AI in Mental Health Market By Technology (Natural Language Processing , Deep Learning and Machine Learning, Context-Aware Computing, Others), By Component (Software-as-a-Service, Hardware), By End-User (Hospitals and Clinics, Mental Health Centers, Research Institutions, Others), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

51291

-

September 2024

-

300

-

-

This report was compiled by Vishwa Gaul Vishwa is an experienced market research and consulting professional with over 8 years of expertise in the ICT industry, contributing to over 700 reports across telecommunications, software, hardware, and digital solutions. Correspondence Team Lead- ICT Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

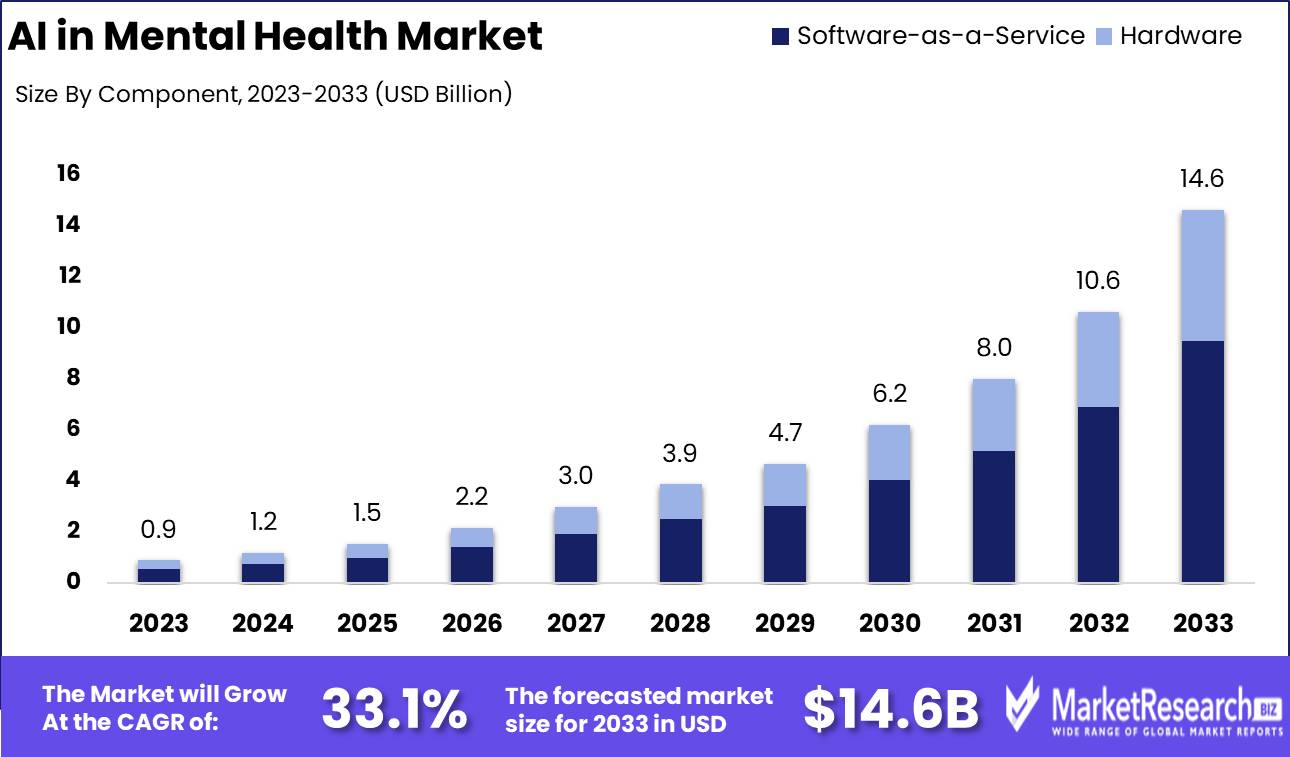

The AI in Mental Health Market was valued at USD 0.9 billion in 2023. It is expected to reach USD 14.6 billion by 2033, with a CAGR of 33.1% during the forecast period from 2024 to 2033.

The AI in Mental Health Market encompasses integrating artificial intelligence technologies into mental health services, facilitating enhanced diagnostic capabilities, personalized treatment plans, and improved patient outcomes. This market includes AI-driven applications such as chatbots, virtual therapy platforms, and predictive analytics tools that assist healthcare professionals in identifying mental health disorders and tailoring interventions.

The integration of artificial intelligence (AI) into the mental health sector is poised for significant transformation, driven by a confluence of rising mental health disorders, increased accessibility to care, and ongoing advancements in technology. Recent statistics indicate that approximately 1 in 5 adults in the U.S. experience mental illness, underscoring the urgent need for scalable solutions. AI applications, such as chatbots and predictive analytics, are emerging as vital tools to enhance therapeutic interventions and provide timely support.

Furthermore, AI-driven platforms can facilitate access to mental health resources, particularly in underserved communities, thereby addressing disparities in care delivery. As these technologies evolve, they are expected to be critical in optimizing treatment pathways and improving patient outcomes.

However, the growth of AI in the mental health market is not without challenges. Data privacy concerns remain a paramount issue, as sensitive patient information must be safeguarded to maintain trust in AI systems. According to industry forecasts, the market is anticipated to grow at a compound annual growth rate (CAGR) of over 30% in the next five years, reflecting a burgeoning demand for innovative mental health solutions. The continued growth of AI in this domain will largely depend on addressing these privacy issues while ensuring regulatory compliance. In summary, the potential of AI to revolutionize mental health care is considerable, yet its success will hinge on balancing technological advancements with ethical considerations and user trust.

Key Takeaways

- Market Growth: The AI in Mental Health Market was valued at USD 0.9 billion in 2023. It is expected to reach USD 14.6 billion by 2033, with a CAGR of 33.1% during the forecast period from 2024 to 2033.

- By Technology: NLP dominated AI in mental health technology advancements with a 39.6% share.

- By Component: SaaS dominated AI in Mental Health's component segment with a 65.7% share.

- By End-User: Hospitals and Clinics dominated AI in the Mental Health Market with a 40% share.

- Regional Dominance: North America dominates the AI in Mental Health market with 42.0% largest market share.

- Growth Opportunity: The global AI in the mental health market will experience significant growth, driven by advancements in machine learning, deep learning, and the expansion of SaaS-based mental health platforms.

Driving factors

Rising Prevalence of Mental Health Disorders Accelerates Market Demand for AI Solutions

The increasing prevalence of mental health disorders is a primary driver for the growth of AI in the mental health market. According to the World Health Organization (WHO), approximately 1 in 8 people globally lives with a mental health condition, and the number continues to rise. This growing burden of mental health issues, such as anxiety, depression, and stress-related disorders, is placing unprecedented pressure on healthcare systems and mental health professionals. As traditional methods struggle to meet the rising demand for mental health services, AI-based solutions offer a scalable, efficient alternative for diagnosis, monitoring, and treatment. AI's ability to provide early detection through sentiment analysis, behavioral data interpretation, and predictive algorithms significantly enhances its attractiveness to both healthcare providers and patients. As a result, AI-powered mental health tools are increasingly being adopted to alleviate the strain on mental health services, facilitating market growth.

Expansion of Data Volumes and Complexity Fuels the Development of AI in Mental Health

The increasing size and complexity of healthcare datasets represent another significant growth catalyst for AI in the mental health market. With the proliferation of digital health records, wearables, mobile applications, and other digital tools, vast amounts of patient data ranging from clinical data to real-time behavioral and biometric data are being generated. AI thrives on such extensive datasets, enabling the development of more sophisticated algorithms capable of identifying nuanced patterns and correlations that may be imperceptible to human clinicians. These patterns assist in more accurate diagnoses, personalized treatment plans, and ongoing monitoring of mental health conditions.

For example, deep learning models can analyze structured and unstructured data from various sources (e.g., EHRs, social media, voice analysis) to provide a holistic understanding of a patient's mental health status. This surge in data complexity and volume significantly enhances AI's ability to predict outcomes, optimize care, and personalize interventions, driving market adoption.

Rising Adoption of AI-Based Solutions by Healthcare Providers and Patients Drives Market Growth

The increasing adoption of AI-based solutions in mental health is another pivotal factor contributing to market expansion. As healthcare providers and patients become more familiar with AI technologies and their benefits, there is growing acceptance of AI-driven applications for mental health diagnostics, monitoring, and treatment. These solutions offer several advantages, including increased accessibility to care through virtual consultations, enhanced diagnostic precision, and cost-effective personalized treatment options. According to a report, AI-based interventions have demonstrated significant efficacy in managing conditions such as depression and PTSD. As these technologies continue to evolve, their adoption is further spurred by advancements in natural language processing (NLP), machine learning (ML), and sentiment analysis, which allow for real-time analysis of patient emotions and mental health status through telehealth platforms and mobile apps. This increased adoption underscores the vital role of AI in transforming mental healthcare delivery, thus driving market growth.

Restraining Factors

Challenges of Integration with Existing Systems

One of the key restraining factors affecting the growth of AI in the mental health market is the difficulty in integrating AI solutions with existing healthcare systems. Many healthcare systems, especially in the mental health sector, operate using legacy software, electronic health record (EHR) systems, and traditional therapeutic methodologies that may not be fully compatible with advanced AI technologies. This lack of seamless integration creates significant challenges for the widespread adoption of AI in clinical environments.

Incompatibility between AI algorithms and current healthcare data formats can result in high implementation costs, delays in deployment, and complex adjustments required to align AI models with existing workflows. The necessity for specialized training for mental health professionals to effectively utilize AI tools adds another layer of complexity. The limited interoperability between AI platforms and legacy systems also raises concerns about data accuracy, continuity of care, and patient privacy, making healthcare providers hesitant to adopt AI at scale. According to industry analysis, integration challenges may account for a delayed adoption timeline, which could hamper the overall growth trajectory of AI solutions in mental health settings.

The healthcare industry as a whole is slow to adopt new technology due to stringent regulations and the need for validation of effectiveness, leading to a bottleneck for AI implementation. Therefore, despite the potential of AI to transform mental health diagnosis and treatment, the slow integration with current systems remains a major hurdle that restricts its rapid market expansion.

Subjectivity in Mental Health Diagnosis Limits AI Accuracy

The inherent subjectivity in mental health diagnosis presents a significant challenge for AI-based solutions. Unlike physical health conditions, where diagnoses are often based on objective data such as laboratory results or imaging, mental health diagnoses rely heavily on qualitative assessments of patient behavior, emotions, and self-reported symptoms. This subjectivity makes it difficult for AI algorithms to standardize and interpret data accurately across diverse patient populations.

AI models are typically designed to work on structured, quantifiable data, but mental health assessments often involve complex human emotions and subjective experiences, which can vary greatly between individuals. As a result, AI algorithms may struggle to provide accurate or consistent results, leading to concerns about their reliability in clinical practice. Mental health conditions such as depression, anxiety, and schizophrenia manifest differently depending on cultural, social, and individual factors, further complicating the creation of AI tools that can universally apply diagnostic criteria.

Moreover, the lack of consensus on diagnostic criteria within the mental health community itself exacerbates this problem. Various classification systems, such as the DSM-5 (Diagnostic and Statistical Manual of Mental Disorders) and ICD-11 (International Classification of Diseases), provide different frameworks for diagnosis, making it difficult for AI systems to establish a unified diagnostic approach. This contributes to skepticism among mental health professionals, limiting the willingness to incorporate AI into diagnostic procedures. The subjectivity in diagnosis could lead to biases in AI models and potential misdiagnoses, further restraining market growth.

By Technology Analysis

In 2023, NLP dominated AI in mental health technology advancements with a 39.6% share.

In 2023, Natural Language Processing (NLP) held a dominant market position in the "By Technology" segment of the AI in Mental Health Market, capturing more than 39.6% of the total market share. This can be attributed to the increasing demand for AI-driven solutions in mental health assessments, particularly through advanced text and speech recognition technologies, enabling more personalized and precise diagnoses and interventions. Following NLP, Deep Learning and Machine Learning accounted for a significant share, driven by their ability to process large datasets and identify patterns in patient behavior, leading to more effective therapeutic recommendations and predictive analytics.

Context-aware computing also demonstrated considerable growth, as it enhances the interaction between AI systems and users by factoring in environmental data, emotions, and contextual cues, further improving mental health treatment personalization. The Others category, encompassing various emerging technologies, contributed modestly to the market, focusing on experimental tools and platforms. Collectively, these technologies are shaping the evolution of AI in mental health by enhancing diagnostic accuracy, therapy customization, and early intervention strategies, fueling overall market expansion.

By Component Analysis

In 2023, SaaS dominated AI in Mental Health's component segment with a 65.7% share.

In 2023, Software-as-a-Service held a dominant market position in the By Component segment of AI in the Mental Health Market, capturing more than a 65.7% share. This substantial market share can be attributed to the growing preference for cloud-based platforms, offering scalable, cost-effective, and real-time solutions for mental health diagnostics and treatment. SaaS solutions have facilitated the integration of AI-driven tools such as chatbots, virtual therapists, and predictive analytics into existing healthcare frameworks, driving their widespread adoption among healthcare providers.

Conversely, Hardware accounted for a comparatively smaller portion of the market, with demand driven by the deployment of AI-enabled devices like wearable sensors and neuroimaging tools. While hardware solutions contribute to enhancing data collection and analysis, their high upfront costs and maintenance requirements limit their mass adoption relative to SaaS platforms. However, advancements in hardware capabilities are expected to foster increased adoption over the coming years, particularly in research-focused mental health settings.

By End-User Analysis

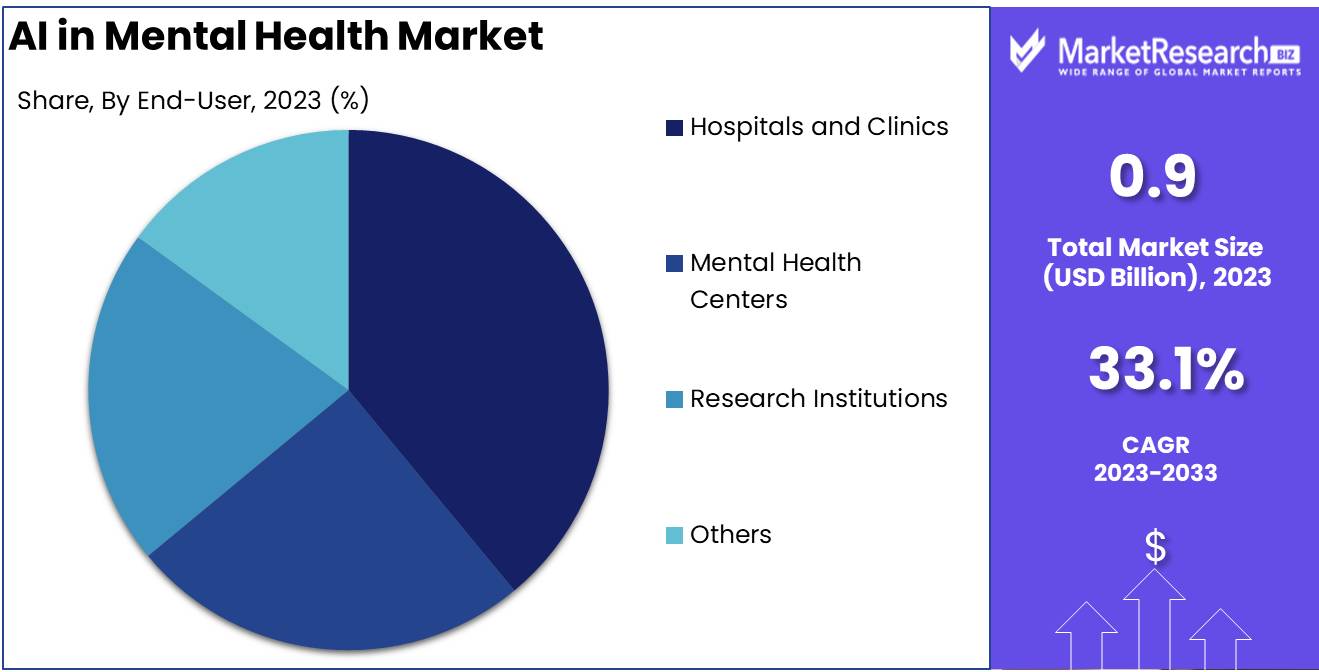

In 2023, Hospitals and Clinics dominated AI in the Mental Health Market with a 40% share.

In 2023, Hospitals and Clinics held a dominant market position in the By End-User segment of the AI in Mental Health Market, capturing more than a 40% share. This segment benefited from the integration of AI-driven tools to enhance diagnosis, patient care, and treatment personalization. The widespread adoption of AI in hospital settings, coupled with increased investment in healthcare technology, solidified its leadership within the market.

Mental Health Centers, comprising around 30% of the market, also saw substantial growth. AI applications in these centers facilitated improved mental health assessments, predictive analytics, and treatment recommendations, driving their market presence.

Research Institutions, holding approximately 20% share, utilized AI for advanced research in mental health disorders, clinical trials, and data analysis. Their role was critical in developing AI models, contributing to the innovation pipeline in mental health care.

The Others category, encompassing private practitioners, telemedicine providers, and rehabilitation centers, accounted for the remaining 10% share, largely driven by the increasing demand for AI-assisted remote care and mental health services. These end-users collectively contributed to the broader expansion of AI in the Mental Health market.

Key Market Segments

By Technology

- Natural Language Processing

- Deep Learning and Machine Learning

- Context-Aware Computing

- Others

By Component

- Software-as-a-Service

- Hardware

By End-User

- Hospitals and Clinics

- Mental Health Centers

- Research Institutions

- Others

Growth Opportunity

Machine Learning and Deep Learning Applications

The integration of ML and DL in mental health services presents a transformative growth opportunity. These technologies enable more accurate diagnosis, predictive analytics, and personalized treatment plans, enhancing the efficacy of mental health interventions. The demand for AI-driven mental health solutions, such as chatbots and virtual therapists, is expected to rise, leveraging ML algorithms to analyze patient data in real time. For instance, DL models can detect patterns in speech and behavior to predict mental health conditions with high accuracy, driving adoption across both healthcare providers and individual users.

Software-as-a-Service (SaaS) Solutions

SaaS-based mental health platforms represent another growth avenue for AI in this sector. These platforms offer scalable, cloud-based solutions that make mental health services more accessible and cost-effective. In 2024, SaaS solutions are anticipated to proliferate as mental health apps, online counseling platforms, and AI-enabled therapy solutions become more prevalent. The subscription-based model of SaaS allows continuous updates, ensuring users and providers access the latest AI capabilities, ultimately improving patient outcomes and expanding the market footprint.

Latest Trends

Integration of Wearable Devices and Mobile Apps

The integration of wearable devices and mobile applications into the mental health sector is poised to revolutionize the delivery of mental health services. These technologies enable continuous monitoring of users' physiological and psychological states, allowing for real-time data collection. The data gathered can be analyzed using advanced algorithms, facilitating personalized interventions. This trend not only enhances patient engagement but also empowers clinicians to make informed decisions based on comprehensive health data. As the technology becomes more accessible, the adoption of wearable devices and mobile applications is expected to accelerate, contributing to improved mental health outcomes.

Increasing Public Awareness and Interest in AI for Mental Health

The growing public awareness of mental health issues, coupled with an increased interest in AI-driven solutions, is significantly shaping the market landscape. Campaigns promoting mental health literacy have led to a greater understanding of AI applications in therapy, diagnosis, and support. This shift is reflected in the heightened demand for AI-based tools and services that provide accessible and affordable mental health care. As stakeholders, including healthcare providers and technology companies, continue to innovate and promote these solutions, it is anticipated that the integration of AI in mental health will expand, fostering a more supportive environment for individuals seeking help.

Regional Analysis

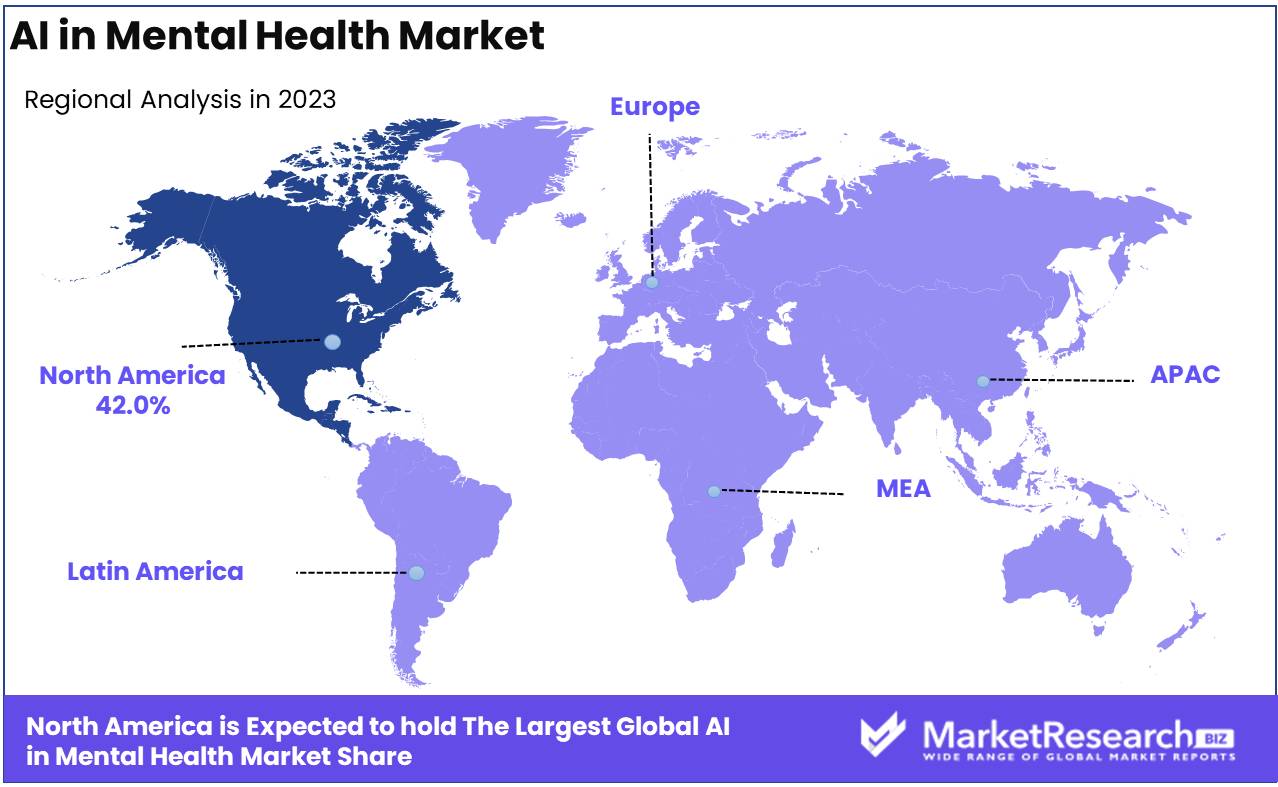

North America dominates the AI Mental Health market with 42.0% largest market share.

The AI in Mental Health market has been experiencing substantial growth across various regions, with North America emerging as the dominating market, accounting for approximately 42.0% of the global share in 2023. This dominance can be attributed to the high adoption rate of advanced technologies and significant investments in healthcare innovations. The presence of key players, such as Google and IBM, along with robust research and development activities, has propelled the market forward. In 2022, the North American AI in Mental Health market was valued at approximately USD 1.1 billion, and it is projected to reach USD 3.2 billion by 2030, reflecting a compound annual growth rate (CAGR) of 14.8%.

In Europe, the market is estimated to hold around 25% of the global share, driven by increasing mental health awareness and government initiatives aimed at integrating AI technologies into healthcare systems. The Asia Pacific region is witnessing rapid growth, with a CAGR of 16.2% projected through 2030, fueled by the rising prevalence of mental health disorders and the expanding digital health infrastructure.

The Middle East and Africa represent a smaller market share of approximately 10%, influenced by varying levels of healthcare infrastructure and technology adoption, while Latin America is expected to grow at a steady pace, accounting for about 8% of the market. Overall, the AI in Mental Health market exhibits strong potential across all regions, with North America leading the charge due to its innovative landscape and investment capabilities.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

The global AI in the Mental Health market is characterized by the strategic initiatives and innovative solutions offered by key players such as Wysa, Woebot Health, Ginger, Mindstrong Health, Marigold Health, Lyra Health, Bark Technologies, and Neuroflow. These companies are leveraging advanced artificial intelligence technologies to enhance mental health support and accessibility.

Wysa and Woebot Health are recognized for their chatbot-driven therapeutic interventions, employing natural language processing to engage users in real-time, and providing personalized support and coping strategies. Their focus on user-friendly interfaces has expanded access to mental health resources, particularly among younger demographics.

Ginger and Mindstrong Health are notable for their comprehensive mental health platforms, integrating AI-driven assessments with human support to deliver a hybrid care model. This approach enables continuous monitoring and tailored interventions, addressing diverse mental health needs effectively.

Marigold Health and Lyra Health emphasize workplace mental health solutions, utilizing AI to analyze employee data and facilitate proactive mental health management. By focusing on organizational well-being, these companies are shaping the future of workplace mental health services.

Bark Technologies and Neuroflow are pioneers in the prevention and early intervention of mental health issues, leveraging AI analytics to identify at-risk individuals and facilitate timely support. Their initiatives underscore the importance of integrating technology with clinical expertise.

Overall, the competitive landscape in the AI in Mental Health market is marked by innovation, strategic partnerships, and an emphasis on evidence-based solutions, positioning these companies as leaders in addressing the growing mental health crisis.

Market Key Players

- Wysa

- Woebot Health

- Ginger

- Mindstrong Health

- Marigold Health

- Lyra Health

- Bark Technologies

- Neuroflow

- Other Key Players

Recent Development

- In September 2024, The World Health Organization released a comprehensive study assessing the potential and challenges of AI in mental health services. The study highlights AI's role in improving service availability and efficiency, but it also emphasizes concerns over data privacy, algorithm bias, and the potential erosion of human interaction in mental health care. These findings encourage further research to develop ethical frameworks for the use of AI in mental health.

- In August 2024, Marigold Health, a Boston-based startup, used AI-powered chat support to create a personalized and peer-driven mental health support system. The platform leverages AI to augment patient engagement in community-based treatment by facilitating chat groups and providing wraparound services. This model has demonstrated the ability to scale support for behavioral health needs, making it more accessible to underserved populations.

- In July 2024, BrainSightAI, a company based in Bengaluru, India, developed an AI-powered platform using MRI-based imaging for psychiatric and neurological diagnosis. Their technology provides functional brain maps that assist clinicians in offering precise diagnoses and predicting treatment outcomes. The AI and machine learning algorithms help personalize mental health care by going beyond traditional symptomatic approaches to include digital phenotypes and biomarkers.

Report Scope

Report Features Description Market Value (2023) USD 0.9 Billion Forecast Revenue (2033) USD 14.6 Billion CAGR (2024-2032) 33.1% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Technology (Natural Language Processing, Deep Learning and Machine Learning, Context-Aware Computing, Others), By Component (Software-as-a-Service, Hardware), By End-User (Hospitals and Clinics, Mental Health Centers, Research Institutions, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Wysa, Woebot Health, Ginger, Mindstrong Health, Marigold Health, Lyra Health, Bark Technologies, Neuroflow, Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Wysa

- Woebot Health

- Ginger

- Mindstrong Health

- Marigold Health

- Lyra Health

- Bark Technologies

- Neuroflow

- Other Key Players

Our Clients

View Our Licence Options