Agriculture Sprayers Market By Type (Handheld, Self-Propelled, Tractor-Mounted, Trailed, Aerial, Backpack Sprayers), By Energy Source (Fuel based, Electric, Manual handling, Solar), By Application (Field Sprayers, Orchard Sprayers, Gardening Sprayers), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

10389

-

July 2024

-

162

-

-

This report was compiled by Shreyas Rokade Shreyas Rokade is a seasoned Research Analyst with CMFE, bringing extensive expertise in market research and consulting, with a strong background in Chemical Engineering. Correspondence Team Lead-CMFE Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

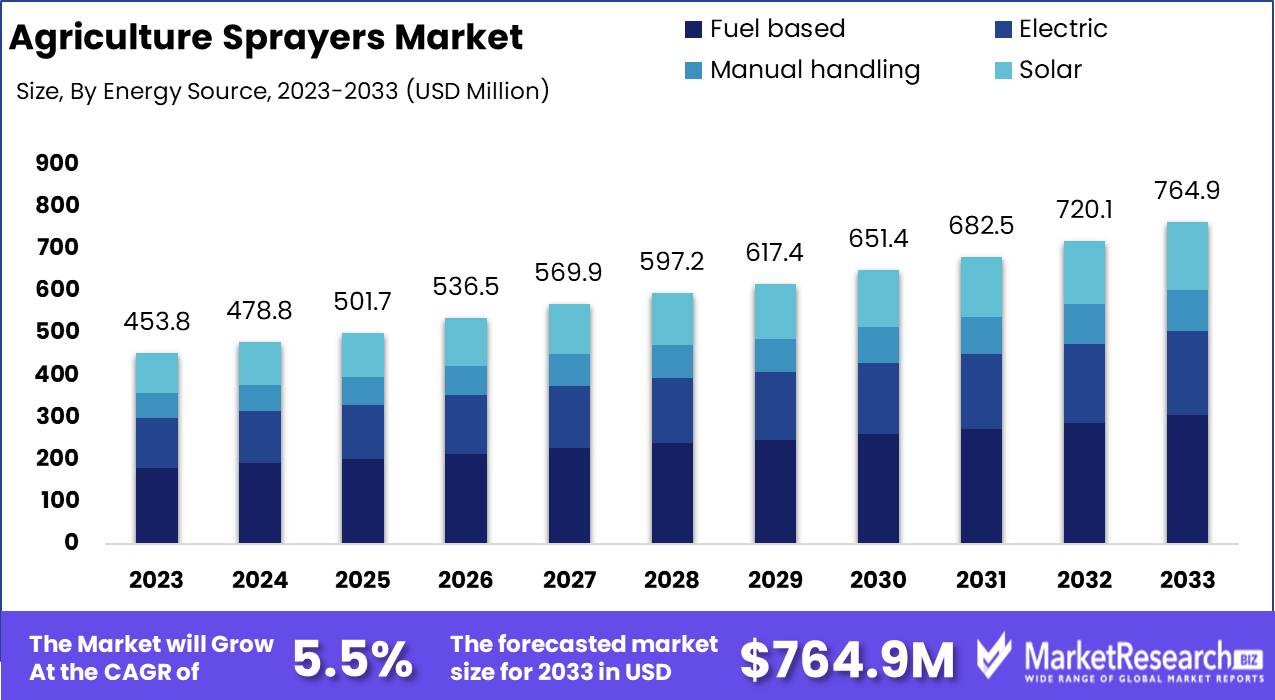

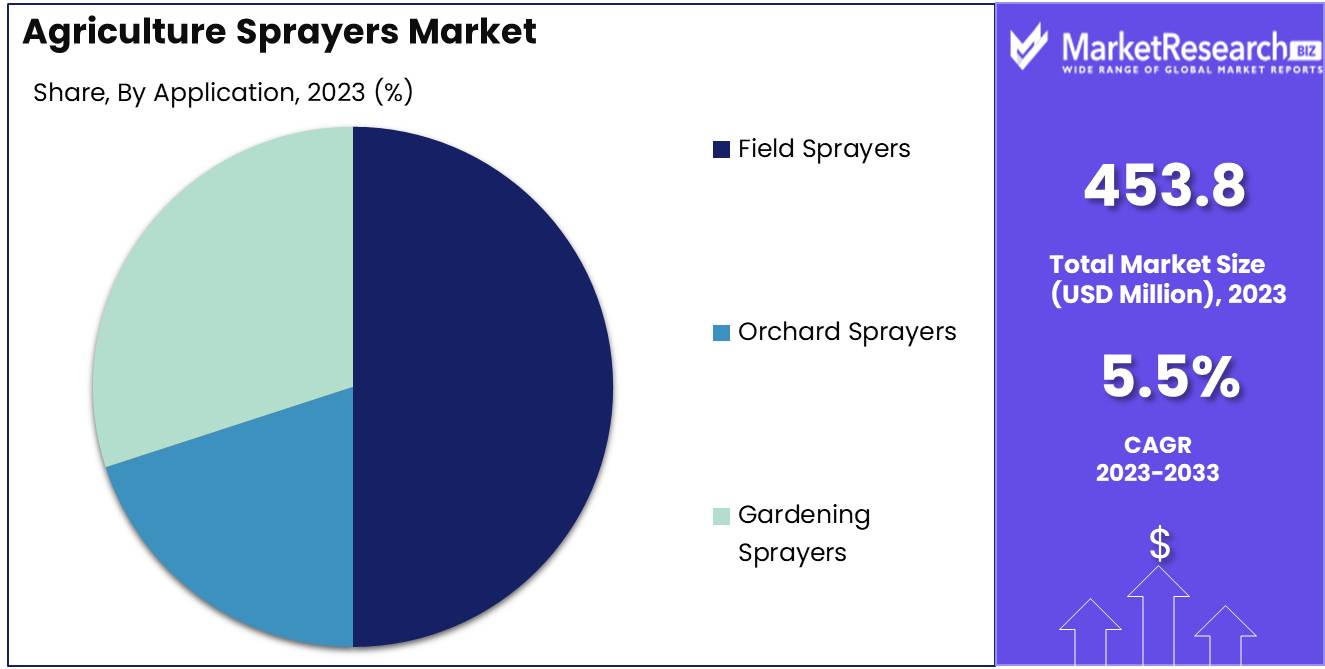

The Global Agriculture Sprayers Market was valued at USD 453.8 Mn in 2023. It is expected to reach USD 764.9 Mn by 2033, with a CAGR of 5.5% during the forecast period from 2024 to 2033.

The agriculture sprayers market encompasses the various types of equipment used for applying pesticides, herbicides, and fertilizers in agricultural settings. This market includes a wide range of products, from handheld and backpack sprayers for small-scale applications to larger, mechanized systems such as ATV, UTV, and tractor-mounted sprayers for extensive farming operations. Innovations in this sector aim to enhance efficiency, precision, and ease of use, addressing the diverse needs of horticulturists and large-scale farmers alike. The market is driven by technological advancements, increased demand for high-yield crops, and the necessity of effective pest and weed control.

The agriculture sprayers market is experiencing a significant transformation driven by technological advancements and the increasing need for efficient pest and weed management solutions. This market is pivotal for enhancing agricultural productivity and ensuring sustainable farming practices. The introduction of innovative products like the Kisan Kraft KK-PS2000, a battery-operated sprayer with a 2-liter capacity, exemplifies the shift towards more user-friendly and efficient manual operation tools tailored for horticulture and small-scale farming. These innovations not only improve application precision but also reduce labor intensity, contributing to better resource management and crop yield.

In addition, the market has seen the integration of advanced sprayer systems designed for medium to large farms, such as the WILDLIFE FARMING 25, 45 & 65 GALLON UTV SPRAYER. With tank capacities ranging from 25 to 100 gallons and boom widths up to 36 feet, these sprayers offer enhanced mobility and coverage, meeting the demands of larger agricultural operations. The capability to cover extensive areas efficiently while maintaining precise application rates is critical for modern farming enterprises aiming to maximize productivity and minimize environmental impact.

The competitive landscape of the agriculture sprayers market is increasingly dynamic, with manufacturers focusing on innovation and the development of versatile, high-performance equipment. Companies must leverage advancements in automation, IoT, and AI to create intelligent sprayer systems that can adapt to varying field conditions and optimize pesticide and fertilizer use.

Ensuring product durability, ease of maintenance, and cost-effectiveness will be crucial in capturing market share and driving growth. As the market continues to evolve, stakeholders must remain agile and responsive to emerging trends and technological innovations to maintain a competitive edge and support sustainable agricultural practices.

Key Takeaways

- Market Value: The Global Agriculture Sprayers Market was valued at USD 453.8 Mn in 2023. It is expected to reach USD 764.9 Mn by 2033, with a CAGR of 5.5% during the forecast period from 2024 to 2033.

- By Type: Tractor-Mounted sprayers constitute 30% of the market, preferred for their efficiency and range in large fields.

- By Energy Source: Fuel-based sprayers dominate with 40%, known for their power and reliability in extensive agricultural applications.

- By Application: Field Sprayers are the largest category, used in 50% of cases, essential for large-scale pesticide and nutrient application.

- Regional Dominance: Asia Pacific commands 40% of the market, supported by extensive agricultural activities and the need for increased crop yield.

- Growth Opportunity: Introducing more environmentally friendly and energy-efficient sprayer models can meet the rising demand for sustainable farming practices.

Driving factors

Increasing Demand for High-Efficiency Farming Equipment

The agriculture sprayers market is significantly driven by the rising demand for high-efficiency farming equipment. Farmers are increasingly seeking advanced machinery that enhances operational efficiency and reduces labor costs. High-efficiency sprayers enable precise application of fertilizers and pesticides, minimizing waste and ensuring uniform distribution across crops.

This precision not only improves crop yields but also optimizes resource usage, making farming more sustainable. The integration of smart technologies into sprayers further enhances their efficiency, allowing for automated adjustments based on real-time field data, which reduces human error and increases overall productivity.

Growing Adoption of Precision Agriculture

The adoption of precision agriculture practices is a pivotal factor propelling the agriculture sprayers market. Precision agriculture leverages GPS technology, IoT, and data analytics to monitor and manage crop fields with high accuracy. Sprayers equipped with precision technology can target specific areas within a field, reducing the over-application of chemicals and thereby lowering input costs.

This targeted approach not only conserves resources but also mitigates environmental impact by preventing chemical runoff into surrounding ecosystems. The demand for precision sprayers is further bolstered by the need for higher crop yields to meet global food security challenges, driving market growth as farmers invest in advanced spraying solutions.

Rising Awareness of Crop Protection Techniques

The increasing awareness of effective crop protection techniques is a crucial driver of the agriculture sprayers market. Farmers are becoming more knowledgeable about the benefits of using advanced sprayers to apply pesticides and herbicides more efficiently. Modern sprayers are designed to deliver precise doses, ensuring that crops receive the exact amount of protection needed without excess application.

This precision helps in managing pest resistance, reducing the frequency of applications, and promoting healthier crop growth. The growing emphasis on sustainable farming practices also encourages the use of advanced sprayers, which support integrated pest management strategies by enabling precise and controlled application of protective agents.

Restraining Factors

High Initial Investment Costs

The agriculture sprayers market faces significant restraint from the high initial investment costs associated with advanced spraying equipment. State-of-the-art sprayers, especially those integrated with precision agriculture technologies, often require substantial capital expenditure. This financial barrier can deter small-scale and resource-constrained farmers from adopting such technologies, limiting market penetration.

Despite the long-term benefits and potential cost savings associated with high-efficiency sprayers, the upfront costs can be prohibitive. Consequently, many farmers continue to rely on traditional, less efficient methods, slowing the overall market growth and the widespread adoption of innovative spraying solutions.

Environmental Concerns Related to Chemical Usage

Environmental concerns regarding the use of chemicals in agriculture present another significant restraint on the agriculture sprayers market. The application of pesticides and herbicides through sprayers can lead to issues such as chemical runoff, soil treatment, and harm to non-target species, including beneficial insects and aquatic life. These environmental impacts have led to stringent regulations and restrictions on chemical use in many regions, posing challenges for the sprayers market.

Farmers and manufacturers are increasingly pressured to adopt more sustainable practices and technologies. While there is a growing trend towards the development of eco-friendly and precision sprayers that minimize chemical use and environmental impact, the transition is gradual. Compliance with environmental regulations often requires additional investments in training and new equipment, further exacerbating the cost challenges for farmers.

By Type Analysis

In 2023, Tractor-Mounted held a dominant market position in the By Type segment of the Agriculture Sprayers Market, capturing more than a 30% share.

In 2023, Tractor-Mounted sprayers held a dominant market position in the By Type segment of the Agriculture Sprayers Market, capturing more than a 30% share. This significant market share is attributed to the widespread use of tractor-mounted sprayers in large-scale farming operations. These sprayers offer high efficiency, extensive coverage, and the capability to handle large volumes of pesticides, herbicides, and fertilizers. The adoption of advanced technologies and precision agriculture practices further enhances their appeal.

Handheld sprayers are essential for small-scale and precision applications, particularly in areas that are difficult to access with larger equipment. However, their market share is smaller compared to tractor-mounted sprayers due to their limited capacity and manual operation.

Self-Propelled sprayers are gaining popularity for their mobility and ease of use, especially in fields with irregular shapes or varying topography. Despite their benefits, their market share is less dominant due to higher costs and maintenance requirements.

Trailed sprayers, which are towed by tractors, offer a balance between capacity and mobility. They are preferred in medium to large farms but hold a smaller market share compared to tractor implements - mounted sprayers due to their dependency on additional equipment.

Aerial sprayers, including drones and aircraft, are emerging as effective tools for large and hard-to-reach areas. While they provide unique advantages, their market share is still developing due to regulatory challenges and high initial costs.

Backpack Sprayers are widely used for small-scale farming and precision applications, offering portability and ease of use. Their market share is modest compared to larger, more automated options due to their manual nature and limited capacity.

By Energy Source Analysis

In 2023, Fuel-based held a dominant market position in the By Energy Source segment of the Agriculture Sprayers Market, capturing more than a 40% share.

In 2023, Fuel-based sprayers held a dominant market position in the By Energy Source segment of the Agriculture Sprayers Market, capturing more than a 40% share. The prevalence of fuel-based sprayers is driven by their robust performance, high power, and suitability for large-scale agricultural operations. These sprayers are particularly favored in regions with extensive farmland, where reliable and continuous operation is critical.

Electric sprayers are gaining traction due to their environmental benefits, reduced noise, and lower operating costs. However, their market share is smaller compared to fuel-based sprayers due to limited battery life and higher initial costs.

Manual Handling sprayers remain important for small farms and specific applications where mechanized equipment is not feasible. Despite their significance, their market share is less dominant due to the labor-intensive nature and lower efficiency.

Solar sprayers are emerging as sustainable alternatives, leveraging renewable energy to reduce operational costs and environmental impact. While promising, their market share is modest due to the nascent stage of adoption and higher upfront investment.

By Application Analysis

In 2023, Field Sprayers held a dominant market position in the By Application segment of the Agriculture Sprayers Market, capturing more than a 50% share.

In 2023, Field Sprayers held a dominant market position in the By Application segment of the Agriculture Sprayers Market, capturing more than a 50% share. This dominance is driven by the extensive use of field sprayers in large-scale crop production, where efficient and uniform application of agrochemicals is crucial. Field sprayers are essential for enhancing crop yield and protecting against pests and diseases across vast agricultural lands.

Orchard Sprayers are critical for applying treatments to tree crops and vines, ensuring thorough coverage and effective pest and disease control. However, their market share is smaller compared to field sprayers due to the specialized nature of orchard farming and the limited geographical area.

Gardening Sprayers cater to small-scale applications in home gardens and horticulture, offering portability and ease of use for various gardening tasks. While important for niche markets, their market share is relatively modest compared to the extensive use of field sprayers in commercial agriculture.

Key Market Segments

By Type

- Handheld

- Self-Propelled

- Tractor-Mounted

- Trailed

- Aerial

- Backpack Sprayers

By Energy Source

- Fuel based

- Electric

- Manual handling

- Solar

By Application

- Field Sprayers

- Orchard Sprayers

- Gardening Sprayers

Growth Opportunity

Development of Advanced, Eco-Friendly Sprayers

The increasing demand for sustainable agricultural practices presents a substantial growth opportunity for the agriculture sprayers market in 2024. The development of advanced, eco-friendly sprayers that minimize chemical usage and environmental impact is gaining momentum. These innovative sprayers are designed to deliver precise doses of pesticides and herbicides, reducing the risk of chemical runoff and soil degradation.

By adopting such technologies, farmers can adhere to stringent environmental regulations while enhancing crop protection and yield. The market is likely to see accelerated growth as manufacturers invest in research and development to create sprayers that align with global sustainability goals.

Integration of IoT and GPS Technologies

The integration of Internet of Things (IoT) and Global Positioning System (GPS) technologies into agricultural sprayers represents a significant opportunity for market expansion. These technologies enable precision agriculture, allowing for real-time monitoring and control of sprayer operations. IoT-connected sprayers can collect and analyze data on crop health, soil conditions, and weather patterns, optimizing spraying schedules and reducing waste.

GPS technology ensures accurate targeting, minimizing overlap and ensuring uniform application of chemicals. This technological advancement not only improves efficiency and productivity but also enhances the sustainability of farming practices, attracting more farmers to adopt modern spraying solutions.

Latest Trends

Adoption of Drone Sprayers

The adoption of drone sprayers is a prominent trend set to reshape the agriculture sprayers market in 2024. Drones offer unparalleled efficiency and precision in spraying applications, particularly in difficult-to-reach areas or uneven terrains. Equipped with advanced sensors and GPS technology, drone sprayers can accurately map and treat specific sections of fields, reducing chemical use and environmental impact.

This trend is particularly advantageous for small to medium-sized farms, as drones require lower initial investment compared to traditional high-capacity sprayers. The increasing affordability and technological advancements in drone technology are expected to drive their widespread adoption, enhancing crop management and protection.

Use of Autonomous and Robotic Sprayers

The use of autonomous and robotic sprayers is another transformative trend in the agriculture sprayers market for 2024. These sprayers operate with minimal human intervention, leveraging artificial intelligence and machine learning to navigate fields, identify crop health issues, and apply treatments with precision. Autonomous sprayers can work continuously and efficiently, optimizing resource use and reducing labor costs.

This trend is driven by the need for increased productivity and the growing labor shortage in the agricultural sector. As these technologies become more accessible and reliable, their adoption is anticipated to rise, offering farmers a high-tech solution to enhance farming operations.

Regional Analysis

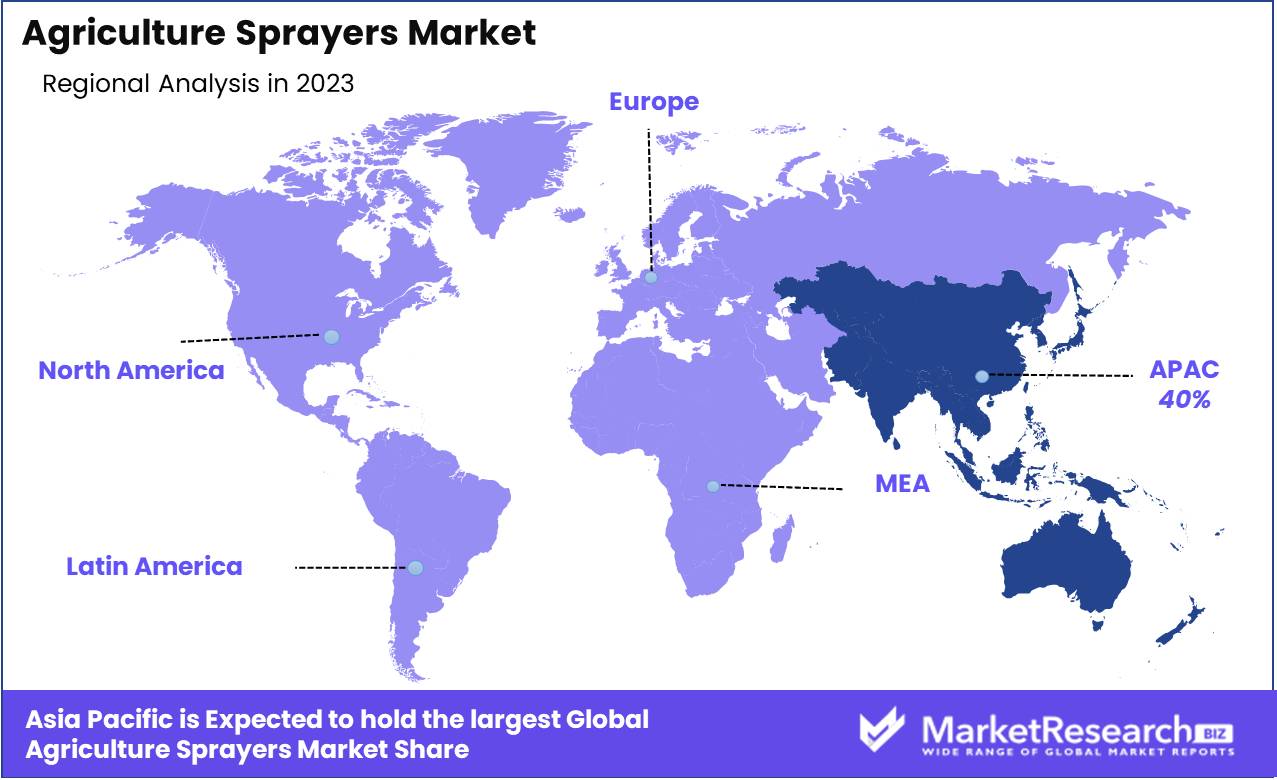

In 2023, Asia Pacific dominated the Agriculture Sprayers Market, capturing 40% of the market share.

Asia Pacific’s dominance is driven by extensive agricultural activities in countries like China, India, and Japan with 40% market share. The region benefits from a large farming population and increasing government initiatives to promote modern agricultural practices. High adoption rates of advanced spraying technologies to enhance crop yield and efficiency support the market's strong position. Rapid urbanization and rising food demand further stimulate the need for efficient agricultural sprayers in the region.

North America follows closely, driven by technological advancements in agriculture and significant investments in precision farming. The region's focus on sustainable farming practices and the presence of major market players also contribute to its substantial market share.

Europe holds a significant share, supported by stringent regulations on pesticide use and a strong emphasis on sustainable agriculture. The European Union’s policies promoting eco-friendly farming techniques further enhance market growth.

Middle East & Africa show promising potential, driven by increasing investments in agriculture and efforts to improve food security. The adoption of modern spraying technologies is gradually rising as governments and private entities focus on boosting agricultural productivity.

Latin America is emerging as a growing market for agricultural sprayers, with Brazil and Argentina leading the demand. The region benefits from extensive agricultural lands and increasing adoption of advanced farming equipment.

Key Regions and Countries

North America

- US

- Canada

- Mexico

Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

The agriculture sprayers market in 2024 is characterized by rapid technological advancements and increased demand for precision farming techniques. Leading companies such as Deere & Company, AGCO Corporation, Mahindra & Mahindra Ltd., and Kubota Corporation are driving innovation and market growth.

Deere & Company remains a market leader, leveraging its robust R&D capabilities to develop advanced sprayers with integrated precision agriculture technologies. These innovations enhance farm productivity and efficiency, catering to the growing need for sustainable farming practices. AGCO Corporation focuses on offering a diverse portfolio of sprayers, including self-propelled, trailed, and handheld models, addressing various agricultural needs across different geographies.

Mahindra & Mahindra Ltd. continues to strengthen its presence in emerging markets, providing cost-effective and durable sprayers suitable for small to mid-sized farms. Their focus on affordability and accessibility makes them a key player in regions with burgeoning agricultural activities. Kubota Corporation emphasizes innovation and reliability, with a strong presence in the Asian market. Their advanced sprayer technologies are designed to meet the specific requirements of rice and other crop farming.

H.D. Hudson Manufacturing Company and ASPEE Agro Equipment Pvt. Ltd. maintain their competitive edge by offering a range of high-quality, durable sprayers for diverse agricultural applications. Jacto Inc. leads in the Latin American market with its innovative and sustainable sprayer solutions, emphasizing environmental stewardship and farmer profitability.

GUSS Automation, LLC (GUSS AG) represents the cutting edge of automation in agriculture sprayers, offering fully autonomous sprayers that reduce labor costs and increase operational efficiency. SZ DJI Technology Co., Ltd. (DJI) leverages its expertise in drone technology to provide aerial spraying solutions, revolutionizing pest and disease management with precision and efficiency.

GVM Incorporated continues to innovate with customizable sprayer solutions, addressing specific farmer needs and optimizing crop yield. These companies collectively drive the agriculture sprayers market forward in 2024, with a strong emphasis on precision, sustainability, and technological integration.

Market Key Players

- Deere & Company

- AGCO Corporation

- Mahindra & Mahindra Ltd.

- Kubota Corporation

- H.D. Hudson Manufacturing Company

- ASPEE Agro Equipment Pvt. Ltd.

- Jacto Inc.

- GUSS Automation, LLC (GUSS AG)

- SZ DJI Technology Co., Ltd. (DJI)

- GVM Incorporated

Recent Development

- In April 2024, John Deere unveiled an advanced sprayer with precision technology, increasing application accuracy and reducing chemical use.

- In March 2024, AGCO Corporation introduced a new series of high-capacity sprayers, designed to improve efficiency and coverage for large-scale farming operations.

Report Scope

Report Features Description Market Value (2023) USD 453.8 Mn Forecast Revenue (2033) USD 764.9 Mn CAGR (2024-2033) 5.5% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Handheld, Self-Propelled, Tractor-Mounted, Trailed, Aerial, Backpack Sprayers), By Energy Source (Fuel based, Electric, Manual handling, Solar), By Application (Field Sprayers, Orchard Sprayers, Gardening Sprayers) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Deere & Company, AGCO Corporation, Mahindra & Mahindra Ltd., Kubota Corporation, H.D. Hudson Manufacturing Company, ASPEE Agro Equipment Pvt. Ltd., Jacto Inc., GUSS Automation, LLC (GUSS AG), SZ DJI Technology Co., Ltd. (DJI), GVM Incorporated Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Deere & Company

- AGCO Corporation

- Mahindra & Mahindra Ltd.

- Kubota Corporation

- H.D. Hudson Manufacturing Company

- ASPEE Agro Equipment Pvt. Ltd.

- Jacto Inc.

- GUSS Automation, LLC (GUSS AG)

- SZ DJI Technology Co., Ltd. (DJI)

- GVM Incorporated

Our Clients

View Our Licence Options