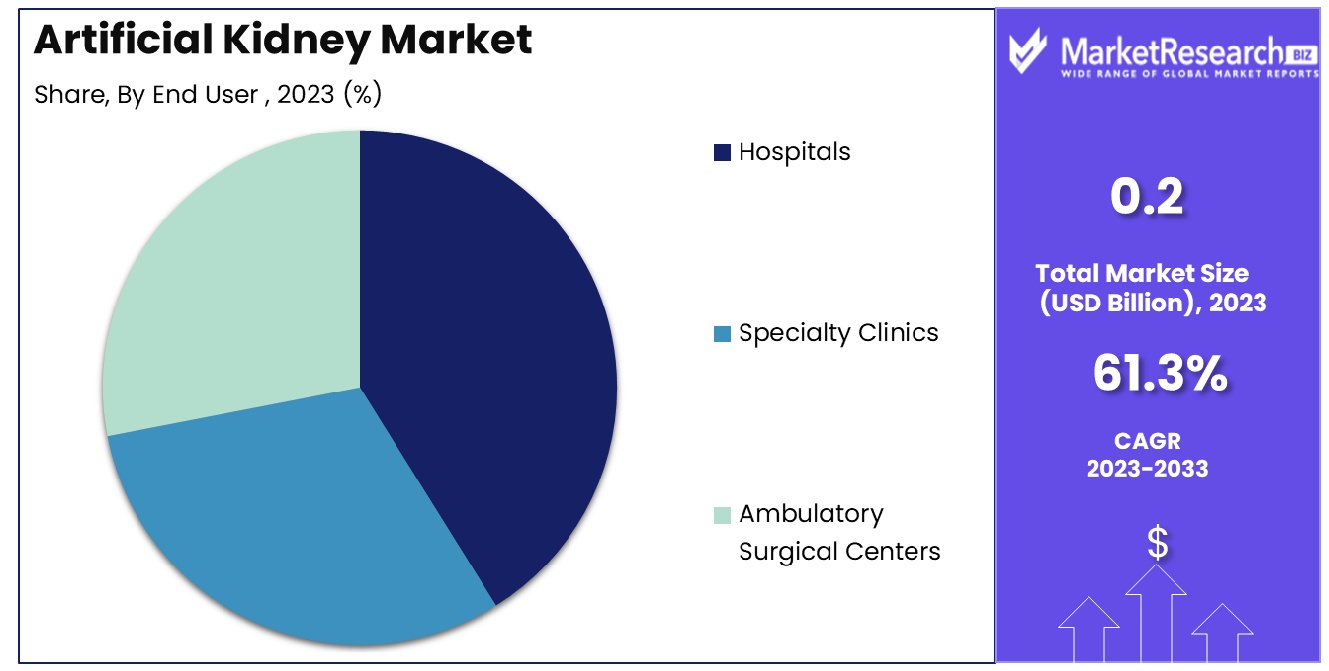

The Global Artificial Kidney Market was valued at USD 0.2 billion in 2023. It is expected to reach USD 21.2 billion by 2033, with a CAGR of 61.3% during the forecast period from 2024 to 2033.

The artificial kidney market refers to the industry focused on the development, production, and distribution of devices that replicate the function of human kidneys. These devices are designed to remove waste products and excess substances from the blood, serving patients with acute or chronic kidney failure.

This market is pivotal for healthcare innovation, offering hope for millions affected by kidney disease and reducing dependency on traditional dialysis and transplants. Key stakeholders, including manufacturers, healthcare providers, and regulatory bodies, collaborate to enhance the efficacy and accessibility of these life-sustaining technologies, driving forward medical advancements and improving patient outcomes.

The artificial kidney market is positioned at a crucial juncture of technological innovation and pressing global healthcare needs. The sector is driven by a growing prevalence of kidney failure combined with a significant gap in the availability of donor kidneys for transplantation. In the United States alone, nearly 750,000 individuals annually suffer from kidney failure, disproportionately affecting minority and economically disadvantaged groups. African Americans are 3.5 times, and both Native Americans and Hispanics are 1.5 times more likely to experience kidney failure than their white counterparts.

This disparity underscores the urgent need for accessible and effective artificial kidney solutions. Moreover, globally, the burden of kidney disease continues to escalate, affecting approximately 2 million people, with a 5-7% annual increase in diagnosed cases. Regions with notably high prevalence rates, including Taiwan, Japan, Mexico, the United States, and Belgium, are potential focal points for market expansion and innovation.

The artificial kidney market is thus not only a field of medical device development but also a significant arena for public health impact. Companies operating in this space must navigate complex regulatory landscapes, advance technological capabilities, and address stark disparities in disease prevalence and treatment access.

For stakeholders, the strategic focus should be on enhancing the scalability of technologies, reducing costs, and improving outcomes, which are critical to tapping into this underserved and rapidly growing market segment. These elements collectively make the artificial kidney market a high-potential, high-impact area in the global healthcare industry.

Key Takeaways

- Market Growth: The Global Artificial Kidney Market was valued at USD 0.2 billion in 2023. It is expected to reach USD 21.2 billion by 2033, with a CAGR of 61.3% during the forecast period from 2024 to 2033.

- By Device Type: Wearable Artificial Kidneys dominated 60% of the market share.

- By End User: Hospitals held 65% dominance in artificial kidney usage.

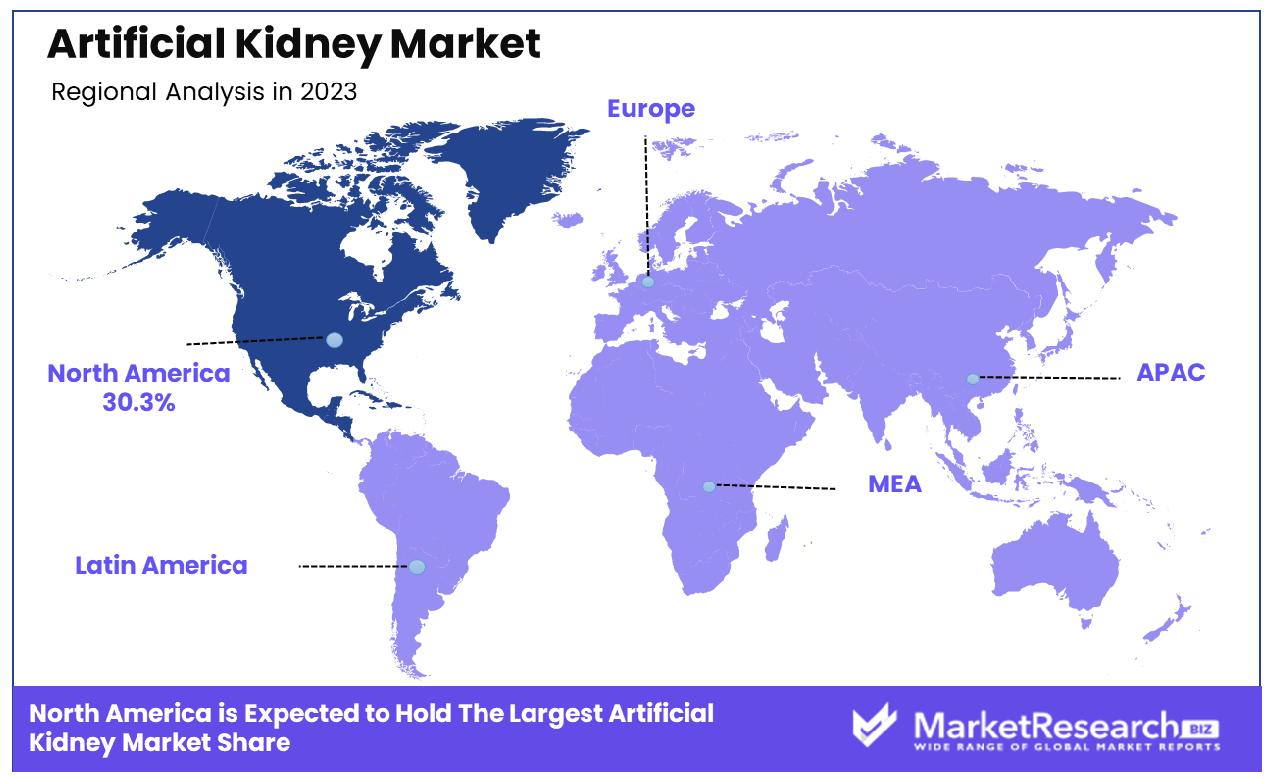

- Regional Dominance: North America holds 30.3% of the global artificial kidney market.

- Growth Opportunity: The artificial kidney market is growing due to advances in wearable kidney devices and the expansion of renal replacement therapy centers, improving patient access and treatment quality.

Driving factors

Rising Prevalence of Chronic Kidney Diseases

The escalating prevalence of chronic kidney diseases (CKD) globally serves as a primary catalyst for the growth of the Artificial Kidney Market. Chronic kidney diseases, including conditions like chronic renal failure, have been on an upward trajectory, largely due to aging populations and increasing rates of diabetes and hypertension.

The World Health Organization estimates that over 1.2 million people die annually due to CKD-related complications, highlighting a critical demand for effective renal replacement therapies, including artificial kidneys. This surge in CKD has spurred significant advancements and investments in the development of artificial kidneys, aiming to alleviate the burden on traditional dialysis and kidney transplant systems and provide patients with more sustainable and less invasive treatment options.

Increasing Demand for Wearable Artificial Kidneys

The demand for wearable artificial kidneys is revolutionizing the Artificial Kidney Market, driven by the need for more convenient and patient-friendly dialysis alternatives. Wearable artificial kidneys allow for continuous dialysis, which better mimics natural kidney functions and offers patients an improved quality of life compared to conventional dialysis methods.

This technology enables mobility and a less restrictive lifestyle, significantly reducing the healthcare costs associated with traditional in-center hemodialysis sessions. The development and increasing adoption of wearable artificial kidneys are anticipated to reduce complications and enhance the efficacy of renal disease management, propelling market growth further.

Presence of Well-Established Healthcare Infrastructure

The presence of well-established healthcare infrastructure significantly enhances the adoption rate and development of advanced medical devices like artificial kidneys. Developed countries, in particular, exhibit robust healthcare systems capable of integrating advanced technologies, thereby facilitating the rapid adoption of innovative solutions such as artificial kidneys.

This infrastructure not only supports extensive research and development activities but also ensures adequate healthcare services, reimbursement policies, and regulatory support necessary for the widespread deployment of new technologies. As such, well-equipped healthcare settings are pivotal in fostering the growth of the Artificial Kidney Market, ensuring that breakthroughs in medical technology reach the patient population effectively.

Restraining Factors

High Cost of Artificial Kidney Implants

The high cost of artificial kidney implants stands as a significant restraining factor in the Artificial Kidney Market. The development and manufacturing of these advanced medical devices involve intricate technology and extensive research, leading to higher production costs. Furthermore, the integration of sophisticated materials and sensors escalates the overall price of the end product.

This cost barrier often limits the accessibility of artificial kidneys, particularly in low- and middle-income countries where healthcare spending is constrained. As a result, even though there is a high demand for renal replacement therapies, the adoption rate of artificial kidneys can be adversely affected by their prohibitive costs, restraining the market's growth potential.

Time-Consuming and Costly Regulatory Approval Process for New Devices

The rigorous and lengthy regulatory approval process for new medical devices also serves as a crucial impediment to the growth of the Artificial Kidney Market. Bringing a medical device from conception to market requires not only substantial financial investment but also compliance with stringent safety and efficacy standards set by regulatory bodies such as the FDA (U.S. Food and Drug Administration) and EMA (European Medicines Agency).

This process often takes several years and involves multiple phases of clinical trials to ensure the device is safe for public use. The associated costs and time can deter new entrants and slow down the pace of innovation and market entry of new artificial kidney models. This not only delays the availability of new treatment options but also burdens existing manufacturers, affecting the overall market dynamics and growth trajectory.

By Device Type Analysis

Wearable artificial kidneys dominated the market with a 60% share, offering continuous dialysis solutions.

In 2023, Wearable Artificial Kidney held a dominant market position in the By Device Type segment of the Artificial Kidney Market, capturing more than a 60% share. This significant market share is primarily driven by the increasing prevalence of chronic kidney diseases (CKD) and the growing demand for portable dialysis solutions. The wearable artificial kidney offers a continuous ambulatory dialysis approach, enhancing patients' quality of life by providing more mobility compared to traditional dialysis methods.

Implantable Artificial Kidney, while still in developmental phases, represented a smaller portion of the market. It is anticipated to gain traction over the coming years due to ongoing advancements in biomedical engineering and nanotechnology. This technology aims to mimic the natural kidney's filtration ability without the need for external dialysis machines, potentially offering a permanent solution to kidney disease patients.

The growth in the Wearable Artificial Kidney segment can also be attributed to technological innovations, increased healthcare expenditure, and a rising emphasis on patient-centered healthcare solutions. Furthermore, regulatory approvals and the expansion of healthcare infrastructure across various regions are accelerating the adoption of these devices. However, high costs and complications associated with wearable kidneys are considerable challenges that the market faces.

Looking ahead, the market is expected to see significant growth as research intensifies and new products are developed. Both segments, Wearable, and Implantable Artificial Kidneys, are poised to transform renal replacement therapy by enhancing the efficacy and convenience of treatments provided to CKD patients.

By End User Analysis

Hospitals held a 65% dominance in the market, reflecting their crucial role in patient treatment.

In 2023, Hospitals held a dominant market position in the end-user segment of the Artificial Kidney Market, capturing more than a 65% share. This substantial market share is primarily attributed to the comprehensive care facilities and advanced technological infrastructure that hospitals offer. Hospitals are equipped to handle the sophisticated requirements of artificial kidney devices, including both wearable and implantable types, which necessitate specialized healthcare personnel and stringent monitoring environments.

Specialty Clinics followed, contributing a significant portion of the market. These clinics often specialize in nephrology and provide targeted treatments for kidney diseases, which supports the adoption of advanced renal care technologies. Their focused approach allows for tailored patient care and often faster adoption of new technologies compared to general hospitals.

Ambulatory Surgical Centers (ASCs) also form a crucial part of the market, especially for procedures that do not require prolonged hospital stays. ASCs have been growing in number due to the cost-effectiveness and efficiency they offer. However, their share in the artificial kidney market is relatively smaller due to the extensive care and monitoring required for artificial kidney patients, which these centers are generally not equipped to handle on a large scale.

The dominance of hospitals is likely to persist as they continue to be the primary centers for comprehensive kidney disease treatment and management. The integration of advanced technologies in artificial kidneys, along with collaborations between hospitals and device manufacturers, is expected to further enhance treatment outcomes and patient management efficiency in this segment.

Key Market Segments

By Device Type

- Wearable Artificial Kidney

- Implantable Artificial Kidney

By End User

- Hospitals

- Specialty Clinics

- Ambulatory Surgical Centers

Growth Opportunity

Development of Wearable Artificial Kidney Devices

The global market for artificial kidneys has witnessed significant momentum from the development of wearable artificial kidney devices. These devices, exemplifying cutting-edge technology, offer a paradigm shift from traditional dialysis methods. The mobility and ease of use associated with wearable devices enhance patients' quality of life and compliance with treatment regimens. Technological advancements have facilitated the miniaturization of components, enabling their integration into wearable formats that mimic the natural physiological process of waste removal continuously.

This innovation is expected to drive substantial market growth as it addresses the critical need for more accessible and less intrusive renal replacement therapies. Market penetration of these devices depends on regulatory approvals and the establishment of reimbursement policies, which are crucial for widespread adoption.

Expansion of Renal Replacement Therapy Centers

Parallel to technological innovations, there is an expansion in the number of renal replacement therapy (RRT) centers globally, which significantly contributes to the growth of the artificial kidney market. The increasing prevalence of kidney diseases and the rising demand for advanced treatment options have led to enhanced healthcare infrastructure. New RRT centers are being established, particularly in regions with previously underserved populations, thus broadening the accessibility to life-sustaining treatments.

This expansion not only supports the immediate needs of patients but also integrates new technologies such as wearable artificial kidneys into clinical practice. The growth of these centers reflects a proactive approach to healthcare planning, emphasizing the importance of renal health and ensuring the availability of advanced treatments across different geographic locations.

Latest Trends

Focus on Improving Patient Outcomes and Quality of Life

In 2023, a predominant trend in the global artificial kidney market is the heightened focus on improving patient outcomes and enhancing quality of life. This shift is driven by patient-centric healthcare models that prioritize minimal disruption to daily life and reduction of treatment-related discomfort.

Innovations in artificial kidney technology are increasingly aimed at developing solutions that are not only effective in managing renal failure but also in aligning with patients' lifestyles. This includes the creation of more compact, efficient, and user-friendly dialysis devices that can be used at home, reducing the need for frequent hospital visits and thereby significantly improving the quality of life for patients with kidney diseases.

Collaboration between Healthcare Institutions and Industry Players

Another significant trend shaping the artificial kidney market is the collaboration between healthcare institutions and industry players. These partnerships are crucial for the rapid development and implementation of advanced renal care technologies. Through collaborative efforts, clinical insights and patient data are shared, leading to innovations that are both clinically validated and tailored to meet the specific needs of patients.

Such collaborations often result in streamlined regulatory pathways and quicker adoption of new technologies in clinical trial settings. Additionally, these partnerships are instrumental in training healthcare providers to use new technologies effectively, ensuring that the benefits of innovations are maximized for patient care.

Regional Analysis

In 2023, North America held a 30.3% share of the global artificial kidney market.

The Artificial Kidney Market is segmented into several key regions: North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America, each exhibiting distinct market dynamics and growth potentials.

North America emerges as the dominating region, holding a substantial market share of 30.3%. This prominence is primarily driven by advanced healthcare infrastructure, high healthcare spending, and a strong presence of leading market players in the U.S. and Canada. The increasing prevalence of kidney diseases and a well-established network for organ transplants further augment the market growth in this region.

Europe follows, with significant investments in healthcare research and a rising number of kidney disease cases. The market here benefits from robust government support for healthcare facilities and the adoption of advanced technologies in countries like Germany, France, and the UK.

The Asia Pacific region is witnessing the fastest growth due to improved healthcare facilities, increasing awareness about kidney diseases, and rising disposable income. Countries like China and India are pivotal to this growth, driven by large patient pools and increasing government focus on healthcare reforms.

The Middle East & Africa region shows promising growth, supported by the development of healthcare infrastructure and increasing access to treatment facilities. However, the market growth is somewhat hampered by the high cost of advanced treatments and lack of awareness.

Latin America's market is growing steadily, bolstered by the gradual improvement in healthcare services and government initiatives to improve kidney disease management in countries like Brazil and Mexico.

Overall, the global landscape for the Artificial Kidney Market presents a robust growth trajectory, with North America maintaining a leading position due to its advanced healthcare systems and high investment in medical research.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of Middle East & Africa

Key Players Analysis

In the global Artificial Kidney Market, several key players have significantly contributed to advancements and growth within this sector in 2023. Kawasumi Laboratories Inc. continues to play a pivotal role with its robust product portfolio and strategic collaborations that enhance its distribution capabilities globally. Similarly, Blood Purification Technologies Inc. stands out for its innovative approaches to developing technologies that aim to improve the efficacy of blood filtration and purification, aligning with current healthcare needs.

AWAK Technologies Pte. Ltd. is noted for its disruptive wearable dialysis technology, which has the potential to transform patient quality of life by offering more freedom compared to traditional dialysis methods. This innovation not only addresses patient comfort but also reduces the healthcare system's burden by enabling at-home treatment. Trimmed AB, although smaller in scale, has made notable strides in integrating artificial intelligence to optimize kidney care outcomes, reflecting significant potential for growth and impact.

Asahi Kasei Medical Co. Ltd. maintains its industry leadership through continuous research and development, leading to high-performance dialysis treatment solutions. This is complemented by its strong global footprint, which ensures widespread accessibility of its advanced medical products. US Kidney Research Corporation introduces a groundbreaking approach with its research into artificial kidney development, which promises to be a game-changer in renal replacement therapy.

Merit Medical Systems and NIPRO Medical Corporation both contribute to the market through their extensive range of dialysis equipment and supplies, enhancing operational efficiencies in kidney treatment. Lastly, Fresenius SE & Co. KGaA remains a dominant force, with its comprehensive solutions in kidney care and a strong emphasis on research and innovation, driving forward the standards of care and treatment efficacy in the artificial kidney landscape.

Market Key Players

- Kawasumi Laboratories Inc.

- Blood Purification Technologies Inc.

- AWAK Technologies Pte. Ltd

- Trimmed AB

- Asahi Kasei Medical Vo. Ltd

- US Kidney Research Corporation

- Merit Medical Systems

- NIPRO Medical Corporation

- Fresenius SE & Co. KgaA

Recent Development

- In April 2024, Massachusetts General Hospital (MGH) successfully discharged the first patient to receive a genetically modified pig kidney transplant, marking a historic milestone in transplantation. The procedure, conducted with support from eGenesis, offers hope for addressing the organ shortage crisis.

- In March 2024, The state government of India, in collaboration with Hellokidney.ai, led by Dr. Chinta Ramakrishna, plans to implement an AI-based mobile app for kidney disease screening, revolutionizing primary healthcare and redefining kidney health outcomes.

- In February 2024, Healionics secures $5.5 million to advance human trials of STARgraft, an artificial blood vessel for dialysis patients. The Seattle-based firm aims for regulatory approval and commercialization to address vascular access challenges.

Report Scope

Report Features Description Market Value (2023) USD 0.2 Billion Forecast Revenue (2033) USD 21.2 Billion CAGR (2024-2032) 61.3% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Device Type(Wearable Artificial Kidney, Implantable Artificial Kidney), By End User(Hospitals, Specialty Clinics, Ambulatory Surgical Centers) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Kawasumi Laboratories Inc., Blood Purification Technologies Inc., AWAK Technologies Pte. Ltd, Trimmed AB, Asahi Kasei Medical Vo. Ltd, US Kidney Research Corporation, Merit Medical Systems, NIPRO Medical Corporation, Fresenius SE & Co. KgaA Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Kawasumi Laboratories Inc.

- Blood Purification Technologies Inc.

- AWAK Technologies Pte. Ltd

- Trimmed AB

- Asahi Kasei Medical Vo. Ltd

- US Kidney Research Corporation

- Merit Medical Systems

- NIPRO Medical Corporation

- Fresenius SE & Co. KgaA

Our Clients

View Our Licence Options