Aptamers Market By Type (Nucleic Acid and Peptide), By Application (Diagnostics, Therapeutics, Research & Development, and Other), By End User, By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2023-2032

-

3100

-

May 2023

-

190

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

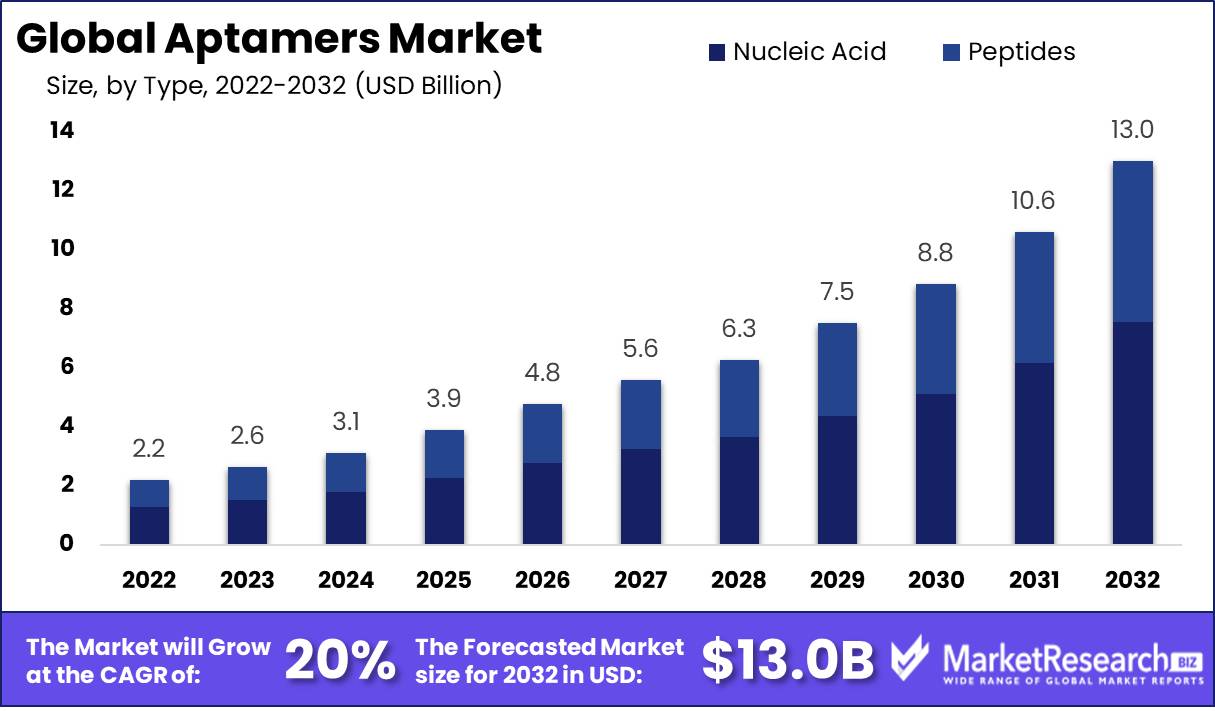

Aptamers Market size is expected to be worth around USD 13.0 Bn by 2032 from USD 2.2 Bn in 2022, growing at a CAGR of 20% during the forecast period from 2023 to 2032.

Aptamers are thermostable and can maintain their structure after repeated denaturation and renaturation cycles. The introduction of the chemical modification system, which will increase nuclease resistance and therapeutic properties, is expected to boost market growth. Global aptamers market Report offers a detailed analysis of the market. This report gives a comprehensive analysis of key market segments. Aptamers are single-stranded DNA molecules or RNA molecules that bind only to one target.

Aptamers are able to take many forms because they can form single-stranded loops or helices. Aptamers are easy to create and can be used to inhibit and identify proteins. Aptamers can be used for biotechnological and therapeutic purposes. They also have analytical applications like food safety and environmental monitoring. They are used for research, diagnostics, biosensing, and as tools for drug development or biomarker creation worldwide.

Driving factors

Rising awareness of the Advantages of Aptamers Over Antibodies

Aptamers are better at targeting small molecules than antibodies, although they have limitations. They are able to bind to small molecules and colors and can be used in standard diagnostic kits. It will result in a greater aptamers market value and acceptance of aptamers for diagnostic and therapeutic purposes.

Aptamers are also capable of binding to large molecules. Research Antibodies can be created by using recombinant DNA technology and animal models to generate antibodies. Chemical methods that are cheaper than traditional ones can be used to synthesize aptamers. Aptamers are, therefore, more attractive for developing and testing diagnostic tools and therapeutic drugs. For antibodies-based treatments for neurodegenerative disorders such as Alzheimer's, the blood-brain barrier is a more difficult problem.

Although technological advancement has helped bridge the gap, antibodies against this disorder's effectiveness and safety remain intact. Aptamer has many advantages, including a lower production cost, ease of design and synthesis, as well as high efficiency. Peptides drive innovation in the Aptamers Market, revolutionizing targeted therapies and diagnostic applications.

Restraining Factors

Low Market Acceptance as Compared to Antibodies

Aptamer market growth is impeded by the limitations of Aptamers. Aptamers have a long history of being used as therapeutic agents. They are comparable to monoclonal antibody therapeutics -like antibodies in that they are specific and highly affinity for their target. Aptamers have many advantages over antibodies, but they also have limitations that limit their widespread clinical application as therapeutic Agents.

The limitations involve serum stability, renal filtration, endocytic escape, and lack of diversity within the nuclease susceptibility, Aptamer Library, and claims of aptamer specialty. Many aptamers are susceptible to rapid degradation in biological media because of interactions with biomolecules.

Type Analysis

Nucleic Acid and Peptides are Main Products in Global Aptamers Segment

Based On type aptamers market segment is divided into nucleic acid and Peptide. Nucleic Acid holds the market's largest share with 58%. It also holds the highest revenue share. This segment is expected to see the most growth over the forecast period. Numerous companies are now investing in the nucleic acid-aptamer mechanism of action for the treatment of many disorders, including age-related macular degeneration. Due to its wide application base, the peptide-aptamer market segment will see a significant increase in revenue over the forecast period.

This testing is done using next-generation biochips that are based on molecular recognition and peptide aptamer markers system. Researchers have created peptide aptamers by using data from the data bank. The introduction of such products may increase the use of peptide-aptamers. This is due to the lower production costs and greater stability compared to the wide availability of DNA aptamers than other nucleic acids-based aptamers.

By Application Analysis

Growing Research Activities, Rising Prevalence of Cancer, and Occurrence of Malnutrition Cases During Cancer Treatment Helping the Market Grow.

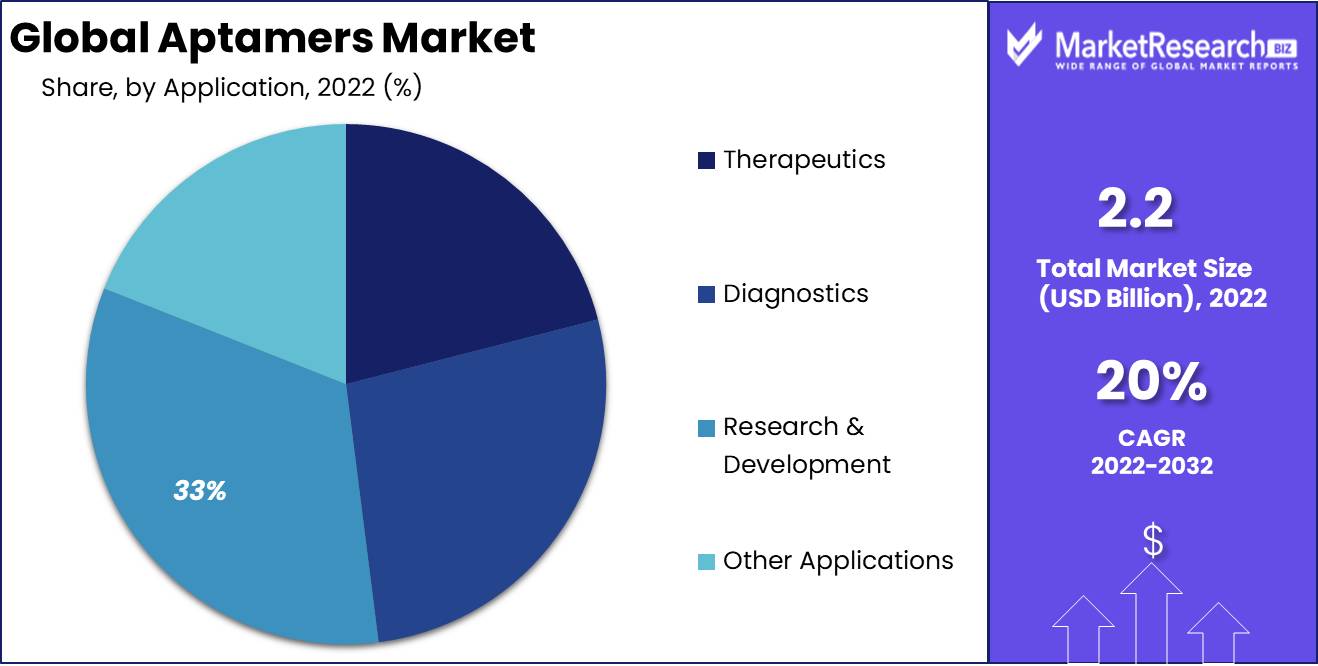

Based on application, the aptamers market segment includes therapeutics, diagnostics, research & development, and other applications. The research & development segment dominated the market in 2022 with a 33% share due to its increasing demand and growing research activities. The therapeutic development segment is the fastest-growing segment in the global aptamers market.

This segment has seen a significant increase in demand for aptamers and an increase in research in this area because of the growing number of clinical trials that evaluate aptamers for new therapies and collaborative partnerships between aptamer firms and top pharmaceutical and biopharmaceutical companies. The diagnostic segment is expected to grow at the fastest rate of CAGR due to the increasing prevalence of chronic diseases.

End-User Analysis

Pharmaceutical and Biotechnological Companies are the Largest end Users of the Aptamer Market

Based on the end-user, the aptamers market is segmented into pharmaceutical companies and biotechnological companies, contract research organizations, academic & government research organizations, and other end-users. Biotechnological and pharmaceutical companies dominate the aptamers market. This is due to the increase in key players offering custom aptamers for therapeutic development and increasing R&D spending. Due to the development of diagnostic tools for infectious diseases and cancer, the diagnostic segment will see the highest CAGR over the forecast period.

Key Market Segments

Based By Type

- Nucleic Acid

- Peptides

By Application

- Therapeutics

- Diagnostics

- Research & Development

- Other Applications

By End-User

- Pharmaceutical & Biotechnological Companies

- Contract Research Organisations

- Academic & Government Research Organisations

- Other End-Users

Growth Opportunity

Growing Healthcare Infrastructure Across the Emerging Market

Due to the growth of healthcare industries in emerging countries such as South Africa, India, and China, the aptamers market is booming. These nations need to advance their healthcare market due to the rapidly increasing geriatric population, high patient numbers, increasing per capita incomes, and increased awareness. Several aptamer development corporations recognize the potential of aptamers for diagnostic and therapeutic applications.

These aptamers market have improved their investment in healthcare infrastructure and facilities. Due to the high effectiveness of sleep apnea, machines only work in a small percentage of cases due to their dependence on consistent use and medical supervision. Due to the increase in number of applications of Aptamers in healthcare sectors, the increasing investment in this market is expected to offer growth opportunities in the market.

Latest Trends

Diagnostics Segment is Expected to Witness a Healthy Growth Rate Over the Forecast Period

The most important factor in the treatment of any disease, especially viral, is proper diagnosis. Aptamer technology has seen a dramatic rise in demand and use over the last few years. Aptamers are being used for a variety of diagnostic and therapeutic purposes. Many strategies against viruses are being investigated in a definitive and conclusive way by using aptamers.

Regional Analysis

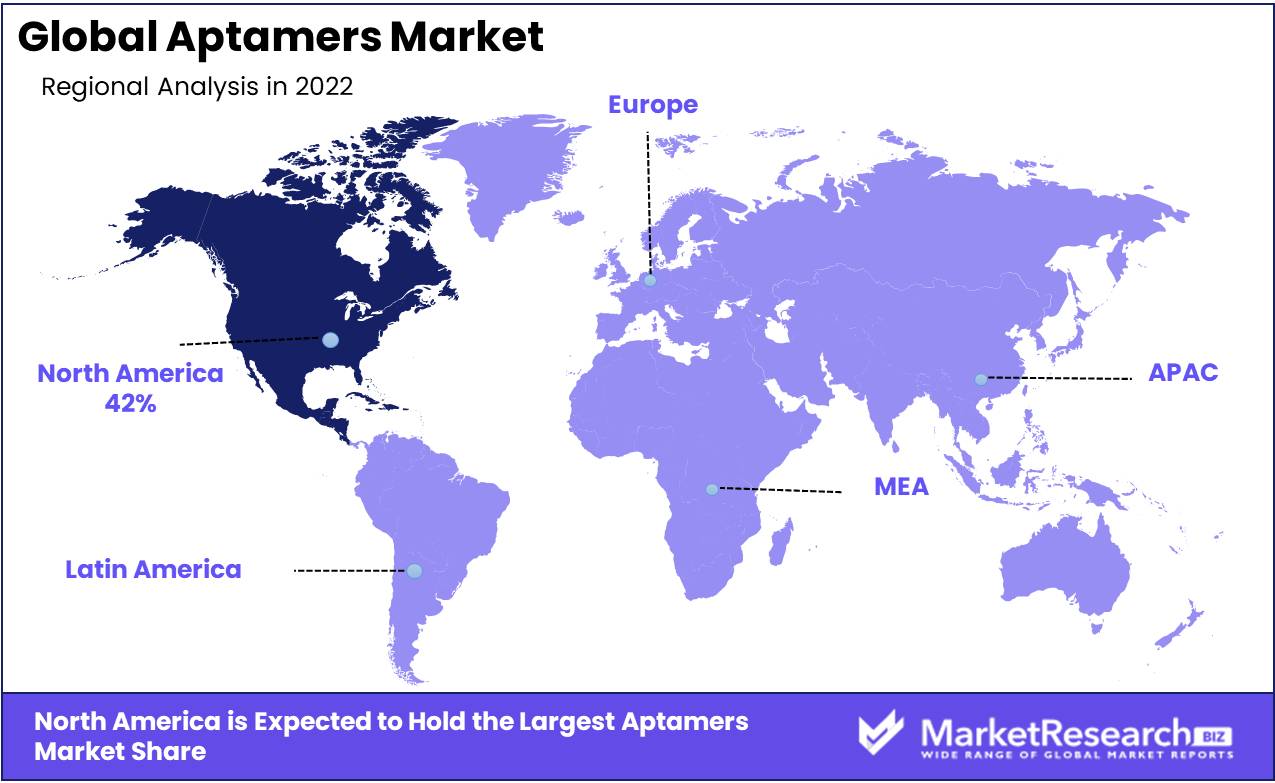

North America Dominates the Market and is Expected to Do the Same in the Forecast Period

North America was the dominant aptamers market and held the largest revenue share of 42%. Strong healthcare infrastructure, rising interest in research laboratories, and rising prevalence of chronic illnesses are major reasons for North America's dominance in the aptamers market. The Asia Pacific market will be the fastest growing during the forecast period. Approval of new aptamer products in the region has contributed to the region's growth. Research and development is the most crucial area for aptamers in North America.

Research applications account for a significant portion of the market's demand. This is also responsible for generating revenue in the aptamers market. The acceptance of personalized medicine also drives the market's growth. In the past ten years, aptamers have rapidly evolved and now target a wide range of molecules involved in tumor progression or metastasis.

Key Regions and Countries

North America

- US

- Canada

- Mexico

Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

Emerging key players are focused on a variety of strategic policies to develop their respective businesses in foreign markets. Several enteral feeding devices market companies are concentrating on expanding their existing operations and R&D facilities. Furthermore, businesses in the enteral feeding device market are developing new products and portfolio expansion strategies through investments and mergers, and acquisitions. In addition, several key players are now focusing on different marketing strategies, such as spreading awareness about natural ingredients, which is boosting the target products' growth.

With many local and regional players' presence, the enteral feeding device market is fragmented. Market players are subject to intense competition from top aptamers market players, particularly those with strong brand recognition and high distribution networks. Companies have gained various expansion strategies, such as partnerships and product launches, to stay on top of the market.

Top Key Players in Aptamers Market

- SomaLogic Inc.

- Vivonics Inc.

- IBA GmbH

- Aptus Biotech S.L.

- Vivonics Inc.

- Base Pair Biotechnologies Inc.

- Baush Health Companies Inc.

- KANEKA CORPORATION

- TriLink BioTechnologies

- Other Key Players

Recent Development

In August 2021: Aptamer Group collaborated with ProAxsis Limited. The agreement states that Aptamer Group produced validated Optimer ligands for ProAxsis' diagnostics.

In July 2021: Aptamer Sciences announced the selection of candidate material to a 'Corona-19 viral neutralizing aptamer’ as a non-clinical program to support the COVID-19 treatment group and vaccine new drug design group projects.

Report Scope:

Report Features Description Market Value (2022) USD 2.2 Bn Forecast Revenue (2032) USD 13.0 Bn CAGR (2023-2032) 20% Base Year for Estimation 2022 Historic Period 2016-2022 Forecast Period 2023-2032 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Type: Nucleic Acid and Peptides; By Application: Diagnostics, Therapeutics, Research & Development, and Other Applications; By End-User: Pharmaceutical & Biotechnological Companies, Contract Research Organisations, Academic & Government Research Organisations, and Other End-Users Regional Analysis North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape SomaLogic Inc., Vivonics Inc., IBA GmbH, Aptus Biotech S.L., Vivonics Inc., Base Pair Biotechnologies Inc., Baush Health Companies Inc., KANEKA CORPORATION, TriLink BioTechnologies, Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- SomaLogic Inc.

- Vivonics Inc.

- IBA GmbH

- Aptus Biotech S.L.

- Vivonics Inc.

- Base Pair Biotechnologies Inc.

- Baush Health Companies Inc.

- KANEKA CORPORATION

- TriLink BioTechnologies

- Other Key Players

Our Clients

View Our Licence Options