Alpha Emitter Market By Type of Radionuclide (Radium (Ra-223), Lead (Pb-212), Actinium (Ac-225), Bismuth-213, Astatine-211, Other Types), By Application (Bone Metastases, Neuroendocrine Tumors, Prostate Cancer, Ovarian Cancer, Other Applications), By Source (Natural Sources, Artificially Produced Sources, Other Sources), By End-User (Hospitals, Diagnostic Centers, Specialty Clinics, Other End-Users), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

46170

-

April 2024

-

136

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

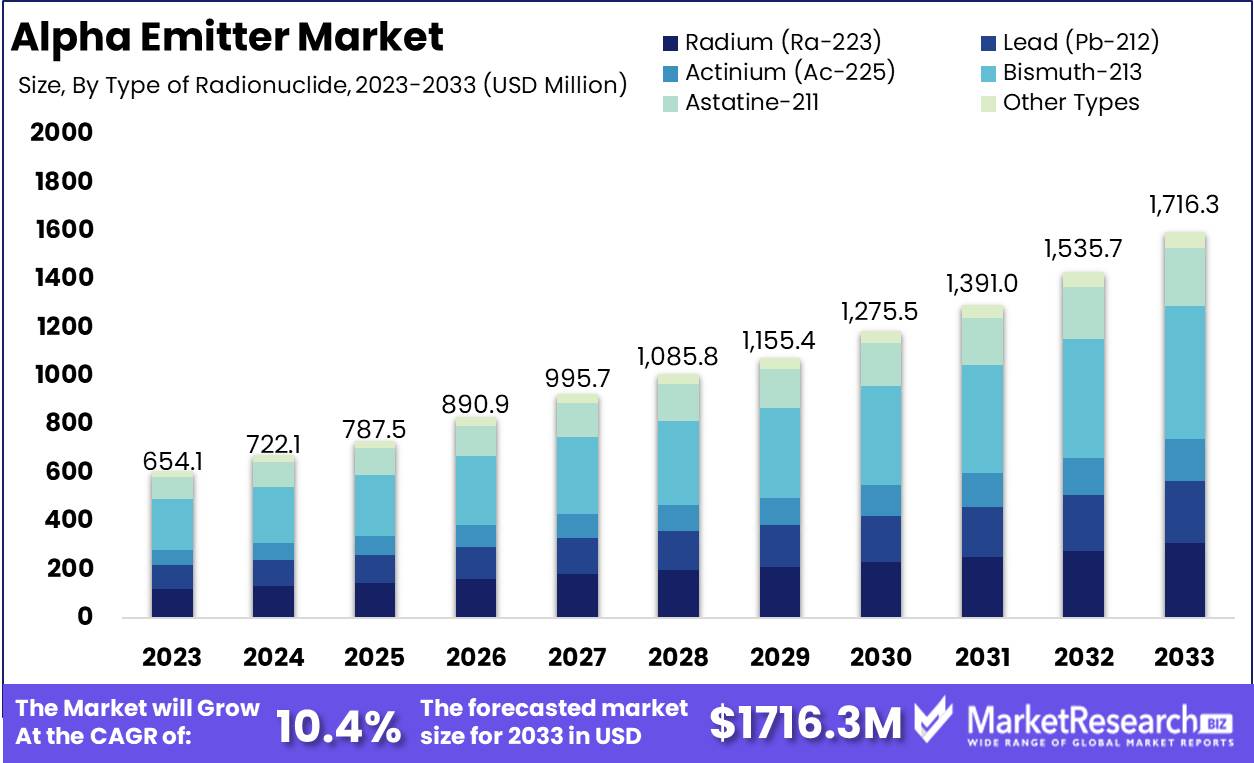

The Global Alpha Emitter Market was valued at USD 654.1 Mn in 2023. It is expected to reach USD 1716.3 Mn by 2033, with a CAGR of 10.4% during the forecast period from 2024 to 2033.

The Alpha Emitter Market refers to the segment within the radiation detection and measurement industry that focuses on alpha-emitting radionuclides and their associated detection technologies. Alpha emitters are radioactive isotopes that emit alpha particles, consisting of two protons and two neutrons, making them highly ionizing but with limited penetrating power. This market encompasses a range of applications including environmental monitoring, nuclear power plants, healthcare, and industrial safety. The demand for alpha emitter detection solutions is driven by stringent regulatory standards, growing concerns over radiation exposure, and the increasing adoption of nuclear technologies across various sectors.

The Alpha Emitter Market demonstrates a promising trajectory, marked by a confluence of factors shaping its growth landscape. With the ubiquity of alpha-emitting radionuclides in diverse sectors such as healthcare, nuclear power generation, and environmental monitoring, the market is witnessing heightened demand for advanced detection and measurement solutions. Key drivers include stringent regulatory frameworks mandating radiation safety standards, heightened awareness regarding environmental contamination, and the imperative for precise monitoring in nuclear facilities.

The intrinsic properties of alpha particles, characterized by high ionization but limited penetration, underscore their significance in applications necessitating localized detection. Notably, the alpha decay of Uranium-238 (U-238) to produce Thorium-234 (Th-234) and an alpha particle, with an energy release of approximately 4.27 MeV, augments the market's appeal by elucidating the fundamental processes underpinning alpha radiation detection. As industries pivot towards sustainable practices and stringent safety protocols, the Alpha Emitter Market is poised to witness steady expansion, underpinned by technological advancements fostering enhanced sensitivity, precision, and real-time monitoring capabilities.

Integrating the data on Uranium-238 (U-238) into the Alpha Emitter Market analysis enriches our understanding of the market dynamics. The alpha decay process of U-238, yielding Thorium-234 (Th-234) alongside an alpha particle with an energy release of approximately 4.27 MeV, underscores the significance of alpha radiation detection technologies. This data elucidates the fundamental mechanisms governing alpha particle emissions, informing the development of innovative detection solutions tailored to diverse applications.

Key Takeaways

- Market Growth: The Global Alpha Emitter Market was valued at USD 654.1 Mn in 2023. It is expected to reach USD 1716.3 Mn by 2033, with a CAGR of 10.4% during the forecast period from 2024 to 2033.

- By Type of Radionuclide: Bismuth-213 leads with 32%, favored for its effectiveness in targeted alpha therapy for cancer treatment.

- By Application: Bone metastases applications dominate at 37.4%, highlighting the demand for effective treatments in metastatic cancer management.

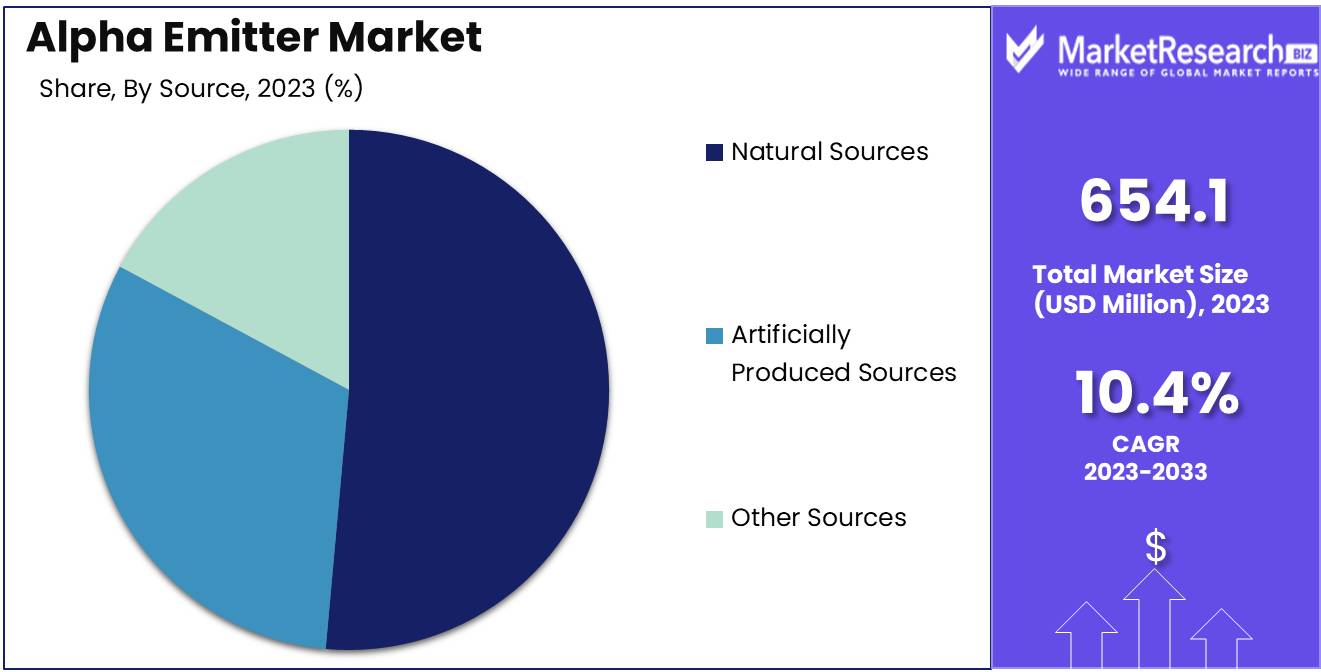

- By Source: Natural sources account for 54% of the market, reflecting the reliance on naturally occurring radionuclides for alpha emitter production.

- By End-User: Specialty clinics hold 47% of the market, emphasizing their role in administering advanced alpha emitter therapies.

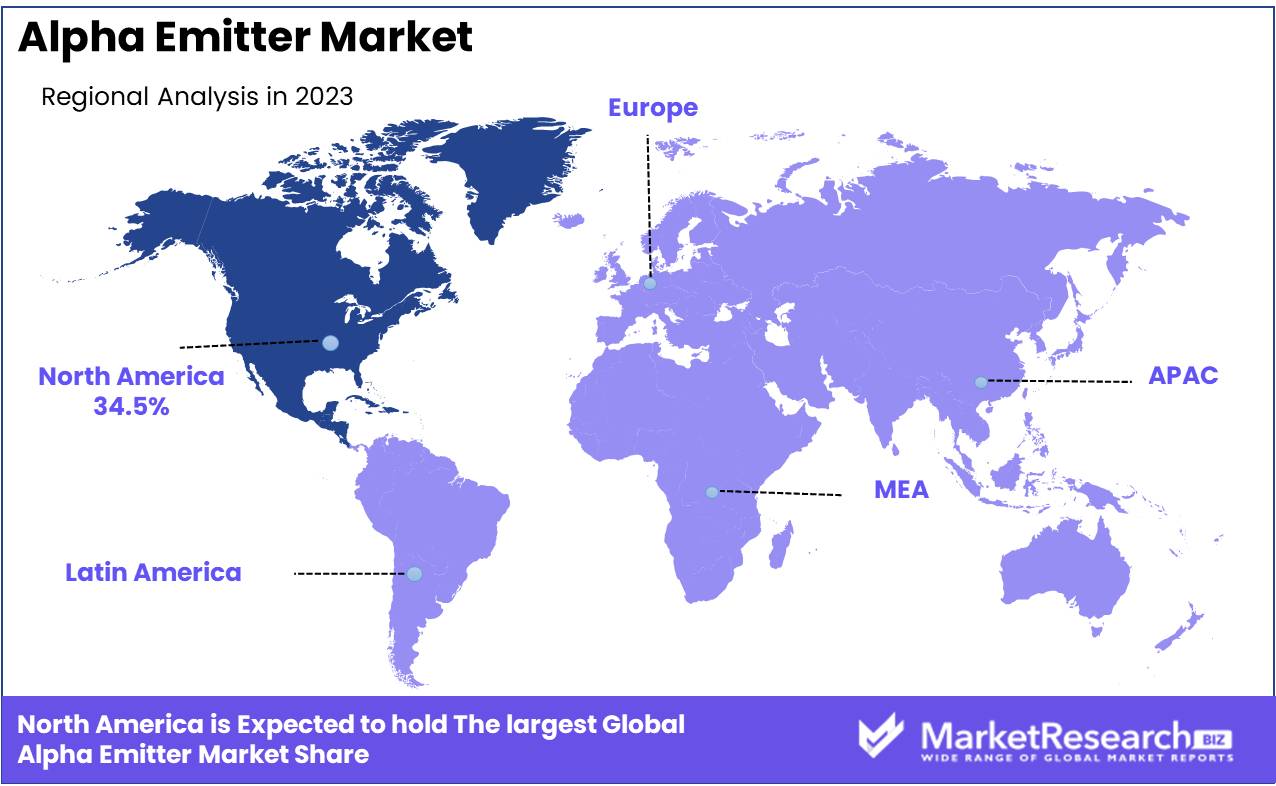

- Regional Dominance: North America holds a significant share of 34.5% in the alpha emitter market, driven by advanced healthcare infrastructure and high demand for innovative cancer therapies.

- Growth Opportunity: The alpha emitter market presents promising growth prospects through research advancements in targeted therapies, expanded applications in oncology, and increased collaboration with pharmaceutical companies for drug development.

Driving factors

Advancements in Cancer Therapy

The constant evolution of cancer therapy with alpha emitters is a pivotal driving force behind the growth of the Alpha Emitter Market. As researchers delve deeper into the mechanisms of these emitters, they uncover novel applications and refine existing treatment protocols. Advancements such as improved targeting techniques, enhanced efficacy, and reduced toxicity levels not only expand the scope of alpha emitter therapy but also bolster its acceptance among clinicians and patients.

Recent studies have demonstrated the efficacy of targeted alpha therapy in treating various types of cancer, including prostate, ovarian, and pancreatic cancers. With each breakthrough, the market experiences a surge in demand for alpha emitter-based treatments, propelling its growth trajectory forward.

Clinical Development for Radiotherapy

The burgeoning opportunities in clinical development for radiotherapy, particularly with alpha emitters, play a crucial role in shaping the Alpha Emitter Market landscape. As the field of radiotherapy continues to advance, fueled by technological innovations and deeper insights into tumor biology, researchers are increasingly exploring the potential of alpha emitters in clinical settings. Clinical trials investigating the efficacy and safety of alpha emitter-based therapies across different cancer types are on the rise, attracting significant attention from both pharmaceutical companies and healthcare providers.

These trials not only pave the way for regulatory approvals but also generate valuable data that reinforces the market's growth prospects. Moreover, the integration of alpha emitters into multimodal treatment regimens further expands their utility, positioning them as indispensable tools in the fight against cancer.

Restraining Factors

Damage to Healthy Cells from Radiation

While the use of alpha emitters in cancer therapy holds immense promise, the potential damage to healthy cells from radiation remains a significant concern shaping the Alpha Emitter Market. Unlike conventional treatments, which may cause collateral damage to surrounding tissues, alpha emitters have the advantage of delivering highly localized radiation, minimizing off-target effects. However, despite this advantage, the inherent cytotoxicity of alpha particles poses a risk of unintended harm to healthy cells within the vicinity of the tumor.

Mitigating this risk requires a delicate balance between maximizing therapeutic efficacy and minimizing adverse effects on healthy tissues. Thus, ongoing research focuses on optimizing treatment protocols, refining targeting strategies, and leveraging innovative delivery systems to enhance the therapeutic window of alpha emitter-based therapies. Addressing these challenges not only improves patient outcomes but also fosters greater confidence among clinicians and regulators, driving the market's sustained growth.

Challenges in Biodistribution and Dose Distribution

Challenges in biodistribution and dose distribution present notable hurdles in the widespread adoption of alpha emitter-based therapies, influencing the trajectory of the Alpha Emitter Market. Achieving precise biodistribution, ensuring that therapeutic radionuclides reach the intended target while minimizing accumulation in non-target organs, is critical for optimizing treatment outcomes and reducing off-target toxicity. Similarly, accurately delivering therapeutic doses to tumor sites while sparing healthy tissues requires innovative approaches in treatment planning and delivery.

Challenges such as variability in patient anatomy, tumor heterogeneity, and differences in radionuclide pharmacokinetics further complicate dose distribution, necessitating personalized treatment approaches and real-time monitoring techniques. Overcoming these challenges demands interdisciplinary collaboration among researchers, clinicians, and industry stakeholders to develop robust solutions that enhance the safety and efficacy of alpha emitter-based therapies.

By Type of Radionuclide Analysis

Bismuth-213 secured over 32% of the Alpha Emitter Market,

In 2023, Bismuth-213 held a dominant market position in the Alpha Emitter Market's segment by type of radionuclide, capturing more than a 32% share. Bismuth-213's prominence was attributed to its significant therapeutic potential and its proven efficacy in targeted alpha therapy (TAT) applications.

Radium (Ra-223) emerged as another notable player in this segment, offering promising results in the treatment of bone metastases associated with advanced prostate cancer. With its ability to selectively target cancerous cells while minimizing damage to surrounding healthy tissue, Ra-223 garnered considerable attention from both clinicians and patients alike.

Lead (Pb-212) secured a respectable position within the market segment, leveraging its unique properties for various medical and research purposes. Pb-212's high energy emissions make it suitable for targeted cancer treatments and diagnostic imaging applications, contributing to its steady market presence.

Actinium (Ac-225) also made its mark in the alpha emitter market, recognized for its potent alpha radiation and its potential in treating a range of cancers, including leukemia and prostate cancer. The growing interest in alpha-emitting isotopes for cancer therapy further bolstered Ac-225's market standing.

Astatine-211, though holding a smaller market share compared to its counterparts, demonstrated promising prospects in targeted alpha therapy research and development. Its short half-life and high-energy emissions make it suitable for precise cancer treatment, driving interest among researchers and pharmaceutical companies.

Other types of radionuclides within the segment collectively contributed to the market landscape, offering diverse applications in medical imaging, radiotherapy, and nuclear medicine research.

By Application Analysis

In the Alpha Emitter Market, Bone Metastases led the segment by application in 2023, commanding over 37.4% share.

In 2023, Bone Metastases held a dominant market position in the Alpha Emitter Market's segment by application, capturing more than a 37.4% share. This significant market share was attributed to the rising prevalence of bone metastases associated with various cancers, including prostate, breast, and lung cancer, driving the demand for effective therapeutic solutions.

Neuroendocrine Tumors emerged as another prominent application within the segment, leveraging the targeted nature of alpha emitters to effectively destroy tumor cells while minimizing systemic toxicity. The increasing incidence of neuroendocrine tumors and the limited treatment options available further propelled the adoption of alpha emitter-based therapies in this segment.

Prostate Cancer represented a substantial market opportunity within the alpha emitter segment, driven by the need for advanced treatment modalities for metastatic prostate cancer. Alpha emitter therapies, such as Radium-223, demonstrated efficacy in prolonging survival and improving quality of life in patients with metastatic castration-resistant prostate cancer, contributing to the segment's growth.

Ovarian Cancer, although holding a smaller market share compared to bone metastases and prostate cancer, presented significant growth potential fueled by the exploration of novel treatment approaches. Alpha emitter-based therapies offered promise in addressing the challenges associated with recurrent or refractory ovarian cancer, encouraging investment and research in this application area.

Other applications within the segment encompassed a wide range of cancer types and non-oncological conditions, including lymphoma, melanoma therapeutics, and bone pain palliation. The versatility of alpha emitter therapies in targeting various cancer types and their potential applications in pain management and palliative care contributed to the segment's overall growth trajectory.

By Source Analysis

Natural Sources dominated the Alpha Emitter Market's segment by source, claiming over 54% share.

In 2023, Natural Sources held a dominant market position in the Alpha Emitter Market's segment by source, capturing more than a 54% share. This significant market share underscored the enduring appeal and widespread availability of naturally occurring alpha-emitting radionuclides, which are often derived from elements such as radium, thorium, and uranium.

Artificially Produced Sources emerged as another noteworthy segment within the market, albeit with a smaller market share compared to natural sources. These sources encompassed a range of artificially produced alpha-emitting radionuclides, including those synthesized through nuclear reactions or particle bombardment techniques. Despite their lower market share, artificially produced sources played a vital role in addressing specific clinical and research needs, particularly in the development of novel radiopharmaceuticals and experimental applications.

Other Sources encompassed a variety of alternative alpha-emitting materials, including those derived from rare-earth elements, actinides, and synthetic compounds. While representing a minority share of the market, these sources offered unique properties and applications that complemented those of natural and artificially produced radionuclides, contributing to the overall diversity and innovation within the alpha emitter market.

By End-User Analysis

Specialty Clinics dominated the Alpha Emitter Market's segment by end-user, with over 47% share.

In 2023, Specialty Clinics held a dominant market position in the Alpha Emitter Market's segment by end-user, capturing more than a 47% share. This substantial market share underscored the pivotal role of specialty clinics in delivering specialized care and innovative treatment modalities, including targeted alpha therapy (TAT), to patients with various cancers and other medical conditions.

Hospitals emerged as another significant end-user within the segment, leveraging their comprehensive infrastructure and multidisciplinary approach to healthcare delivery. Hospitals offered a wide range of medical services, including diagnostics, surgery, and radiotherapy, making them key stakeholders in the adoption and utilization of alpha emitter-based therapies for cancer treatment and management.

Diagnostic Centers represented a vital component of the alpha emitter market, providing essential imaging and diagnostic services to aid in the detection, staging, and monitoring of cancerous lesions and other diseases. The integration of alpha emitter-based imaging techniques, such as alpha-particle emission tomography (αPET), into diagnostic workflows contributed to the segment's growth and expansion.

Other End-Users encompassed a diverse array of healthcare facilities, research institutions, and academic centers involved in the provision of healthcare services, medical research, and education.

Key Market Segments

By Type of Radionuclide

- Radium (Ra-223)

- Lead (Pb-212)

- Actinium (Ac-225)

- Bismuth-213

- Astatine-211

- Other Types

By Application

- Bone Metastases

- Neuroendocrine Tumors

- Prostate Cancer

- Ovarian Cancer

- Other Applications

By Source

- Natural Sources

- Artificially Produced Sources

- Other Sources

By End-User

- Hospitals

- Diagnostic Centers

- Specialty Clinics

- Other End-Users

Growth Opportunity

Capitalizing on Growing Cancer Prevalence

The global Alpha Emitter Market stands at the precipice of unprecedented growth opportunities in 2024, buoyed by a convergence of factors propelling demand for innovative cancer therapies. One of the primary drivers is the escalating prevalence of cancer worldwide, which continues to fuel the need for advanced treatment modalities. With cancer incidence rates on the rise across demographics, there is a pressing imperative to develop targeted and efficacious therapies to address the burgeoning disease burden.

Alpha emitters, with their ability to deliver potent radiation directly to cancer cells while minimizing systemic toxicity, are poised to play a pivotal role in meeting this critical need. Supported by robust clinical evidence and regulatory approvals, alpha emitter-based therapies are gaining traction as frontline options in the oncology armamentarium, driving market expansion.

Increased R&D Investments

Another catalyst propelling the growth of the Alpha Emitter Market is the surge in research and development (R&D) investments aimed at enhancing treatment efficacy and expanding therapeutic indications. Pharmaceutical companies, academic institutions, and government agencies are intensifying their efforts to innovate and refine alpha emitter-based therapies through strategic collaborations and funding initiatives.

These investments are directed towards advancing targeted delivery systems, refining dosimetry algorithms, and elucidating the underlying mechanisms of action to optimize treatment outcomes. The emergence of novel radionuclides and radiopharmaceuticals, coupled with advancements in imaging technologies, is broadening the scope of alpha emitter applications across a spectrum of cancer types. As these R&D endeavors translate into clinical successes and commercialization milestones, the Alpha Emitter Market is poised to witness accelerated growth, ushering in a new era of precision oncology and improved patient outcomes.

Latest Trends

Advancements in Targeted Alpha Therapy (TAT)

As we navigate through 2024, the global Alpha Emitter Market is witnessing a paradigm shift fueled by advancements in Targeted Alpha Therapy (TAT). TAT represents a transformative approach to cancer treatment, harnessing the immense cytotoxic potential of alpha emitters to precisely target and eradicate malignant cells. Recent breakthroughs in radiopharmaceutical development, coupled with innovative targeting strategies, have propelled TAT to the forefront of precision oncology.

By leveraging tumor-specific antigens and molecular markers, researchers are enhancing the selectivity and efficacy of alpha emitter-based therapies, paving the way for personalized treatment regimens tailored to individual patients. Moreover, ongoing clinical trials across a spectrum of cancer types are generating robust evidence supporting the therapeutic value of TAT, driving increased adoption and market growth.

Increasing Adoption of Nuclear Medicine

Another notable trend shaping the Alpha Emitter Market in 2024 is the escalating adoption of nuclear medicine approaches, underscoring the growing recognition of alpha emitters as indispensable tools in the oncology arsenal. Nuclear medicine techniques, including positron emission tomography (PET) and single-photon emission computed tomography (SPECT), play a pivotal role in disease diagnosis, treatment planning, and response assessment. The integration of alpha emitter-based radiopharmaceuticals into nuclear medicine workflows offers unparalleled opportunities for precision imaging and targeted therapy delivery.

The expanding infrastructure for radiopharmaceutical production and distribution worldwide is facilitating broader access to alpha emitter-based treatments, driving market expansion. As healthcare systems increasingly embrace nuclear medicine as a cornerstone of modern oncology, the Alpha Emitter Market is poised for sustained growth, fueled by the synergistic convergence of diagnostic and therapeutic innovations.

Regional Analysis

North America dominates the alpha emitter market, holding a 34.5% share.

The alpha emitter market demonstrates varied regional dynamics, with North America at the forefront, commanding 34.5% of the market share. This region's leadership is attributed to its advanced healthcare infrastructure, substantial investment in oncology research, and high prevalence of cancer. The United States, in particular, plays a pivotal role due to its significant funding for medical research and favorable regulatory environment supporting novel radiopharmaceutical therapies.

Europe follows closely, characterized by robust healthcare systems, extensive research initiatives, and strong government support for cancer treatment advancements. Key contributors include Germany, France, and the UK, which are actively involved in clinical trials and the adoption of innovative cancer therapies. The European market is also driven by stringent regulatory frameworks aimed at improving patient outcomes and reducing healthcare costs.

The Asia Pacific region is experiencing rapid growth, driven by increasing healthcare expenditures, rising cancer incidences, and expanding medical infrastructure in countries like China, India, and Japan. Government initiatives to enhance healthcare services and the growing awareness of advanced treatment options further propel the market in this region.

In the Middle East & Africa, the market is gradually expanding due to improving healthcare facilities and rising investments in medical technology, although it starts from a smaller base compared to other regions. Countries within the Gulf Cooperation Council (GCC) are particularly focusing on modernizing their healthcare systems and adopting advanced cancer treatments.

Latin America shows steady market growth, with Brazil and Argentina leading the way. Enhancements in healthcare services, growing adoption of cutting-edge cancer therapies, and increasing investments in medical research contribute to the market's expansion in this region. Overall, North America's substantial market share underscores its leading position, while Europe and Asia Pacific display significant growth potential driven by their respective healthcare advancements and economic conditions.

Key Regions and Countries

North America

- US

- Canada

- Mexico

Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

In 2024, the global alpha emitter market is witnessing dynamic growth, with key players shaping the industry landscape through innovative therapies and strategic collaborations. Among these, Alpha Tau Medical Ltd. stands out as a frontrunner, leveraging its groundbreaking alpha radiation technology, Alpha DaRT, for targeted cancer treatment. This approach holds promise for improving outcomes in various cancer types while minimizing damage to healthy tissue, positioning Alpha Tau Medical Ltd. as a key innovator in the field.

IBA Worldwide, with its expertise in particle therapy solutions, plays a pivotal role in advancing alpha emitter-based treatments. Its focus on precision and efficacy aligns with the growing demand for personalized cancer therapies, driving adoption and market expansion.

NorthStar Medical Radioisotopes emerges as a key player in the production and supply of medical isotopes, including alpha emitters, addressing the critical need for reliable and sustainable radioisotope sources in healthcare.

Additionally, companies like RadioMedix, Fusion Pharmaceuticals Inc., and Actinium Pharmaceuticals, Inc., are making significant strides in developing novel alpha emitter-based radiopharmaceuticals for targeted cancer therapy, catering to unmet medical needs and expanding treatment options for patients worldwide.

Collaborations between pharmaceutical giants like Bayer AG, Novartis International AG, and emerging biotech firms such as Eckert & Ziegler and Curium Pharma signify a growing interest and investment in alpha emitter technologies. These partnerships facilitate the development and commercialization of next-generation therapies, driving innovation and market growth.

Telix Pharmaceuticals Limited, alongside other key players, contributes to the diversification of the alpha emitter market by exploring applications beyond oncology, including neurology and cardiology, broadening the scope of alpha radiation-based interventions.

Market Key Players

- Alpha Tau Medical Ltd.

- IBA Worldwide

- NorthStar Medical Radioisotopes

- RadioMedix

- Bayer AG

- Orano Med

- Novartis International AG

- Fusion Pharmaceuticals Inc.

- Actinium Pharmaceuticals, Inc.

- Eckert & Ziegler

- Curium Pharma

- Telix Pharmaceuticals Limited

- Other Key Players

Recent Development

- In May 2024, Radiopharmaceuticals include AstraZeneca's acquisition of Fusion ($2.5B) and Novartis's purchase of Mariana Oncology ($1B upfront), indicating big pharma's interest in advancing oncology therapeutics.

- In March 2024, Orano Med pioneers Europe's first TAT facility, advancing targeted alpha therapy. Promising Phase II data for AlphaMedix and expansion plans signal significant growth in radioligand therapeutics.

Report Scope

Report Features Description Market Value (2023) USD 654.1 Mn Forecast Revenue (2033) USD 1716.3 Mn CAGR (2024-2033) 10.4% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type of Radionuclide (Radium (Ra-223), Lead (Pb-212), Actinium (Ac-225), Bismuth-213, Astatine-211, Other Types), By Application (Bone Metastases, Neuroendocrine Tumors, Prostate Cancer, Ovarian Cancer, Other Applications), By Source (Natural Sources, Artificially Produced Sources, Other Sources), By End-User (Hospitals, Diagnostic Centers, Specialty Clinics, Other End-Users) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Alpha Tau Medical Ltd., IBA Worldwide, NorthStar Medical Radioisotopes, RadioMedix, Bayer AG, Orano Med, Novartis International AG, Fusion Pharmaceuticals Inc., Actinium Pharmaceuticals, Inc., Eckert & Ziegler, Curium Pharma, Telix Pharmaceuticals Limited, Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Alpha Tau Medical Ltd.

- IBA Worldwide

- NorthStar Medical Radioisotopes

- RadioMedix

- Bayer AG

- Orano Med

- Novartis International AG

- Fusion Pharmaceuticals Inc.

- Actinium Pharmaceuticals, Inc.

- Eckert & Ziegler

- Curium Pharma

- Telix Pharmaceuticals Limited

- Other Key Players

Our Clients

View Our Licence Options