Aerospace Cold Forgings Market By Platform (Fixed Wing (Narrow-body, Regional Jets, Wide Body, Fighter Jets), Rotary Wing (Helicopters)), By Application (Airframe, Landing Gear, Nacelle Component), By Technology, By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2024-2033

-

45426

-

May 2024

-

300

-

-

This report was compiled by Research Team Research team of over 50 passionate professionals leverages advanced research methodologies and analytical expertise to deliver insightful, data-driven market intelligence that empowers businesses across diverse industries to make strategic, well-informed Correspondence Research Team Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

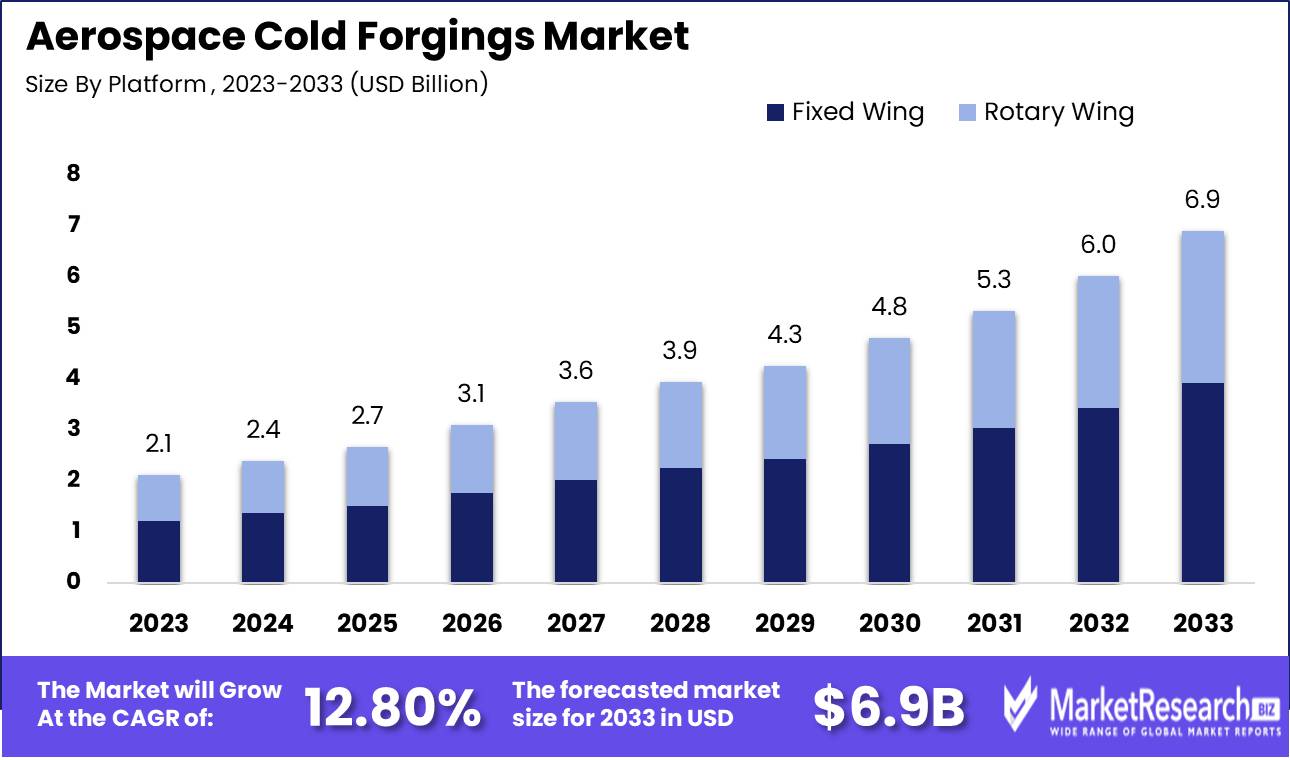

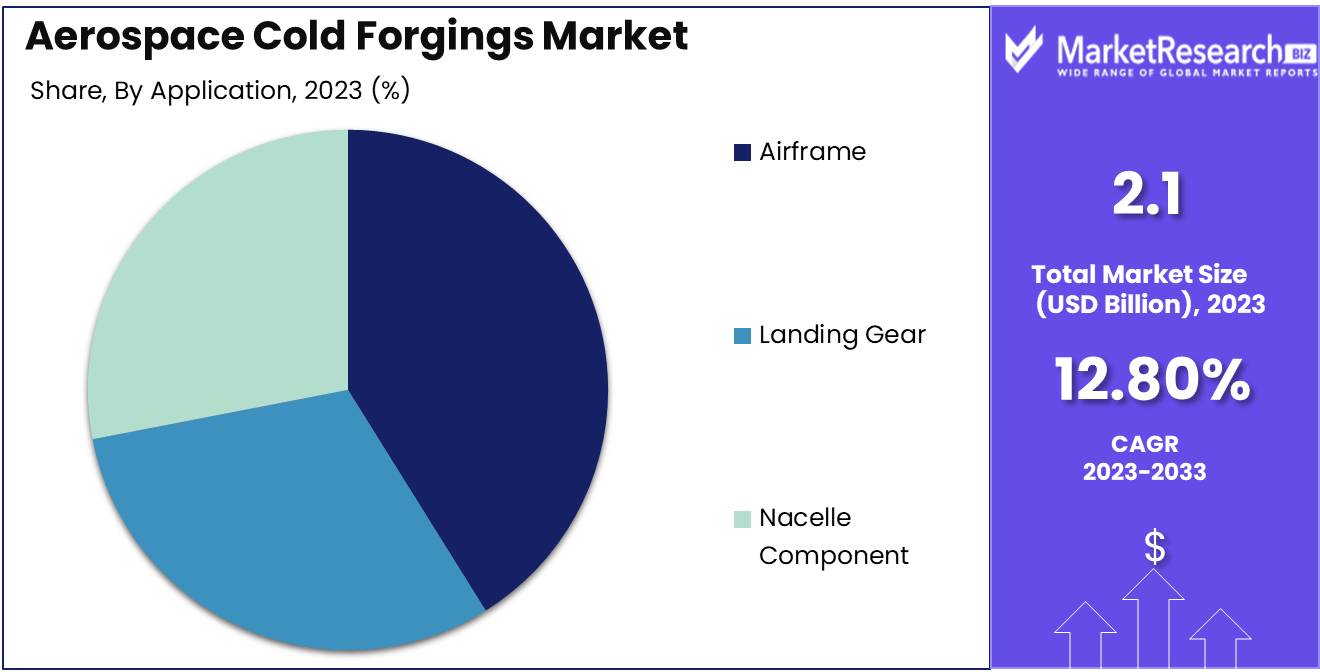

The Aerospace Cold Forging Market was valued at USD 2.13 billion in 2023. It is expected to reach USD 6.82 billion by 2033, with a CAGR of 12.80% during the forecast period from 2024 to 2033.

The surge in demand for military and commercial aircraft is one of the key driving factors for the aerospace cold forging market. The aerospace cold forging aims at the manufacturing and production of cold-forged elements and parts in the aerospace industry. Cold forging is a technique that shapes metal by applying pressure without any heat interference and storing it at room temperature. It uses the plasticity of metals which is also known as plastic forming. It provides proper structure to the materials by distorting and twisting them, so almost no metal waste is produced during this production. Likewise, materials are manufactured at room temperature without any thermal pressure, dimensional precision is fine and even the difficult structures can be manufactured at high speed. The cold forging technology has high material appliance efficacy and makes sure that the accuracy and fast processing can make environmentally friendly and rationalized manufacturing technology.

The aerospace industry requires less weight and lasting elements to improve aircraft performance and fuel efficacy while upholding strict safety measures. These are low-cost and have effective techniques for manufacturing high-strength aerospace elements with complicated geometries. Cold forging plays an important role in meeting these demands by offering components with better mechanical elements like high strength, enhanced exhaustion resistance, and dimensional precision. The latest progression in cold forging technologies has substantially improved the competences and efficacy of the techniques. New methods like accuracy forging and near net shape structure permit the manufacturing of difficult geometries with high precision and enhanced material usage. Such type of advancements have increased the application areas of cold forging in the aerospace industry.

As the aerospace industry is aiming for sustainability, it has witnessed a significant emphasis on decreasing the environmental impact of aircraft production processes. Cold forging supports such sustainability goals as they basically demand minimal energy as compared to other production techniques. The utilization of cold forging can contribute to decreasing carbon emissions and improving the overall environmental sustainability of the aerospace industry. This industry is also witnessing a rise in aircraft manufacturing, driven by an upsurge in air travel requirements and the demand to replace aging fleets. It has led to a higher demand for aerospace elements that comprise cold-forged equipment. the demand for aerospace cold forging will increase due to its high-end requirement in the aerospace industry which will help in market expansion during the forecasted period.

Key Takeaways

- Market Growth: The aerospace cold forging market was valued at USD 2.13 billion in 2023. It is expected to reach USD 6.82 billion by 2033, with a CAGR of 12.80% during the forecast period from 2024 to 2033.

- By Platform : Fixed Wing segment held a dominant position in the Aerospace Cold Forgings Market.

- By Application: Airframe segment held a dominant position in the Aerospace Cold Forgings Market.

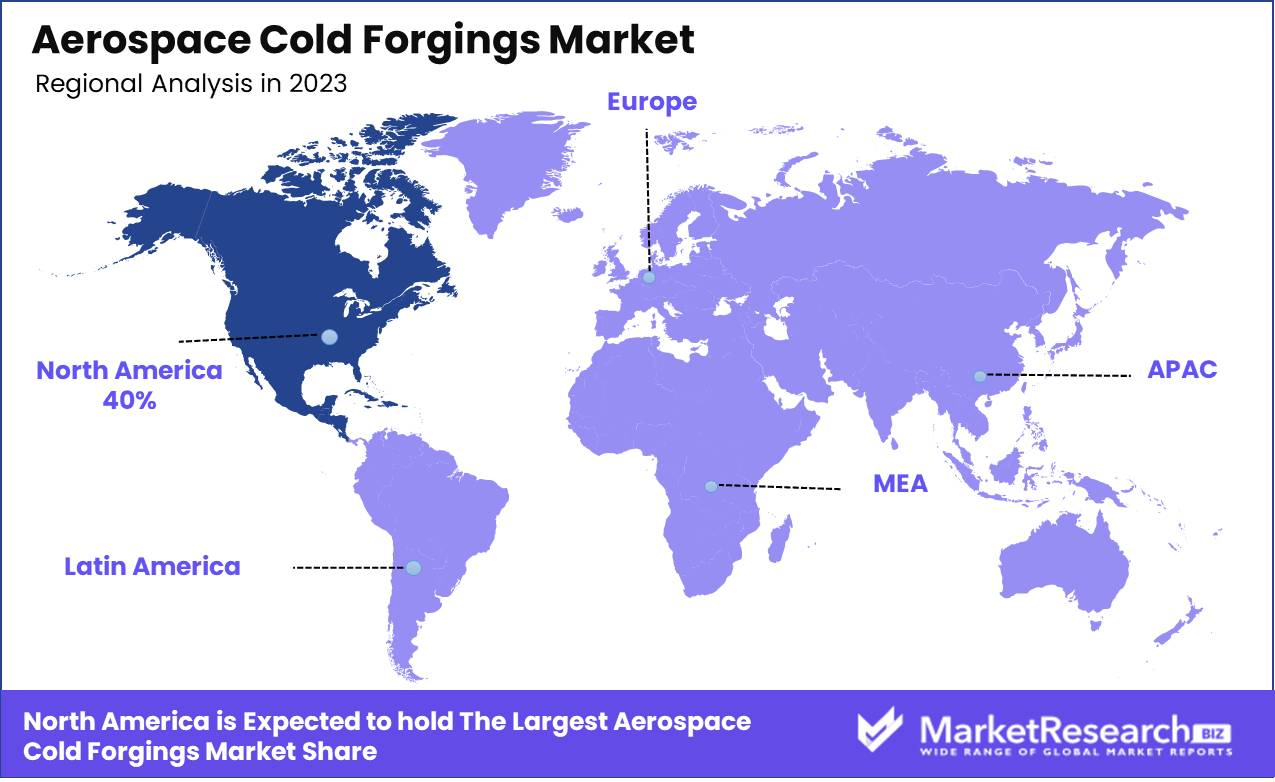

- Regional Dominance: North America leads the global aerospace cold forgings market with a 40% share.

- Growth Opportunity: The aerospace cold forgings market is set to thrive on titanium alloys and precision forging innovations.

Driving factors

Material Selection: Enhancing Performance and Efficiency in Aerospace Applications

The choice of materials in the aerospace cold forgings market is pivotal, influencing not only the performance and durability of aerospace components but also the efficiency of manufacturing processes and the overall cost-effectiveness of production. In aerospace applications, materials such as titanium, aluminum, and high-strength steel are predominantly used due to their lightweight, high strength-to-weight ratio, and resistance to environmental stress and corrosion.

For instance, titanium is highly valued in the aerospace industry for its exceptional strength and corrosion resistance, making it ideal for critical aircraft structures where reliability and longevity are paramount. The increased adoption of titanium in aerospace cold forgings helps in reducing the overall weight of the aircraft, thereby enhancing fuel efficiency and performance. Statistics indicate that the use of advanced materials like titanium in aerospace applications can lead to a weight reduction of up to 30%, which directly contributes to more efficient aircraft performance and reduced environmental impact.

Cold Working Techniques: Refining Manufacturing Precision and Product Integrity

Cold working techniques, which involve the deformation of metal at room temperature to enhance its yield strength and hardness, play a critical role in the aerospace cold forgings market. These methods improve the mechanical properties of metals without altering their inherent characteristics, which is crucial for aerospace components that must withstand extreme conditions.

The primary advantage of cold working includes the elimination of shrinkage and porosity, which are common in hot forging. This results in a denser, more precise, and higher quality product. The refined grain structure achieved through cold working enhances the fatigue resistance of the components, an essential requirement for aerospace parts subjected to cyclic stress.

Heat Treatment: Optimizing Material Properties for Advanced Aerospace Applications

Heat treatment processes are integral to the aerospace cold forgings market, as they significantly enhance the material properties of forged parts, such as their strength, hardness, and resistance to wear and fatigue. These processes involve controlled heating and cooling operations, tailored to the specific requirements of each material and component design, thus optimizing their performance in aerospace applications.

Heat treatment can alter the microstructure of metals, enhancing their mechanical properties to meet the stringent standards required for aerospace components. For example, the process of annealing can relieve internal stresses in the metal caused by prior cold working, thereby improving ductility and reducing brittleness. This is particularly important in aerospace, where the reliability and safety of components cannot be compromised.

Restraining Factors

Impact of Raw Material Price Volatility on Market Growth

The price volatility of raw materials, such as aluminum, titanium, and high-grade steel, which are predominantly used in aerospace forgings, significantly impacts the aerospace cold forgings market. This volatility can be attributed to several factors including fluctuating geopolitical scenarios, changes in supply chain dynamics, and shifts in global demand. For aerospace manufacturers, raw material costs constitute a substantial portion of production expenses. When prices of these materials spike, it compresses profit margins and compels manufacturers to reconsider pricing strategies for their end products.

From a strategic perspective, companies often hedge against this volatility by entering into long-term contracts with suppliers to lock in prices. However, this strategy is not foolproof; sudden and severe fluctuations can still affect contractual terms or lead to renegotiations, which might not always be favorable. Additionally, companies invest in supply chain diversification, sourcing materials from different geographical regions to mitigate the risk associated with any single source.

Influence of Stringent Regulatory Standards on Market Growth

The aerospace industry is one of the most heavily regulated industries globally. Stringent standards, covering everything from material specifications and production processes to part performance and safety, pose significant challenges to forging manufacturers. These regulations ensure that every component used in aerospace meets the highest safety and performance standards due to the critical nature of their applications.

Compliance with such stringent regulations incurs substantial costs in terms of both time and resources. Each new product or innovation must undergo rigorous testing and approval processes before it can be brought to market, which can significantly lengthen product development cycles and increase costs. This not only impacts the speed at which new products can be introduced but also affects the overall agility of companies operating within this market space.

By Platform Analysis

Fixed Wing segment held a dominant position in the By Platform category of the Aerospace Cold Forgings Market.

In 2023, the Fixed Wing segment held a dominant position in the By Platform category of the Aerospace Cold Forgings Market. This segment's prominence is primarily attributed to the extensive use of cold forged parts in the construction and maintenance of fixed-wing aircraft, which include commercial airliners, private jets, and military fighters. Cold forging enhances the strength and reliability of critical components such as fuselage structures, engine mounts, and landing gear. The demand for fixed-wing aircraft has been sustained by the growing global air travel and the increasing military expenditures by countries aiming to modernize their air fleets.

Conversely, the Rotary Wing segment, which encompasses helicopters and other aircraft with rotary wings, also significantly utilizes cold forgings for its critical components, though it occupies a smaller share of the market compared to fixed-wing. The specific requirements for durability and precision in rotary-wing aircraft drive the need for specialized forgings that can withstand the dynamic stresses encountered during flight. As these aircraft are crucial for disaster response, military operations, and in locations where fixed-wing aircraft operation is impractical, this segment maintains a steady demand within the aerospace industry.

By Application Analysis

Airframe segment held a dominant position in the By Application category of the Aerospace Cold Forgings Market.

In 2023, the Aerospace Cold Forgings Market saw substantial growth and innovation, particularly within the By Application segment, where Airframe maintained a dominant market position. This segment includes crucial subcategories such as Airframe, Landing Gear, and Nacelle Component, each integral to the sector's advancement. The Airframe sub-segment, essential for constructing the aircraft's structural core, benefited significantly from advancements in materials science and precision forging techniques, enhancing the strength-to-weight ratio of airframes and thereby boosting fuel efficiency and performance. The push for high-strength, lightweight components that meet rigorous operational demands was a primary driver of market dominance in this area.

Simultaneously, the Landing Gear and Nacelle Components sub-segments witnessed significant technological enhancements. The Landing Gear, critical for aircraft safety and functionality, saw innovations in material composition and design, incorporating advanced aluminum and titanium alloys to meet demands for durability and reliability.

The Nacelle Component, which houses engines and other critical equipment, also advanced through the adoption of cold forging techniques aimed at improving resistance to environmental and thermal stress. These innovations, focused on reducing weight while maintaining structural integrity, underscored the industry's commitment to enhancing aircraft performance and safety, shaping the dynamics of the Aerospace Cold Forgings Market.

Key Market Segments

By Platform

- Fixed Wing

- Narrow-body

- Regional Jets

- Wide Body

- Fighter Jets

- Helicopters

- Rotary Wing

- Helicopters

By Application

- Airframe

- Landing Gear

- Nacelle Component

Growth Opportunity

Embracing Advanced Materials: The Rise of Titanium Alloys

As the aerospace industry continues to seek lighter, more durable components for enhanced performance and fuel efficiency, the demand for titanium alloys in cold forgings presents a significant growth opportunity in 2024. Titanium alloys, known for their high strength-to-weight ratio and corrosion resistance, are increasingly favored over traditional materials such as aluminum and steel. This shift not only supports the industry's drive towards weight reduction but also opens up new avenues for cold forging applications in critical aircraft structures and engine components. The adoption of titanium alloys is set to redefine market dynamics, pushing manufacturers to innovate and upgrade their forging capabilities to handle this advanced material.

Technological Innovations: Advancements in Precision Forging

Parallel to material innovations, technological advancements in precision forging are poised to transform the aerospace cold forgings market. Modern precision forging techniques enable the production of complex shapes with minimal material wastage, thereby enhancing the efficiency of the manufacturing process. These advancements are crucial for meeting the stringent quality and performance standards of the aerospace sector. As precision forging technologies evolve, they allow for tighter tolerances and improved mechanical properties, which are imperative in high-stress aerospace applications. The integration of these technologies will likely lead to better cost-effectiveness and resource efficiency, fostering growth and competitiveness within the market.

Latest Trends

Increasing Demand for Lightweight and Fuel-Efficient Aircraft Components

The aerospace industry continues to prioritize the development of lightweight and fuel-efficient aircraft components, primarily driven by stringent global emission standards and the ongoing need to enhance fuel economy. Cold forging, known for its ability to produce strong, lightweight structures, is increasingly favored for manufacturing critical aircraft parts such as fuselage components, engine mounts, and fasteners.

This trend is bolstered by the aerospace sector's recovery post-pandemic and the rising demand for new aircraft equipped with the latest technology for reduced environmental impact. Manufacturers leveraging cold forging techniques are likely to see substantial growth as airlines and aircraft manufacturers seek to minimize aircraft weight to meet both regulatory demands and operational cost savings.

Adoption of Advanced Materials

The integration of advanced materials in cold forging processes marks a significant trend reshaping the aerospace cold forgings market. Materials such as titanium and high-strength aluminum alloys are becoming more prevalent due to their superior properties, including high strength-to-weight ratios and corrosion resistance. These composite materials are particularly suited for the stringent demands of aerospace applications, offering enhanced performance and longevity.

The adoption of these advanced materials in cold forging allows for the production of more complex and precise components, catering to the evolving needs of aerospace engineering. As the market for these lightweight materials grows, suppliers and manufacturers investing in R&D to expand their capabilities in advanced material cold forgings will likely gain a competitive edge, aligning with industry demands for innovation and efficiency.

Regional Analysis

North America leads the global aerospace cold forgings market with a 40% market share.

In North America, the market is robust, driven by a strong aerospace manufacturing base in the United States and Canada. This region leads in the adoption of advanced manufacturing techniques, including cold forgings, which are crucial for producing high-strength, lightweight components for aerospace applications. North America dominates the global market, contributing approximately 40% of the total market share. The presence of major aerospace companies and extensive investment in aerospace R&D are key industry growth accelerants.

Europe follows closely, with its focus on enhancing aerospace infrastructure and increasing demand for fuel-efficient aircraft. Countries like France, Germany, and the UK are pivotal, bolstered by strong governmental support and the presence of giant aerospace conglomerates like Airbus.

The Asia Pacific region is rapidly emerging as a significant player due to expanding aerospace manufacturing in countries such as China, India, and Japan. Investments in new aerospace projects and regional collaborations are boosting the demand for cold forgings.

The Middle East & Africa, and Latin America, though smaller markets, are experiencing gradual growth rate. The Middle East benefits from increasing activities in aerospace hubs like the UAE, while Latin America is slowly expanding its aerospace capabilities through partnerships and foreign investments.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

In the rapidly evolving aerospace industry, the cold forgings market is expected to be prominently shaped by several key players in 2024. Among these, Arconic Corporation and Bharat Forge Limited stand out due to their extensive capabilities and innovative approaches in lightweight and high-strength forged components, crucial for aerospace applications. Arconic, with its established footprint and expertise in advanced manufacturing techniques, is poised to leverage its R&D capabilities to meet the increasing demands for efficiency and performance in aerospace structures. Bharat Forge, known for its diversified industrial presence, continues to expand its global reach and technological prowess, making significant strides in integrating digital technologies into its forging processes.

Companies like Scot Forge Company and Larsen & Toubro Ltd. also play critical roles, with Scot Forge emphasizing custom, high-quality forgings that reduce material waste and enhance structural integrity. Larsen & Toubro showcases its capacity to deliver large-scale projects, benefiting from India's growing focus on aerospace and defense manufacturing capabilities.

Moreover, smaller specialists like Somers Forge Ltd and Pacific Forge Inc. provide bespoke solutions that cater to specific aerospace needs, offering agility and specialized expertise that larger firms may not match. This ability to rapidly adapt and innovate is crucial in a market driven by stringent regulatory standards and the push towards more sustainable aviation solutions.

As the aerospace sector continues to pursue advancements in materials science and engineering to achieve greater fuel efficiency and performance, these key market players are expected to drive significant developments in the cold forgings market. Their contributions will likely be characterized by strategic partnerships, technological upgrades, and expansions in production capacities to accommodate the next generation of aerospace designs.

Market Key Players

- Arconic Corporation

- Bharat Forge Limited

- Scot Forge Company

- Larsen & Toubro Ltd.

- Jiangyin Hengrun Heavy Industries Co. Ltd.

- Consolidated Industries Inc.

- Somers Forge Ltd

- Pacific Forge Inc

- Precision Castparts

- Ellwood Group Inc

- All Metals & Forge Group

- Farinia Group

- Victoria Drop Forgings

- Mettis Group

Recent Development

- In January 2024, Goodluck India Ltd, a manufacturer of diverse steel products, announced a successful fundraising venture, securing approximately Rs 200 crore through the issuance of equity shares via Qualified Institutional Placement (QIP). The company specializes in producing a varied array of steel structures, including engineered constructions, precision/auto tubes, forging components for defense and aerospace applications, as well as CR (cold rolled) and GI (galvanized iron) pipes.

- In May 2023, the establishment of a new aerospace cold forgings facility in India was disclosed by RTI International. This facility is poised to specialize in the production of meticulously crafted forgings designed for employment in aircraft engine components and various other applications.

- In June 2023, an announcement was made regarding Scot Forge's plans to enhance its aerospace cold forgings facility located in Scotland. This strategic initiative aims to accommodate rapid growth within the sector and is anticipated to result in the creation of 50 new employment opportunities.

Report Scope

Report Features Description Market Value (2023) USD 2.13 billion Forecast Revenue (2033) USD 6.82 billion CAGR (2024-2032) 12.80% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Platform (Fixed Wing (Narrow-body, Regional Jets, Wide Body, Fighter Jets), Rotary Wing (Helicopters) ), By Application (Airframe, Landing Gear, Nacelle Component) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Arconic Corporation, Bharat Forge Limited, Scot Forge Company, Larsen & Toubro Ltd., Jiangyin Hengrun Heavy Industries Co. Ltd., Consolidated Industries Inc., Somers Forge Ltd, Pacific Forge Inc, Precision Castparts, Ellwood Group Inc, All Metals & Forge Group, Farinia Group, Victoria Drop Forgings, Mettis Group Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Arconic Corporation

- Bharat Forge Limited

- Scot Forge Company

- Larsen & Toubro Ltd.

- Jiangyin Hengrun Heavy Industries Co. Ltd.

- Consolidated Industries Inc.

- Somers Forge Ltd

- Pacific Forge Inc

- Precision Castparts

- Ellwood Group Inc

- All Metals & Forge Group

- Farinia Group

- Victoria Drop Forgings

- Mettis Group

Our Clients

View Our Licence Options