Acute Agitation And Aggression Treatment Market By Drug Class(Benzodiazepines, First-generation Anti-psychotics, Others), By Route of Administration(Oral, Intramuscular, Others), By Indication(Schizophrenia, Dementia, Others), By End User(Hospitals & Ambulatory Surgical Centers, Others),By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2023-2032

-

22244

-

Nov 2023

-

150

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

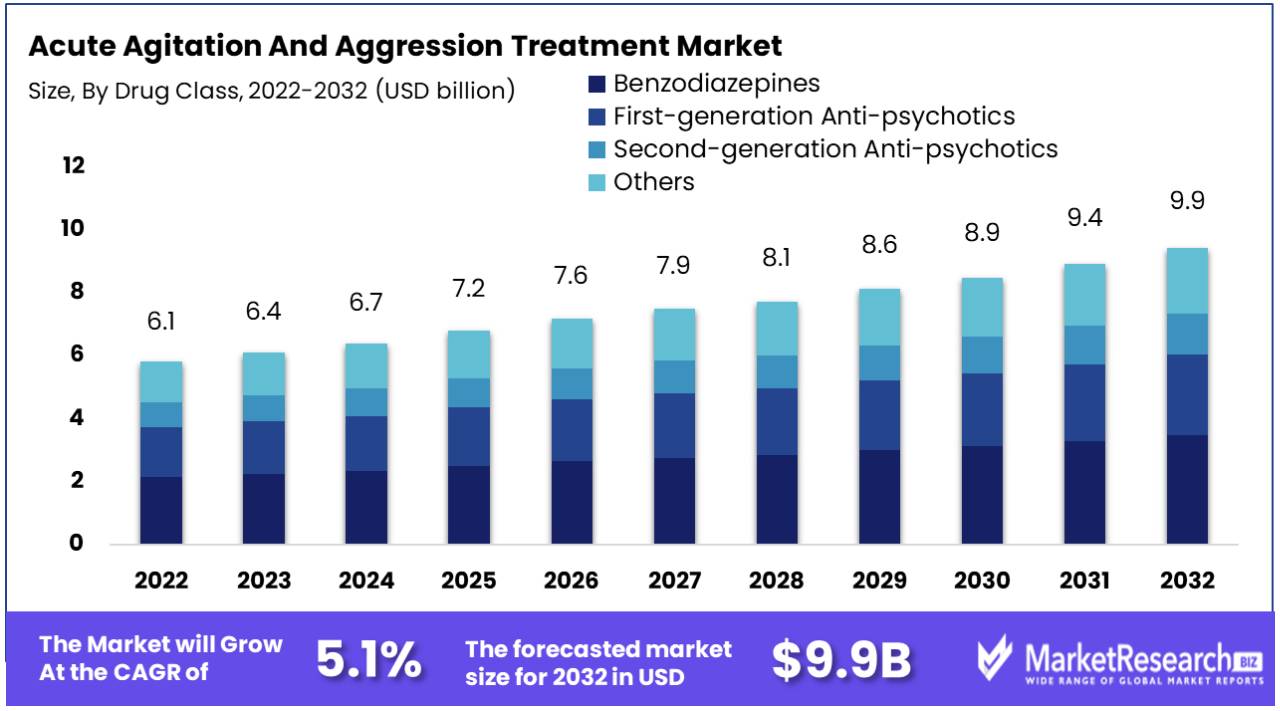

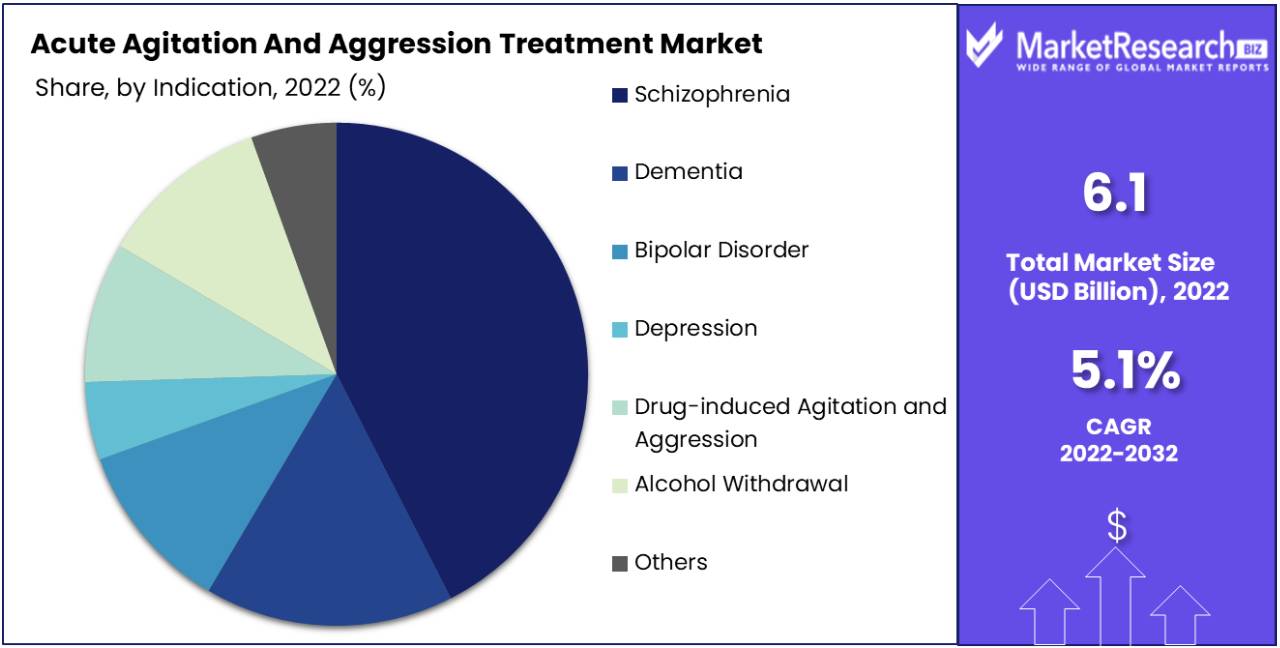

Acute Agitation And Aggression Treatment Market size is expected to be worth around USD 9.9 Bn by 2032 from USD 6.12 Bn in 2022, growing at a CAGR of 5.1% during the forecast period from 2023 to 2032.

Acute agitation is a state of uneasiness or tension with or without abnormal motor activity. Aggression denotes a behavioral manifestation of extreme stimulation that can be self-harm or harm to others. Enthusiasm and aggression are basically in the context of mental health care and need priority care from staff if detected. It is gaining popularity due to the surge in the agitation and aggression diagnoses in mental illness, which enhances the economic burden of mental illness, and the building of an organization to spread awareness.

The development of acute agitation and aggression management emphasizes the significance of quickly addressing rising symptoms and actively preventing the requirement for more restraining interventions like isolation and physical restraint. In recent years, drug deficiency has made treatment planning more difficult.

The limited amount of medicines has forced prescribers to use substitutes that they may not be accustomed to. This is problematic during acute arousal and aggression, where timely participation is vital. Moreover, there are numerous cases of acute agitation and aggression due to work stress and the surging burden of mental illness are some factors that are projected to drive market growth.

The most predominant mental and neurological disorders are Dementia and depression. Dementia affects nearly about 8%, whereas depression affects over 10% of the global older population. For instance, In February 2023, Emory University, Medical University of South Carolina, Northwell Health Hospital, PineRest Christian Mental Health Services, Mayo Clinic and McLean Hospital, and Harvard Medical School conducted research on the use of Electroconvulsive Therapy (ECT) for the treatment of refractory agitation and aggression in dementia.

A total of 15 papers were known for their research on mental illness. Among them, 10 papers showed evidence supporting the usage of BL ECT in patients undergoing treatment of refractory agitation and aggression in dementia. Among that research paper suggested the beginning of the treatment with RUL (Right Unilateral) placement. Furthermore, a comprehensive study highlighted the significance of RUL Ultra-Brief Pulse-Width as a treatment choice for the elderly population (aged >60 years). Moreover, three studies provided evidence showing that BL ECT could be a safe and effective substitute in cases where there is an inadequate response to unilateral ECT.

Additionally, new product innovations and growth are the main contributors to market expansion. For Example, in May 2022, the beginning of the TRANQUILITY II research marked a substantial milestone in the field of acute agitation treatment for Alzheimer's patients. It was conducted by BioXcel Therapeutics, this study primarily aims at BXCL501, a novel orally liquefying thin film preparation of dexmedetomidine. As a result, this growth is the main driving factor for market expansion in the coming future.

Driving factors

Innovative Therapies Set New Standards in the Acute Agitation and Aggression Treatment Market

The acute agitation and aggression treatment market is significantly impacted by advances in both pharmacological and non-pharmacological interventions. The development of new psychiatric medications that target the underlying causes of agitation with fewer side effects has been crucial. On the non-pharmacological front, therapies such as cognitive behavioral therapy (CBT), mindfulness, and environmental modifications are being integrated into treatment plans, offering a holistic approach.

The market has seen the introduction of atypical antipsychotics and other novel drug classes that offer improved efficacy and safety profiles. Concurrently, there is a growing emphasis on personalized medicine, where treatments are tailored to the individual's genetic makeup, potentially improving outcomes. These advancements are crucial in a market where the tolerance for side effects is low and the demand for patient-centered care is high.

The integration of these novel therapies is expected to not only continue but accelerate, given the ongoing investment in research and development. In the long term, these advances will likely establish new treatment paradigms, solidify the role of multidisciplinary approaches, and expand the market as these therapies become more accessible and standard in care practices.

Increasing Mental Health Cases Propel Market Growth

The increasing number of cases regarding mental health conditions directly contributes to the expansion of the acute agitation and aggression treatment market. The prevalence of mental health disorders, such as bipolar disorder, schizophrenia, and depression, which are often associated with episodes of acute agitation and aggression, is on the rise globally. This increase is driving the demand for effective management strategies and treatments.

The uptick in mental health cases can be attributed to a variety of factors, including better diagnostic tools, reduced stigma, and increased stress levels in modern society. With the World Health Organization citing depression as a leading cause of disability worldwide, the urgency for effective treatments has never been clearer. As awareness grows, so does the recognition of the need for intervention, resulting in a broader patient demographic seeking treatment.

Economic Burden of Mental Illness Necessitates Market Growth

The economic burden of mental illness is a powerful motivator in the growth of the acute agitation and aggression treatment market. The costs associated with mental illness are substantial, encompassing not only healthcare expenditures but also lost productivity and social services support. Effective management and treatment of acute agitation and aggression can significantly reduce these costs.

Healthcare systems worldwide are recognizing that investing in treatment not only improves patient outcomes but can also result in substantial economic savings. Thus, there is a push towards developing treatments that can reduce hospitalization rates, decrease the need for emergency care, and allow individuals to maintain their role in the workforce.

Changing Attitudes Toward Mental Illness Expand Market Reach

Changing attitudes toward mental illness has a profound impact on the acute agitation and aggression treatment market. As stigma decreases, there is a greater willingness among individuals to seek help and adhere to treatment plans. Societal acceptance can also lead to better funding for mental health services and more significant investment in research.

This shift in perception is likely to increase the utilization of mental health services and, consequently, the demand for treatments. It also opens the door for innovative care models, such as community-based support and digital health interventions, which can make treatment more accessible.

Availability of Safer Treatments Spurs Market Evolution

The availability of safer and more effective treatments is a critical growth factor for the acute agitation and aggression treatment market. As research delivers new insights into the pathophysiology of mental health disorders, treatments are becoming more sophisticated, moving away from a one-size-fits-all approach to targeted therapies with improved safety profiles.

The development of medications with reduced risks of side effects and non-pharmacological interventions with proven efficacy means that patients have more options than ever before. This expansion of the treatment repertoire not only improves patient outcomes but also enhances compliance, a crucial component of effective long-term management.

Restraining Factors

High Cost of Treatment Restrains Acute Agitation and Aggression Treatment Market Growth

The treatment of acute agitation and aggression often entails the use of costly medications, specialized therapeutic interventions, and potentially prolonged hospital stays, all of which contribute to the high cost of care. These expenses can be a significant barrier for patients, particularly in the absence of adequate insurance coverage or in healthcare systems with less financial support for mental health. The high cost reduces the accessibility and affordability of treatment, limiting the market's growth potential as many patients may forgo or seek alternative, less effective treatments.

Stigma Associated with Mental Illness Restrains Market Growth

Stigma associated with mental illness continues to act as a major player impediment to the growth of the acute agitation and aggression treatment market. The societal stigma can prevent individuals from seeking treatment due to fear of discrimination or misunderstanding. This not only reduces the number of patients accessing available treatments but also can impact the willingness of healthcare providers to specialize in this field, further exacerbating the problem. The stigma effectively diminishes market demand and can limit investment in the development of new and improved treatment options.

Segmentation Analysis of Acute Agitation And Aggression Treatment Market

By Drug Class Analysis

Benzodiazepines constitute the dominant drug class in the treatment of acute agitation and aggression due to their rapid onset of action and efficacy in reducing acute symptoms. The segment’s predominance is also due to its widespread use and familiarity among medical professionals in both hospital and outpatient settings.

First-generation antipsychotics, while effective, are associated with a higher risk of side effects and are increasingly being replaced by second-generation anti-psychotics, which have a more favorable side effect profile. Other treatments include mood stabilizers and off-label medications, which play a role in cases where patients have specific treatment requirements or co-morbid conditions.

By Route of Administration Analysis

Oral administration is the most common route due to its convenience, patient compliance, and safety profile. In the context of long-term management of chronic psychiatric conditions, oral medications are preferred for ongoing treatment.

Intramuscular injections are critical in emergencies where rapid control of symptoms is necessary and the patient may be non-compliant or unable to take oral segment medication. Other routes, including intravenous administration, are less common and typically reserved for more controlled settings.

By Indication Analysis

Schizophrenia is a leading indication for the treatment of acute agitation and aggression due to the nature of the disease, which often presents with these symptoms. Treatment for schizophrenia represents a significant portion of the market, given the chronic nature of the disease and the necessity for ongoing medication management.

Other indications include dementia segment and bipolar disorder, where agitation and aggression can be prominent symptoms. Depression can also present with agitation, and drug-induced agitation and aggression are common in emergency departments. Alcohol withdrawal is another area where these medications are essential. Each of these segments contributes to the overall market, addressing the specific needs of these patient populations.

By End User Analysis

Hospitals and ambulatory surgical centers are the primary end-users due to the need for immediate intervention in acute cases. The controlled environment allows for rapid administration and monitoring of medication effects, which is critical for patient safety.

Psychiatric care facilities also represent a key segment, providing ongoing treatment for patients with chronic conditions. Other settings may include general practice and community health centers where initial treatment or stabilization may occur before transfer to a specialized setting.

The acute agitation and aggression treatment market is driven by the need for effective and rapid symptom control in various psychiatric and neurological conditions. Benzodiazepines lead the market, with oral administration being the most common route due to its ease of use and patient compliance. Schizophrenia remains the primary indication for these treatments, while hospitals and ambulatory surgical centers are the main end-users, reflecting the urgency and severity of cases typically encountered in these settings. Each segment is integral to the overall market, catering to the diverse needs of the patient population.

Key Market Segments

By Drug Class

- Benzodiazepines

- First-generation Anti-psychotics

- Second-generation Anti-psychotics

- Others

By Route of Administration

- Oral

- Intramuscular

- Others

By Indication

- Schizophrenia

- Dementia

- Bipolar Disorder

- Depression

- Drug-induced Agitation and Aggression

- Alcohol Withdrawal

- Others

By End User

- Hospitals & Ambulatory Surgical Centers

- Psychiatric Care Facilities

- Others

Growth Opportunity

Improved Adherence Treatment Options Offer Growth Opportunity in Agitation and Aggression Treatment

Developing treatment options that enhance patient adherence presents a considerable growth opportunity in the acute agitation and aggression treatment market. Improved adherence correlates with better patient outcomes and reduced healthcare costs, which is a compelling factor for healthcare providers and payers.

Telemedicine Adoption Offers Market Growth for Acute Agitation and Aggression Treatment

Adopting telemedicine in regions with limited healthcare access can significantly expand the acute agitation and aggression treatment market. Telemedicine can bridge the gap between patients and providers, ensuring timely intervention for acute episodes. With the telehealth sector projected to grow exponentially in the coming years, incorporating these services for acute agitation and aggression treatments can broaden the reach of healthcare providers and allow for early management of these conditions, potentially reducing the incidence of severe cases.

Integrated Care Models Offer Market Expansion for Agitation Treatment

Integrated care models, which encourage collaboration between various healthcare departments, provide a growth opportunity for the treatment of acute agitation and aggression.

Customized Treatment Plans Offer Personalized Growth in the Agitation Treatment Market

Providing customized treatment plans for patients with acute agitation and aggression is key to market growth. Personalization in healthcare is becoming increasingly important, as it can lead to better patient outcomes and satisfaction.

Regional Analysis

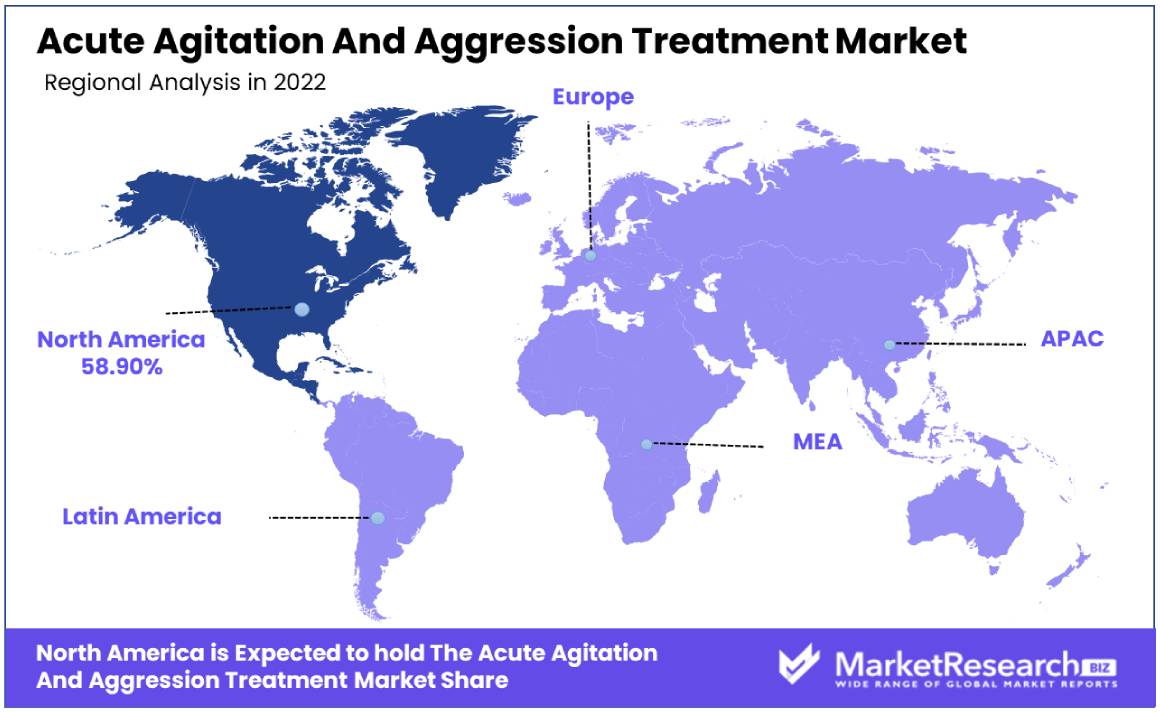

North America Dominates with a 58.90% Market Share in the Acute Agitation and Aggression Treatment Market

North America holds a substantial 58.90% share in the acute agitation and aggression treatment market, a testament to the region's robust healthcare infrastructure and the prevalence of psychiatric conditions. Key factors driving this dominance include high awareness of mental health issues, comprehensive coverage of healthcare services, and significant investment in research and development for psychiatric medications and therapies.

The market dynamics are characterized by the strong presence of global pharmaceutical key companies and healthcare providers, collaborative research efforts between academic institutions and industry, and supportive government policies for mental health initiatives. Moreover, there is a substantial patient population seeking treatment for conditions associated with acute agitation and aggression, such as schizophrenia, bipolar disorder, and dementia care products, which fuels demand for these treatments.

Europe: A Strong Contender in the Acute Agitation and Aggression Treatment Market

Europe also represents a significant share of the acute agitation and aggression treatment market. The region's approach to healthcare, with universal coverage systems in many countries, allows for accessible treatment options for patients with psychiatric disorders. Investments in mental health, particularly in acute care, coupled with a growing elderly population susceptible to neurodegenerative diseases, contribute to the market's strength.

Asia-Pacific: An Expanding Market in Acute Agitation and Aggression Treatment

The Asia-Pacific region, while currently holding a smaller share of the acute agitation and aggression treatment market, shows significant growth potential. Factors such as improving healthcare infrastructures, increasing awareness of mental health, and economic development contribute to the expansion of the market.

The region faces challenges due to diverse healthcare systems and varying levels of access to care. However, with the increasing prevalence of psychiatric conditions and a large, aging population, demand for treatment options is expected to rise. Future market influence will likely grow as healthcare access improves and awareness of mental health increases across the region.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of Asia Pacific

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of Middle East & Africa

Key Players Analysis

The acute agitation and aggression treatment market is shaped by the contributions of a consortium of key pharmaceutical entities. Eli Lilly and Company, Pfizer Inc., and Johnson & Johnson are distinguished by their extensive portfolios and substantial R&D investments, which enable them to lead in the innovation of therapeutic solutions. Their strategic positioning is further reinforced by robust global sales and distribution networks, which enhance their market influence and patient outreach.

Otsuka Pharmaceutical Co., Ltd. and Bristol-Myers Squibb stand out for their collaborative efforts in developing and marketing novel antipsychotic treatments, which have become pivotal in setting clinical standards. H. Lundbeck A/S and AstraZeneca plc emphasize their specialized focus on CNS disorders, thus positioning themselves as key players in niche segment growth of the market.

Teva Pharmaceutical Industries Ltd., Novartis AG, and Merck & Co., Inc. have expanded their market influence through generic offerings, increasing the accessibility and affordability of treatments. Sanofi S.A. and AbbVie Inc. leverage their global presence to address unmet needs in this therapeutic area, with a keen focus on patient-centric healthcare solutions.

Overall, the collective efforts of these companies underscore a dynamic market environment, wherein strategic collaborations, therapeutic advancements, and a focus on accessibility define the competitive landscape of acute agitation and aggression treatment options.

Top Key Players in the Acute Agitation And Aggression Market

- Eli Lilly and Company

- Pfizer Inc.

- Otsuka Pharmaceutical Co., Ltd.

- GlaxoSmithKline plc

- H. Lundbeck A/S

- Johnson & Johnson

- Bristol-Myers Squibb

- Teva Pharmaceutical Industries Ltd.

- Novartis AG

- AstraZeneca plc

- Merck & Co., Inc.

- Sanofi S.A.

- AbbVie Inc.

- Allergan plc

- Valeant Pharmaceuticals International, Inc.

Recent Development

- In 2023, a clinical trial is investigating Sativex®, a cannabinoid-based medicine (CBM), for managing agitation in dementia. The trial assesses Sativex's safety, feasibility, and efficacy in nursing home settings. In 2023, a clinical trial is investigating Sativex®, a cannabinoid-based medicine (CBM), for managing agitation in dementia. The trial assesses Sativex's safety, feasibility, and efficacy in nursing home settings to inform a potential phase III trial.

- In May 2023, the FDA granted its first approval for a medication to address agitation symptoms in individuals with Alzheimer 's-related dementia. Rexulti (brexpiprazole) oral tablets have received supplemental approval from the U.S. Food and Drug Administration, marking the inaugural FDA-approved therapy for this specific condition.

- In 2023, NRL-4, made by Neurelis, is a proprietary nasal spray formulation of olanzapine, an antipsychotic medication that is currently approved for the treatment of schizophrenia and bipolar disorder. Neurelis is expected to begin clinical trials of NRL-4 in the fourth quarter of 2023."

Report Scope

Report Features Description Market Value (2022) USD 6.12 Bn Forecast Revenue (2032) USD 9.9 Bn CAGR (2023-2032) 5.1% Base Year for Estimation 2022 Historic Period 2016-2022 Forecast Period 2023-2032 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Drug Class(Benzodiazepines, First-generation Anti-psychotics, Second-generation Anti-psychotics, Others), By Route of Administration(Oral, Intramuscular, Others), By Indication(Schizophrenia, Dementia, Bipolar Disorder, Depression, Drug-induced Agitation and Aggression, Alcohol Withdrawal, Others), By End User(Hospitals & Ambulatory Surgical Centers, Psychiatric Care Facilities, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Eli Lilly and Company, Pfizer Inc., Otsuka Pharmaceutical Co., Ltd., GlaxoSmithKline plc, H. Lundbeck A/S, Johnson & Johnson, Bristol-Myers Squibb, Teva Pharmaceutical Industries Ltd., Novartis AG, AstraZeneca plc, Merck & Co., Inc., Sanofi S.A., AbbVie Inc., Allergan plc, Valeant Pharmaceuticals International, Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Eli Lilly and Company

- Pfizer Inc.

- Otsuka Pharmaceutical Co., Ltd.

- GlaxoSmithKline plc

- H. Lundbeck A/S

- Johnson & Johnson

- Bristol-Myers Squibb

- Teva Pharmaceutical Industries Ltd.

- Novartis AG

- AstraZeneca plc

- Merck & Co., Inc.

- Sanofi S.A.

- AbbVie Inc.

- Allergan plc

- Valeant Pharmaceuticals International, Inc.

Our Clients

View Our Licence Options