Global Artificial Intelligence (AI) In Radiology Market Size, Share, Growth, And Industry Analysis By Solution Type (AI Software, AI Hardware), Technology (Machine Learning, Deep Learning, NLP), Application (Image Analysis, Workflow Optimization,) And By Region Forecast - 2023-2032

-

41127

-

Sep 2023

-

155

-

-

This report was compiled by Vishwa Gaul Vishwa is an experienced market research and consulting professional with over 8 years of expertise in the ICT industry, contributing to over 700 reports across telecommunications, software, hardware, and digital solutions. Correspondence Team Lead- ICT Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

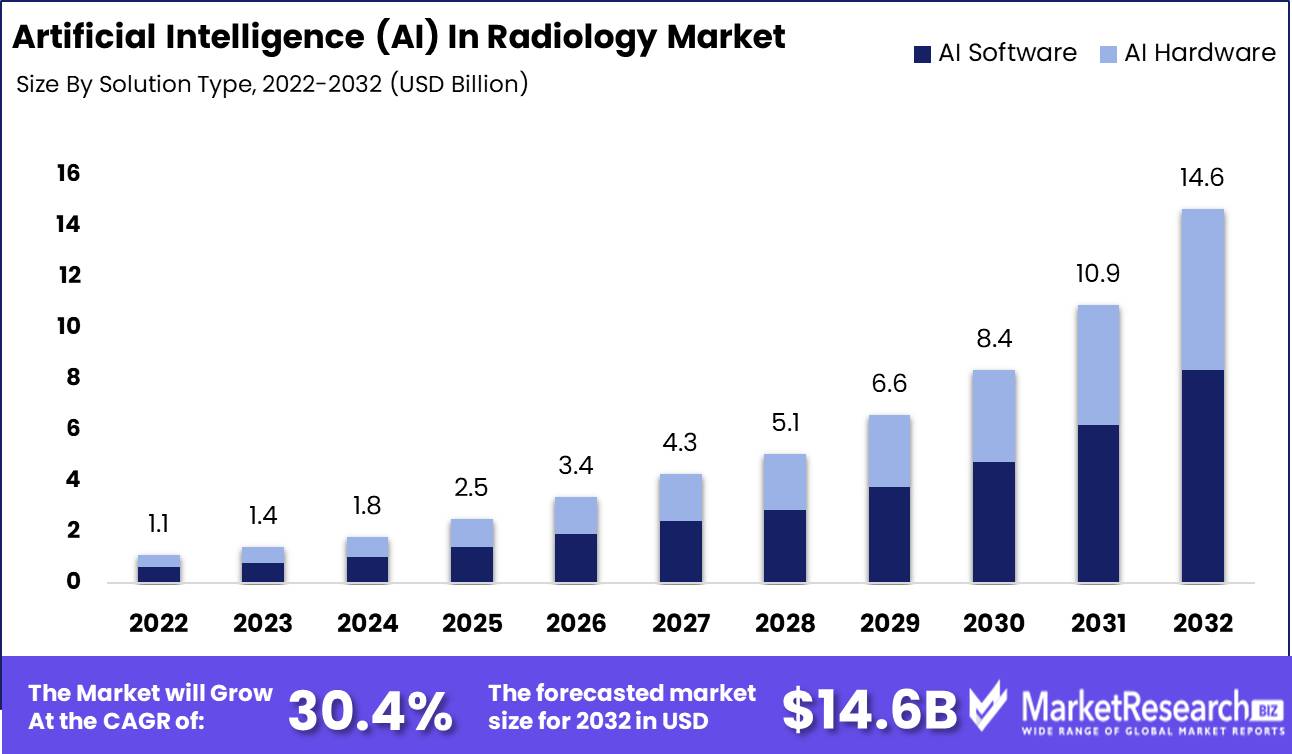

Artificial Intelligence (AI) In Radiology Market size is expected to be worth around USD 14.6 Bn by 2032 from USD 1.1 Bn in 2022, growing at a CAGR of 30.4% during the forecast period from 2023 to 2032.

Key Takeaways

- The global AI in radiology market is registering robust growth, with a CAGR of approximately 22% during the forecast period

- Global AI in radiology market revenue is expected to exceed USD 15.6 Bn by the end of the forecast period

- Asia-Pacific is registering significantly rapid revenue growth rate, with a regional revenue CAGR expected to remain around 24.5% over the forecast period

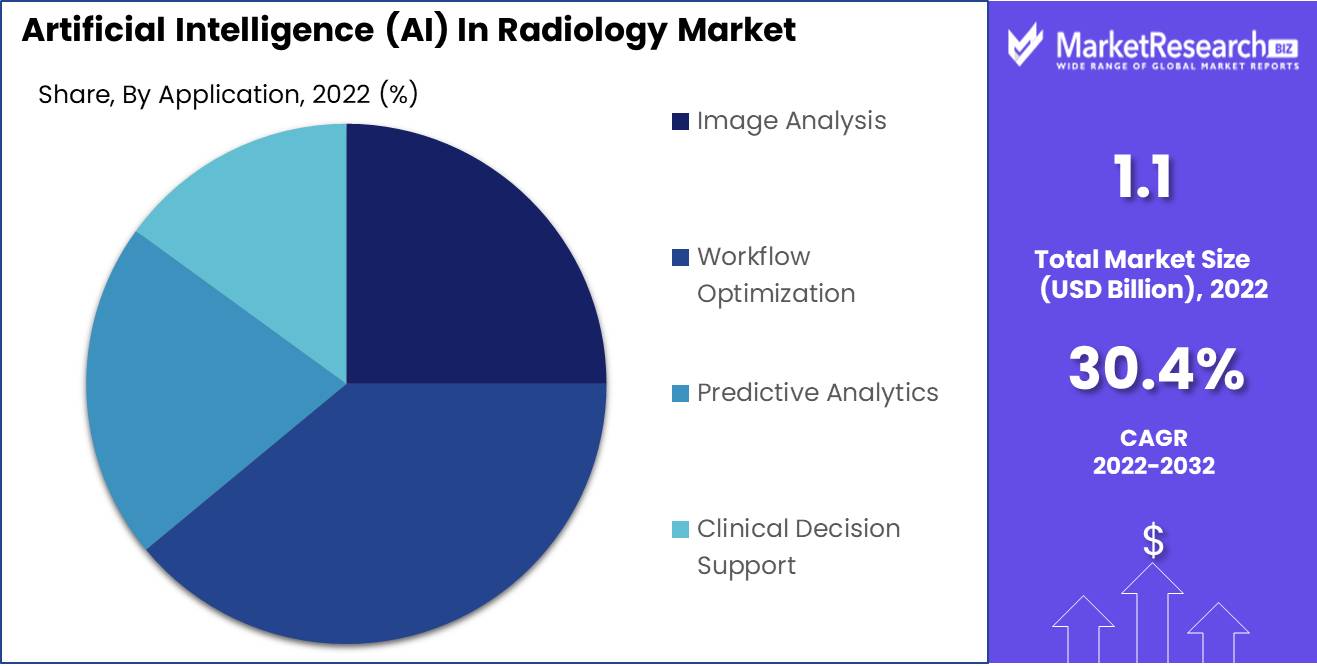

- The image analysis segment accounted for largest revenue share in 2022 and is expected to register a CAGR of approximately 21.6% over the forecast period

- The clinical decision support segment accounted for largest revenue share in 2022, and this segment is expected to register a CAGR of around 24% over the forecast period

- Over 500 service providers have integrated AI into their radiology services and offerings in the past year, reflecting the growing adoption of AI technologies in the healthcare industry

Market Overview

Artificial Intelligence (AI) in radiology entails the use of advanced Machine Learning (ML) and deep learning algorithms to assist radiologists and healthcare professionals in the interpretation and analysis of medical images such as X-rays, CT scans, MRIs, and ultrasound images. Integration of AI-powered technologies have been proving to be highly beneficial in various medical, science, and healthcare fields and applications. Integration has been enhancing diagnostic accuracy, speed of diagnosis, and efficiency.

Machine learning and deep learning algorithms analyze images, assisting radiologists in identifying anomalies. Computer-aided detection (CAD) systems flag potential issues, while AI-driven workflow optimization streamlines administrative tasks. Image enhancement, predictive analytics, and quantitative analysis provide invaluable insights for treatment decisions. These technologies integrate with Electronic Health Records (EHR), improving patient care coordination. Widely used AI applications in radiology include CAD for cancer detection, image denoising, predictive modeling for disease progression, and population-level health management. AI is a pivotal tool, augmenting expertise of radiologists while transforming outcomes in the healthcare sector.

Revenue growth of the global Artificial Intelligence (AI) in radiology market is expected to continue to increase significantly, driven by rising demand for accurate and efficient medical imaging diagnosis. Advancements in deep learning algorithms, and initiatives promoting AI integration in healthcare systems and research are also expected to contribute to revenue growth of the market.

Also, consumption trends indicate increasing AI adoption in radiology practices and hospitals, with ability of AI to improve diagnosis speed and accuracy being a major advantage. Rising focus on enhancing patient care, reducing healthcare burden and costs, and revolutionizing the field with data-driven insights are some trends observed in the market.

Driving Factors

Increased Diagnostic Accuracy

AI algorithms improve the accuracy of radiological diagnoses, thereby reducing potential for errors and need for re-evaluation. Increased accuracy serves to drive confidence in diagnoses and also adds some level of interest in more healthcare facilities adopting AI solutions. As an increasing number of healthcare providers and public and private hospitals, clinics, and medical and research centers adopt and integrate newer technologies, driven by the modernization and digitization trends, revenue growth from the market is also expected to increase in parallel over the forecast period.

Efficiency and Productivity

AI streamlines radiology workflows by automating routine tasks such as image sorting and annotation. Radiologists can review cases faster, leading to increased patient throughput and revenue generation.

Population Health Management

AI enables the analysis of large datasets, facilitating population-level health management. This trend can lead to proactive disease prevention and management, and continued success along the way will further serve to encourage increased adoption and deployment among healthcare providers and medical centers.

Personalized Medicine

AI enables designing customized treatment plans based on individual patient data and medical imaging results. The ability to provide personalized care improves patient outcomes and allows healthcare organizations looking to offer high-value services design more premium treatment options and offer personalized services.

Research and Development

Ongoing research and development initiatives in the medical imaging field and integration of more advanced technologies and approaches are supporting expansion of AI in radiology. As AI algorithms become more advanced and versatile, these can be applied to a wider range of medical imaging modalities and conditions, thereby opening up more potential opportunities and revenue streams.

Restraining Factors

Regulatory Challenges and Compliance

Stringent regulatory requirements and compliance issues are cumbersome under some circumstances for players operating in the market and can restrain implementation of AI in radiology. AI systems must meet regulatory standards, especially with regard to patient data privacy and safety, and ensuring the proper measures and safeguards can be costly and time-consuming.

Limited Data Availability

AI algorithms in radiology are reliant on large datasets for training and validation. Availability of high-quality, diverse data, or for specific medical conditions may be a limited in some countries or regions, which can impede further development and adoption of AI solutions, particularly in niche areas of radiology.

High Initial Costs

Implementing AI systems, including purchase of AI-enabled equipment and software, can entail substantial upfront investments. Smaller or budget-constrained healthcare facilities and institutions may face challenges to justify these costs, and this is a major factor that restrains adoption and hampers potential revenue growth of the market.

Opportunities

Software as a Service Offerings

Companies can capitalize on the trend of offering AI-powered radiology solutions as subscription-based services and this model can be a lucrative option as it serves as a recurring revenue stream. This further allows for providers to continually update and improve their AI algorithms while providing cost-effective solutions to healthcare providers. This model is also appealing to subscribers or healthcare providers due to the fact that users will be able to access regular updates and new features whenever these are made available by the service provider.

Data Analytics and Insights

Along with diagnostic tools, companies can leverage the data generated by AI systems to provide valuable insights and analytics to healthcare organizations. This includes predictive analytics for patient outcomes, population health management, and treatment efficacy assessment, thus creating opportunities for additional revenue streams.

Partnerships and Collaborations

Equipment manufacturers and other solutions and technology development companies can collaborate with healthcare institutions to open potential for joint ventures and co-development initiatives. Such partnerships can lead to the creation of integrated solutions that combine AI technology with medical devices, as well as further expand revenue opportunities.

Segment Analysis

By Solution Type

Among the solution type segments the AI software segment accounted for majority revenue share in 2022. Robust revenue growth of this segment is supported is driven by continuous development of advanced AI algorithms and integration of Natural Language Processing (NLP) and computer vision technologies, enabling more comprehensive and accurate analysis of radiological data.

By Technology

Among the technology segments, the machine learning segment accounted for majority revenue share contribution in 2022. Machine learning algorithms are at the core of many AI applications in radiology, offering the ability to learn from data and make predictions. Robust revenue growth of this segment is supported by increasing availability of large medical imaging datasets for training machine learning models and growing expertise in algorithm development for radiological tasks, resulting in improved diagnostic accuracy and efficiency.

By Application

Workflow Optimization solutions are gaining traction as healthcare institutions seek to improve operational efficiency and reduce workload for radiologists. These solutions help automate routine tasks and prioritize critical cases. The revenue growth in this segment is driven by the rising demand for streamlined radiology workflows and the reduction of radiologist burnout, resulting in improved healthcare delivery and resource utilization.

Market Segmentation

Solution Type

- AI Software

- AI Hardware

Technology

- Machine Learning

- Deep Learning

- Natural Language Processing (NLP)

- Computer Vision

Application

- Image Analysis

- Workflow Optimization

- Predictive Analytics

- Clinical Decision Support

End-User

- Hospitals

- Diagnostic Imaging Centers

- Research and Academic Institutions

- Others

- Clinics

- Ambulatory Care Centers

Deployment

- Cloud-Based

- On-Premises

Regional Analysis

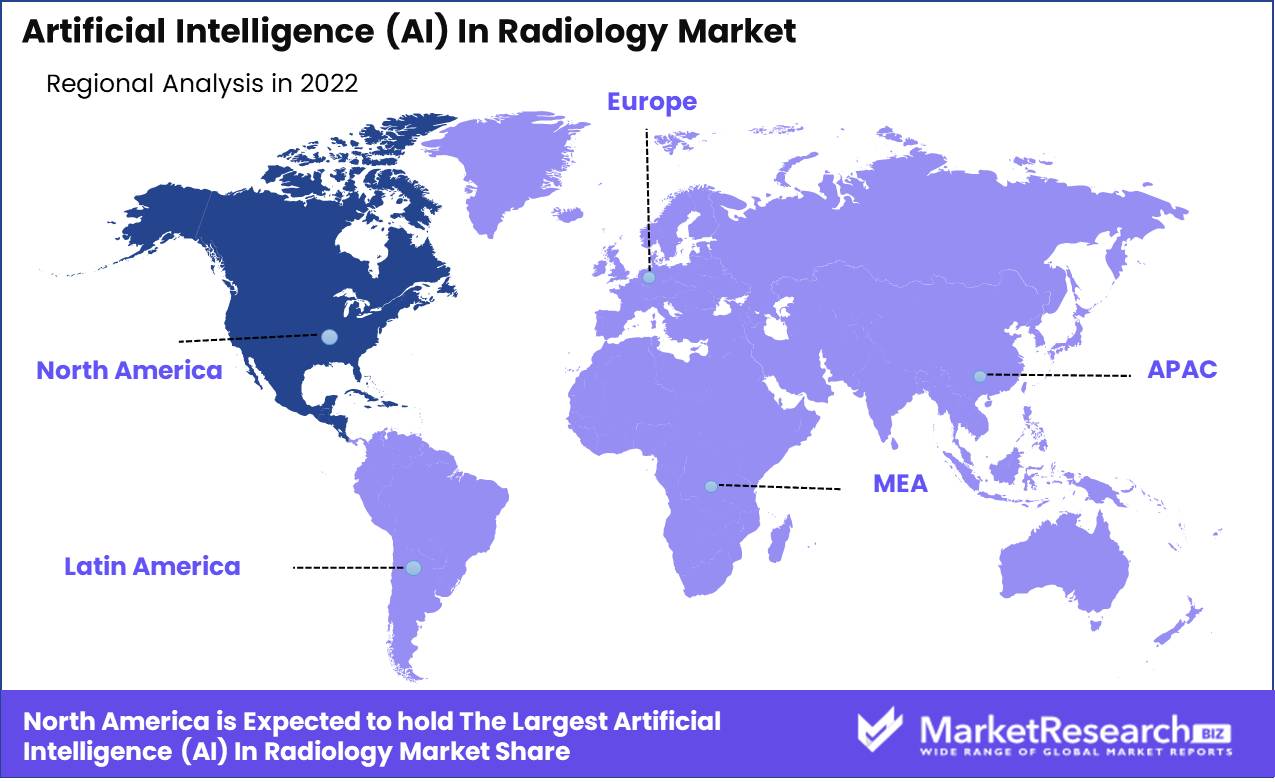

North America

North America accounts for a significantly large revenue share of the global AI in radiology market, and this is driven by a well-established healthcare infrastructure and technological advancements in countries in the region. The U.S., in particular, is a major revenue contributor. Market growth is also supported by rising adoption of AI-driven diagnostic tools, AI-powered EHR integration, and research initiatives in leading medical institutions in the U.S. Increasing partnerships between tech companies and healthcare providers to develop innovative AI solutions and streamlining of approval processes by regulatory bodies for AI applications in healthcare is expected to continue.

Europe

Europe AI in radiology market is registering steady revenue growth, with countries such as Germany, the UK, and France leading in terms of revenue share contribution respectively. Strong government support for healthcare technology initiatives, including AI, rising demand for AI-assisted diagnosis, focus on improving patient care and reducing healthcare costs, technological advancements in AI algorithms, and increased data availability are some other key factors driving Europe market revenue growth. Initiatives such as data-sharing networks among countries in the region is promoting research and development, and is expected to further contribute to market revenue growth.

Asia-Pacific

Asia-Pacific market revenue growth rate is expected to continue to be fastest among the regional markets and this is supported by significant contribution from countries such as China, Japan, and India, where AI adoption in radiology has increased substantially in the recent past. Also, increasing prevalence of chronic diseases is driving demand for efficient diagnostic solutions in a number of countries in the region. Government initiatives promoting AI technology in healthcare, technological developments in AI image analysis and remote diagnostics, and collaborations between healthcare providers and AI startups are also expected to support revenue growth of the market over the forecast period.

Latin America

Latin America is an emerging market for AI in radiology, with Brazil, Mexico, and Argentina accounting for majority revenue contribution. Though relatively smaller currently, revenue share of the market in Latin America is expected to increase steadily over the next few years. This can be attributed to factors such as rising awareness among healthcare providers and medical facilities regarding the benefits of AI in radiology. Also, rising focus on improving healthcare infrastructure and need to address healthcare disparities, coupled with technological advancements supported by local startups focusing on developing AI solutions tailored to the specific needs of countries in the region are expected to support market growth. In addition, initiatives across public and private sectors supporting AI adoption will drive market growth.

Middle East and Africa

Healthcare providers in countries in Middle East and Africa are gradually adopting AI in radiology, with the UAE and South Africa leading the way. Market share is relatively modest currently, but growth potential is expected to incline further as healthcare facilities seek to enhance diagnostic accuracy. Potential revenue growth is also supported by government investments in healthcare technology and infrastructure development. Technological developments in AI image processing and telemedicine are also expected to support market growth. Initiatives to further encourage developments and advancements in AI in radiology include collaborations with international tech firms and training programs for healthcare professionals.

Segmentation By Region

North America

- United States

- Canada

Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- Association of Southeast Asian Nations (ASEAN)

- Rest of Asia Pacific

Europe

- Germany

- The U.K.

- France

- Spain

- Italy

- Russia

- Poland

- BENELUX (Belgium, the Netherlands, Luxembourg)

- NORDIC (Norway, Sweden, Finland, Denmark)

- Rest of Europe

Latin America

- Brazil

- Mexico

- Argentina

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Egypt

- Israel

- Rest of MEA (Middle East & Africa)

Competitive Landscape

The global Artificial Intelligence (AI) in radiology market has been registering significant growth in recent years, driven by steadily increasing adoption of AI technologies in the healthcare sector to enhance diagnostic accuracy and efficiency. The competitive landscape in this market is dynamic, with a number of key players and service providers competing for majority market share and expanding geographically.

The landscape is continually evolving, owing to existing companies developing and introducing new services and solutions, and new entrants and startups also contributing to innovation. Development of cutting-edge AI algorithms, regulatory approvals, strategic partnerships with healthcare providers, and the ability to provide cost-effective and accurate solutions are essential for maintaining a strong standing in this increasingly competitive market. Below are some key trends and moves observed in the market.

A number of leading AI in medical imaging companies have entered into strategic partnerships and collaborations with healthcare institutions, research organizations, and technology providers to accelerate the development and deployment of AI solutions. These partnerships are ideally to combine domain expertise with AI capabilities for better patient care and diagnostic accuracy. Besides, companies are also leveraging mergers and acquisitions to enable market consolidation. Larger healthcare and technology companies have acquired AI startups with innovative solutions to expand their AI offerings and gain a competitive edge, as well as enhance AI portfolios and gain access to broader customer bases.

In addition, key players regularly launch new AI-powered radiology products and software solutions, with additional focus on improving image interpretation, automating repetitive tasks, and providing clinical decision support. Continuous product innovation is vital to stay competitive and meet evolving healthcare demands.

Furthermore, new product/service launches and enhancements to existing offerings, expanded service offerings, obtaining regulatory approvals, increasing focus on specialty areas, leveraging scalability and accessibility through offering of cloud-based solutions, and international expansion to tap into global markets and meet international regulatory requirements and compliances are some key trends observed in the market.

Company List

- IBM Corporation

- GE Healthcare

- Siemens Healthineers

- Philips Healthcare

- NVIDIA Corporation

- Canon Medical Systems

- Arterys

- Zebra Medical Vision

- Nuance Communications

- Aidoc

- 3D Systems

- Butterfly Network

- PathAI

- Subtle Medical

- Qure.ai

- Imagen Technologies

- Quibim

- Viz.ai

- CureMetrix

- Tempus

Recent Developments

- In June 2022, Bayer unveiled its new Calantic Digital Solutions, which is a cloud-hosted platform delivering access to digital applications. This solution includes AI-enabled programs for medical imaging, which also comprises tools to help triage critical patient findings for expedited review, improve lesion detection and automate tasks. Bayer has with this new move expanded its radiology portfolio into more diverse possibilities.

- In August 2021, Launch of Paxera’s newest product, PaxexaUltima 8th Generation, which is an AI-based imaging platform, was made at HIMSS 2021 in Las Vegas, US. The latest product is based on cutting-edge AI algorithms for analysis of large data sets, and prioritizes studies and provides support for clinical analysis. Also, it supports collaborative learning, thereby allowing users to directly contribute their diagnostic knowledge to the AI model’s database to enable access to more information for future analysis, and is designed for Chest X-ray, Mammo, and Brain CT, detects 20 abnormalities, and can learn and improve with each user interaction.

- In November 2021, Royal Philips, which is a global leader in health technology, announced its new AI-enabled innovations in MR imaging launching at the Radiological Society of North America (RSNA) annual meeting (November 23 – December 2, Chicago, USA). The company’s new MR portfolio of intelligent integrated solutions is designed to speed up MR exams, streamline workflows, optimize diagnostic quality, and help ensure the efficiency and sustainability of radiology operations.

Report Scope of the Artificial Intelligence (AI) In Radiology Market

Report Features Description Market Value (2022) USD 310.0 Mn Forecast Revenue (2032) USD 2,154.4 Mn CAGR (2023-2032) 22.0% Base Year for Estimation 2022 Historic Period 2016-2022 Forecast Period 2023-2032 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered Solution Type(AI Software, AI Hardware), Technology(Machine Learning, Deep Learning, Natural Language Processing (NLP), Computer Vision), Application(Image Analysis, Workflow Optimization, Predictive Analytics, Clinical Decision Support), End-User(Hospitals, Diagnostic Imaging Centers, Research and Academic Institutions, Others), Clinics(Ambulatory Care Centers, Deployment, Cloud-Based, On-Premises) Regional Analysis North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape IBM Corporation, GE Healthcare, Siemens Healthineers, Philips Healthcare, NVIDIA Corporation, Canon Medical Systems, Arterys, Zebra Medical Vision, Nuance Communications, Aidoc, 3D Systems, Butterfly Network, PathAI, Subtle Medical, Qure.ai, Imagen Technologies, Quibim, Viz.ai, CureMetrix, Tempus Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- IBM Corporation

- GE Healthcare

- Siemens Healthineers

- Philips Healthcare

- NVIDIA Corporation

- Canon Medical Systems

- Arterys

- Zebra Medical Vision

- Nuance Communications

- Aidoc

- 3D Systems

- Butterfly Network

- PathAI

- Subtle Medical

- Qure.ai

- Imagen Technologies

- Quibim

- Viz.ai

- CureMetrix

- Tempus

Our Clients

View Our Licence Options