Global Aerospace Raw Materials Market By Platform Type(Commercial Aircraft, Regional Aircraft, General Aviation, Military Aircraft, Helicopter, Spacecraft), By Material Type(Titanium & Alloys, Aluminum & Alloys, Steel & Alloys, Composites, Others), By Sales Channel Type(Direct Sales, Distributor Sales), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

46235

-

May 2024

-

300

-

-

This report was compiled by Research Team Research team of over 50 passionate professionals leverages advanced research methodologies and analytical expertise to deliver insightful, data-driven market intelligence that empowers businesses across diverse industries to make strategic, well-informed Correspondence Research Team Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

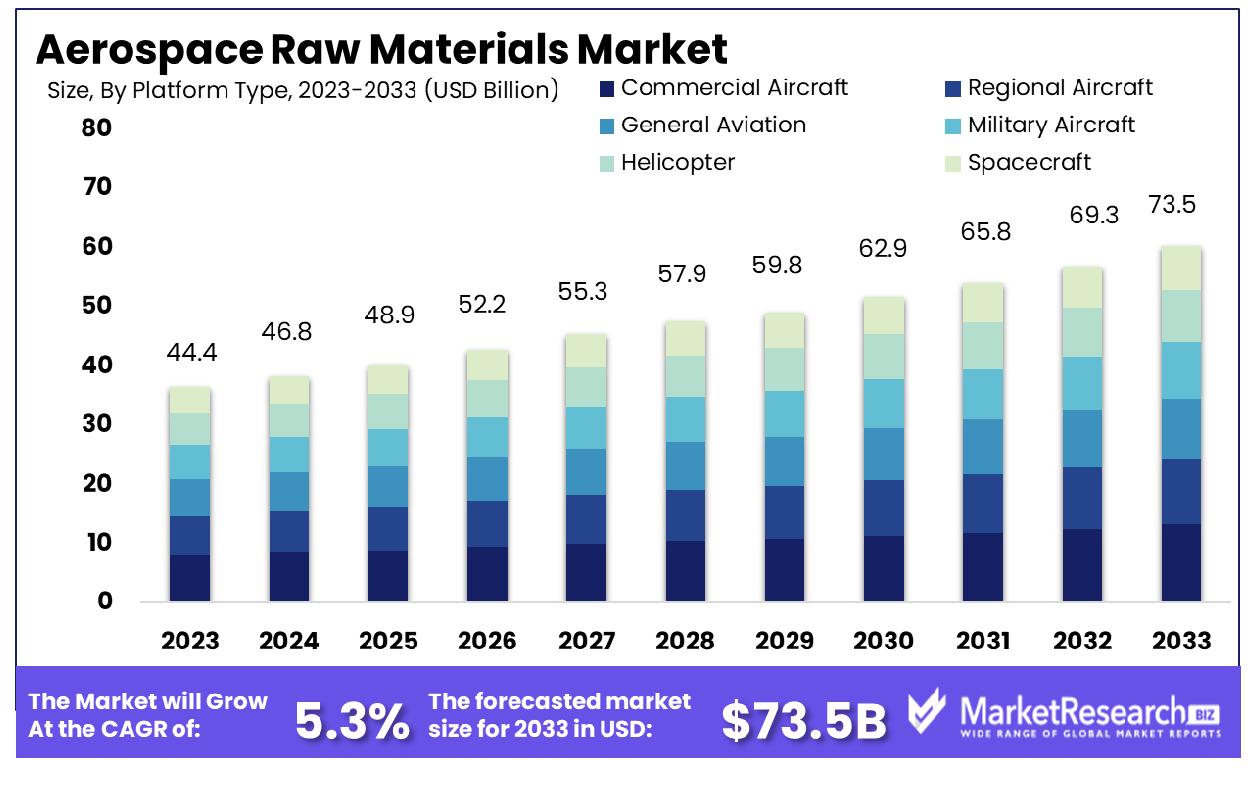

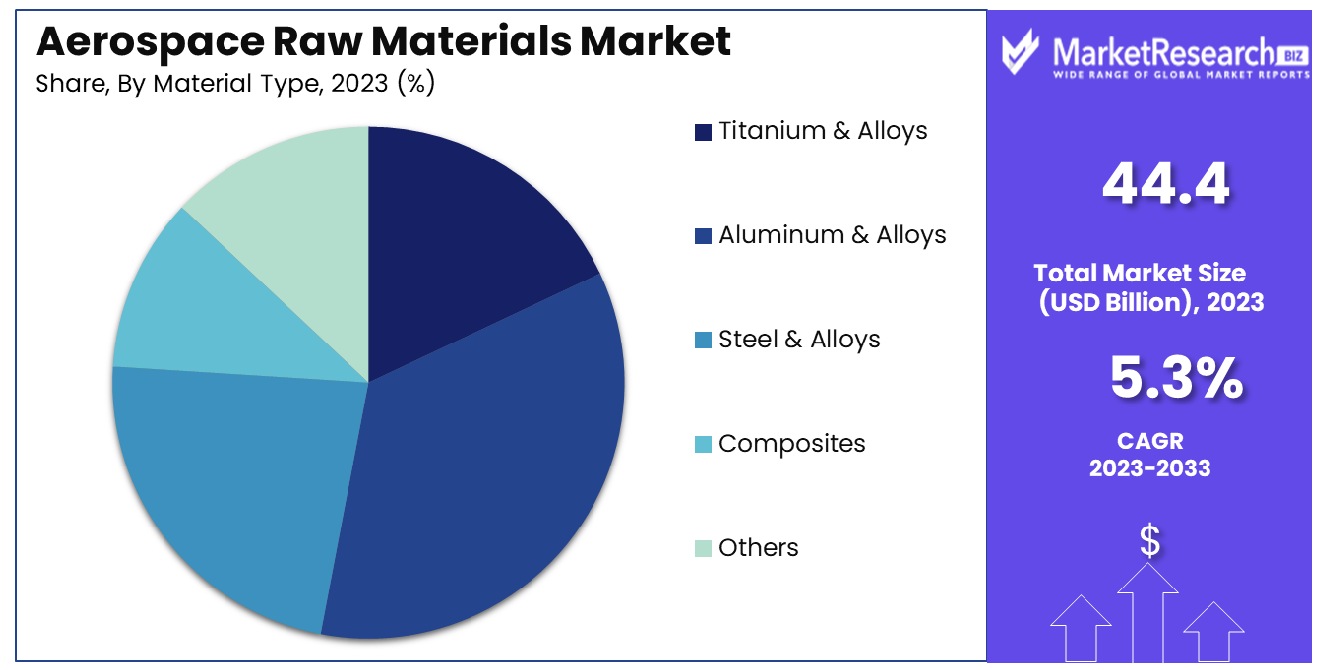

The Global Aerospace Raw Materials Market was valued at USD 44.4 billion in 2023. It is expected to reach USD 73.5 billion by 2033, with a CAGR of 5.3% during the forecast period from 2024 to 2033.

The Aerospace Raw Materials Market encompasses the procurement and utilization of essential materials required for manufacturing aerospace components and structures. This market is pivotal in sourcing metals like aluminum and titanium, advanced composites, alloys, and thermoplastics, which are integral for crafting airframes, engines, and interior fittings.

The strategic selection of these materials directly influences the performance, weight, and durability of aerospace products, thereby impacting overall industry competitiveness and innovation. Vice Presidents, CEOs, Chief Marketing Officers, and Product Managers within the aerospace sector must prioritize advancements and sustainability in this market to enhance product efficiency and meet stringent regulatory standards.

The Aerospace Raw Materials Market is currently undergoing significant transformations driven by fluctuations in material costs and demands for advanced, lightweight materials. Notably, the price of stainless steel, a critical component in aerospace manufacturing, has doubled since September 2022. This surge has elevated overall raw material costs by 69% over the past year, posing financial challenges for manufacturers and impacting production costs across the industry. Despite these hurdles, the market exhibits robust growth potential, projected to expand at a compound annual growth rate (CAGR) of 6.46% and reach USD 11.39 billion by 2030.

This growth trajectory is supported by the increasing demand for more fuel-efficient and environmentally friendly aircraft, which necessitates continuous innovation in materials technology. Manufacturers are compelled to explore alternative materials and composites that can reduce aircraft weight without compromising structural integrity. Moreover, the adoption of these advanced materials aligns with the industry's shift towards sustainability, aiming to reduce the environmental impact of aviation.

For industry leaders, navigating these cost dynamics while investing in research and development for sustainable materials is crucial. They must strategically manage their supply chains to mitigate the risks associated with price volatility and ensure steady material availability. This approach will not only address immediate cost concerns but also position companies competitively in a market that values technological advancement and environmental responsibility.

Key Takeaways

- Market Growth: The Global Aerospace Raw Materials Market was valued at USD 44.4 billion in 2023. It is expected to reach USD 73.5 billion by 2033, with a CAGR of 5.3% during the forecast period from 2024 to 2033.

- By Platform Type: Commercial aircraft led with a 45% share.

- By Material Type: Aluminum and alloys held a 40% dominance.

- By Sales Channel Type: Distributor sales commanded a 65% majority.

- Regional Dominance: Europe holds 36.4% of the aerospace raw materials market.

- Growth Opportunity: In 2023, the aerospace raw materials market is thriving due to a focus on sustainability and enhanced R&D for innovative, environmentally friendly, and efficient materials.

Driving factors

Global Aerospace Industry Expansion and Rising Air Travel Demand

The global aerospace industry is undergoing rapid expansion, driven primarily by increasing demand for air travel, particularly in emerging markets. This surge in air traffic is compelling aerospace companies to expand their fleets, directly influencing the demand for aerospace raw materials. The growing number of aircraft orders is reflected in production forecasts, with Boeing projecting a need for 43,610 new aircraft over the next 20 years, a testament to the ongoing growth trajectory of the aerospace sector.

This escalation is not only boosting the volume demand for raw materials such as aluminum, titanium, and composites but is also pushing the market towards more innovative, lightweight materials that contribute to fuel efficiency and emissions reductions.

Technological Advancements and R&D in Aerospace

Technological advancements and robust research and development (R&D) initiatives are pivotal in shaping the aerospace raw materials market. The shift towards next-generation aircraft that are lighter, more fuel-efficient, and capable of reducing carbon footprints drives the need for advanced materials.

For instance, the integration of carbon fiber reinforced polymers (CFRP) and other composite materials enhances aircraft performance by reducing weight and increasing durability and resistance to environmental factors. The continuous innovation in material science, supported by substantial R&D investments by key aerospace players, is essential for developing materials that meet the evolving standards of the aerospace industry.

Global Demand for New and Efficient Aerospace Materials

The global push for new and efficient aerospace materials is closely linked to environmental sustainability goals and the need for operational efficiency in the aerospace sector. With stringent environmental regulations and rising fuel prices, the industry is compelled to adopt materials that contribute to the overall efficiency of aircraft.

Materials such as advanced alloys and composites are being increasingly preferred for their benefits in weight reduction and maintenance costs, leading to their expanded use in both military and commercial aircraft. The demand for these innovative materials is expected to grow, as they are critical to achieving the industry's goals of sustainability and cost-effectiveness in operations.

Restraining Factors

Industry Shifts Impacting Metal Utilization

Changes within the aerospace industry, particularly the shift towards composite materials and away from traditional metals like aluminum and titanium, significantly impact the dynamics of the aerospace raw materials market. This transition is driven by the demand for more fuel-efficient and lighter aircraft. As a result, the usage of metals is evolving, with a notable reduction in the preference for heavy metals and an increased incorporation of lighter alloys and composites.

For instance, the Boeing 787 and Airbus A350 series have set trends by incorporating approximately 50% composite materials in their structures, directly influencing the demand and market dynamics for traditional aerospace metals. This shift poses challenges for suppliers and manufacturers of these metals, compelling them to innovate and diversify their offerings to include advanced materials that align with current industry preferences.

Stringent Security and Regulatory Challenges

The aerospace raw materials market is further constrained by stringent security and regulatory policies, especially within the defense sector. These regulations dictate the standards for material composition, quality, and sourcing, which can significantly slow down production processes and increase costs. For example, materials used in military aircraft must comply with rigorous safety and performance standards, often requiring extensive testing and certification.

This regulatory environment, while crucial for safety and reliability, often acts as a barrier to the rapid adoption of new materials and technologies, thereby restraining market growth. The defense sector's need for materials that meet high security and performance specifications can limit the market's ability to quickly adapt to new technologies and material innovations.

By Platform Type Analysis

Commercial aircraft held a dominant 45% market share by platform type.

In 2023, Commercial Aircraft held a dominant market position in the By Platform Type segment of the Aerospace Raw Materials Market, capturing more than 45% of the market share. This segment's strong performance is primarily attributed to the increasing demand for new aircraft to accommodate the global surge in air travel and the replacement of older aircraft with more fuel-efficient models. The aerospace industry's focus on sustainability has also driven the demand for advanced lightweight materials, contributing to the growth of this segment.

Following Commercial Aircraft, the segments of Regional Aircraft and General Aviation also showed significant market activity. Regional Aircraft accounted for approximately 20% of the market, supported by the rising demand for short-haul flights and the expansion of regional air services. General Aviation, which includes private and business aircraft, held about 15% of the market, benefitting from the increasing number of high-net-worth individuals and the demand for personalized travel.

Military Aircraft and Helicopters represented smaller yet vital segments of the aerospace raw materials market. Military Aircraft accounted for around 10% of the market, driven by global increases in defense budgets and ongoing technological upgrades. The Helicopter segment, holding a 5% market share, saw growth due to its versatile applications in disaster relief, medical evacuation, and transportation in remote areas.

The Spacecraft segment, though the smallest, captured about 5% of the market. This segment is poised for growth with rising investments in space exploration and satellite deployment by both governmental and private entities. The demand for materials capable of withstanding extreme space conditions supports this segment's expansion.

Collectively, these segments underscore the diverse applications and dynamic nature of the Aerospace Raw Materials Market, reflecting different growth drivers and technological advancements across platforms.

By Material Type Analysis

Aluminum and alloys led the materials segment, capturing 40% of the market.

In 2023, Aluminum & Alloys held a dominant market position in the By Material Type segment of the Aerospace Raw Materials Market, capturing more than 40% of the market share. Aluminum & Alloys are favored in the aerospace industry due to their strength-to-weight ratio, corrosion resistance, and cost-effectiveness, which are crucial for aircraft performance and fuel efficiency.

Following closely, Composites accounted for approximately 25% of the market. The rising adoption of composites is driven by their advantages in reducing aircraft weight and enhancing durability, which significantly improve fuel efficiency and operational capabilities. Composites are increasingly used in both structural applications and critical components of aircraft.

Titanium & Alloys, known for their high strength, lightweight, and resistance to high temperatures, held around 20% of the market. These materials are predominantly used in engine components and critical aerospace structures, where their properties can be fully utilized to enhance performance and longevity.

Steel & Alloys, which accounted for 10% of the market share, are utilized for their durability and cost-effectiveness. They are primarily used in landing gear and other applications where high strength and resistance to wear and tear are essential.

The Others category, comprising various specialty materials, made up about 5% of the market. This segment includes materials such as ceramics and thermoplastics, which are used in specific applications that require unique properties such as high heat resistance or electrical insulation.

Overall, the Aerospace Raw Materials Market is characterized by a diverse range of materials, each serving specific purposes that contribute to advancements in aerospace technology and efficiency.

By Sales Channel Type Analysis

Distributor sales are significantly led by channel type, comprising 65% of the market.

In 2023, Distributor Sales held a dominant market position in the By Sales Channel Type segment of the Aerospace Raw Materials Market, capturing more than 65% of the market share. This significant portion of the market underscores the critical role distributors play in the aerospace supply chain, offering extensive networks and streamlined logistics that facilitate the efficient distribution of raw materials globally.

Distributors provide value-added services such as inventory management, just-in-time delivery, and supply chain optimization, which are crucial for manufacturers facing tight production schedules and cost constraints.

Direct Sales accounted for the remaining 35% of the market. This channel is typically favored by manufacturers seeking to establish close relationships with raw material suppliers to ensure the reliability and quality of supply. Direct sales are often preferred for transactions involving highly specialized materials or when significant customization is required. This approach allows aerospace manufacturers to exert greater control over their supply chains, enhancing transparency and reducing potential risks associated with third-party handling.

The distinct advantages of each sales channel cater to different strategic needs within the aerospace industry. While distributor sales offer broad access and logistical advantages, direct sales provide precision and customization. As the aerospace sector continues to evolve with technological advancements and shifting market dynamics, the balance between these sales channels may shift, reflecting changes in manufacturing strategies and supply chain configurations.

Key Market Segments

By Platform Type

- Commercial Aircraft

- Regional Aircraft

- General Aviation

- Military Aircraft

- Helicopter

- Spacecraft

By Material Type

- Titanium & Alloys

- Aluminum & Alloys

- Steel & Alloys

- Composites

- Others

By Sales Channel Type

- Direct Sales

- Distributor Sales

Growth Opportunity

Rising Focus on Environmental Sustainability

In 2023, the global aerospace raw materials market is witnessing significant growth opportunities driven by an intensifying focus on environmental sustainability. As the aerospace industry faces mounting pressures to reduce its environmental footprint, there is an escalating demand for advanced materials that not only meet stringent safety and performance standards but also comply with rigorous environmental regulations.

This shift is catalyzed by global policy changes and an increased awareness among stakeholders about the importance of sustainable practices. Consequently, materials that offer enhanced efficiency and lower emissions are becoming critical in the design and manufacture of aerospace components. This trend is likely to influence market dynamics substantially, fostering innovation and potentially leading to the development of new, eco-friendly materials.

Increasing Research and Development Activities

Concurrently, the aerospace raw materials market is experiencing a surge in research and development (R&D) activities aimed at material innovation and technology enhancement. The drive to develop materials that can withstand extreme conditions while providing weight reductions and cost savings is fueling investments in R&D.

These activities are not only focused on creating new materials but also on improving the processing and recyclability of existing materials, thus extending their lifecycle and reducing waste. As aerospace companies continue to seek competitive advantages through material technology, the R&D landscape in this market is expanding, leading to more sophisticated and application-specific materials that could revolutionize aerospace manufacturing processes.

Latest Trends

Increased Production Rates by Airbus and Boeing

In 2023, a notable trend within the global aerospace raw materials market is the strategic decision by industry giants, Airbus and Boeing, to increase their production rates for key aircraft programs. This upsurge in production is in response to recovering demand in the aviation sector, particularly for commercial airliners, as global travel restrictions ease. The planned increase in production rates is expected to drive substantial demand for aerospace raw materials.

Suppliers and manufacturers in the aerospace supply chain are likely to experience heightened activity, necessitating robust logistical and operational capabilities to meet the increased production demands. This trend underscores a bullish outlook for the aerospace materials market, reflecting a resurgence in the aviation industry's growth trajectory post-pandemic.

Continued High Demand for Titanium and Composites

Furthermore, 2023 continues to see strong demand for specific aerospace materials, notably titanium and composites. These materials are prized for their strength-to-weight ratios and corrosion resistance, qualities essential for modern aerospace applications. Titanium and composites are integral to manufacturing processes that aim to enhance aircraft performance while minimizing environmental impact.

Their continued high demand is driven by ongoing efforts to improve fuel efficiency and reduce emissions in line with global sustainability goals. As aerospace manufacturers and suppliers focus on these advanced materials, the market for titanium and composites is expected to remain robust, supported by technological advancements and increased adoption in both commercial and military aerospace valves sectors.

Regional Analysis

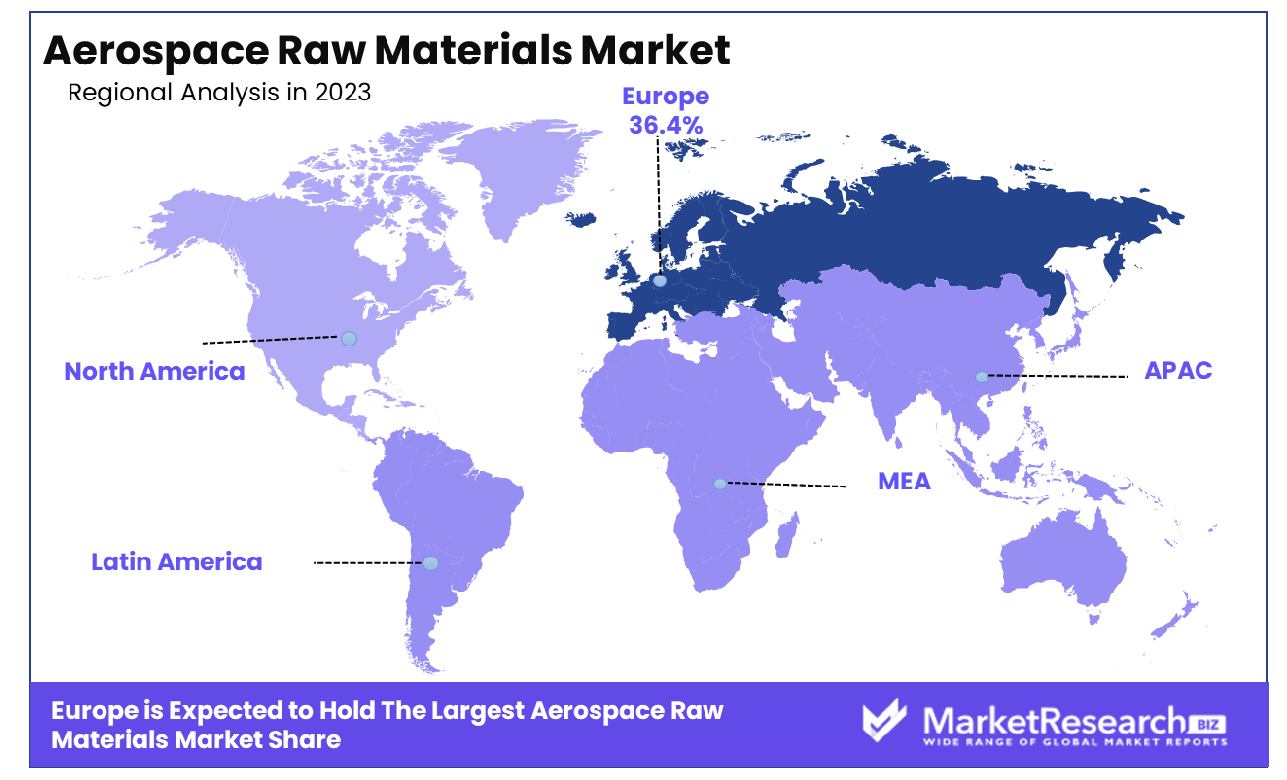

The aerospace raw materials market in Europe holds a significant 36.4% share globally.

The aerospace raw materials market is segmented into five key regions: North America, Europe, Asia Pacific, Middle East & Africa, and Latin America, each demonstrating unique growth dynamics and market potentials.

North America, a prominent player in the aerospace sector, leverages its advanced manufacturing capabilities and substantial investments in aerospace R&D. The region's market is bolstered by the presence of major aerospace corporations and extensive supply chain infrastructure, supporting a robust demand for high-performance materials.

Europe holds a dominant position, accounting for 36.4% of the global market. This is attributed to its strong aerospace industry, led by major manufacturers and suppliers who are pushing for innovation in lightweight and durable aerospace materials. The focus on reducing environmental impact and enhancing fuel efficiency continues to drive the European market forward.

The Asia Pacific region is witnessing rapid growth, driven by the expanding aviation sectors in countries like China and India. Increasing air traffic, coupled with rising military expenditures in the region, fuels the demand for aerospace raw materials. The region is expected to exhibit significant growth rates over the forecast period, supported by ongoing industrial expansions and technological advancements.

The Middle East & Africa region, though smaller in comparison, shows potential due to increasing investments in airport infrastructure developments and the growing focus on diversifying economies away from oil dependency. This shift is likely to increase the demand for aircraft, subsequently boosting the market for aerospace raw materials.

Latin America, while currently the smallest segment, is poised for growth. Factors such as the gradual recovery of Brazil’s economy and increasing air travel in South America contribute to the region's market expansion prospects.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of Middle East & Africa

Key Players Analysis

In the dynamic landscape of the global Aerospace Raw Materials Market in 2023, several key players are pivotal in driving industry standards and innovation. Global Titanium Inc., renowned for its specialized production capabilities, continues to lead in the supply of titanium, essential for lightweight and high-strength aerospace components. AMETEK Inc., with its diversified portfolio, strengthens its position through advanced materials technologies that enhance product reliability and performance in aerospace applications.

ArcelorMittal stands out for its vast array of steel and alloy products, catering to the rigorous demands of aerospace manufacturing. Its commitment to sustainable practices aligns with the industry's shift towards environmentally friendly materials. Similarly, NSSMC Group leverages its expertise in steel products, focusing on innovation to meet the stringent quality standards required in aerospace.

Supreme Engineering Ltd and AMG Advanced Metallurgical Group play crucial roles in supplying specialized alloys that are fundamental to aerospace engineering. Their focus on R&D helps in developing materials that resist extreme conditions encountered in aviation environments.

Allegheny Technologies Incorporated (ATI) and Precision Castparts Corp are notable for their precision in producing critical aerospace components. Their advanced manufacturing processes ensure high performance and durability, which are paramount in the aerospace sector.

Special Metals and Doncasters Group Ltd further enrich the market with their niche offerings in superalloys and precision-engineered components, respectively. These companies are integral to the supply chain, providing materials that uphold safety and efficiency in aerospace operations.

Market Key Players

- Global Titanium Inc

- AMETEK Inc

- ArcelorMittal

- NSSMC Group

- Supreme Engineering Ltd

- Technologies

- AMG Advanced Metallurgical Group

- Allegheny

- Incorporated (ATI)

- Precision Castparts Corp

- Special Metals

- Doncasters Group Ltd

Recent Development

- In April 2024, PaperShell, aided by RISE, developed bio-based materials from agricultural and forestry waste. Secured SEK 114 million in funding, advancing pilot production for customizable fiber composites and weather-resistant plastics.

- In March 2024, Open Trellis CEO Dale Fickett discusses U.S. manufacturing opportunities amid mixed economic signals. Emphasizes leveraging tech combinations, understanding cost implications, and aligning with innovation-led industrial policy.

Report Scope

Report Features Description Market Value (2023) USD 44.4 Billion Forecast Revenue (2033) USD 73.5 Billion CAGR (2024-2032) 5.3% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Platform Type(Commercial Aircraft, Regional Aircraft, General Aviation, Military Aircraft, Helicopter, Spacecraft), By Material Type(Titanium & Alloys, Aluminum & Alloys, Steel & Alloys, Composites, Others), By Sales Channel Type(Direct Sales, Distributor Sales) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Global Titanium Inc, AMETEK Inc, ArcelorMittal, NSSMC Group, Supreme Engineering Ltd, Technologies, AMG Advanced Metallurgical Group, Allegheny, Incorporated (ATI), Precision Castparts Corp, Special Metals, Doncasters Group Ltd Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Global Titanium Inc

- AMETEK Inc

- ArcelorMittal

- NSSMC Group

- Supreme Engineering Ltd

- Technologies

- AMG Advanced Metallurgical Group

- Allegheny

- Incorporated (ATI)

- Precision Castparts Corp

- Special Metals

- Doncasters Group Ltd

Our Clients

View Our Licence Options