Ophthalmic Lasers Market By Type (Photocoagulation Lasers, Nd:YAG Lasers, Excimer Lasers, Femtosecond Lasers, Diode Lasers), By Application (Refractive Error Correction, Cataract Surgery, Glaucoma Surgery, Posterior Capsulotomy), By End User (Hospitals, Ambulatory Service Centers, Clinics), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

49156

-

July 2024

-

136

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

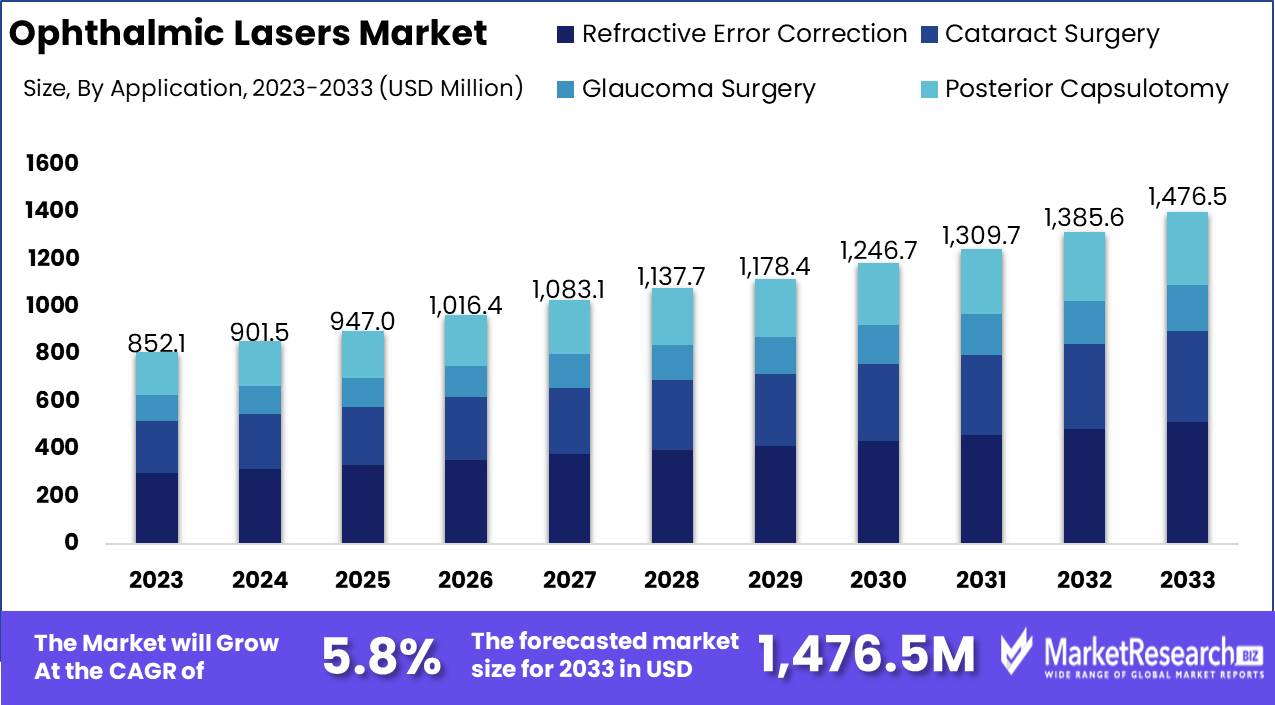

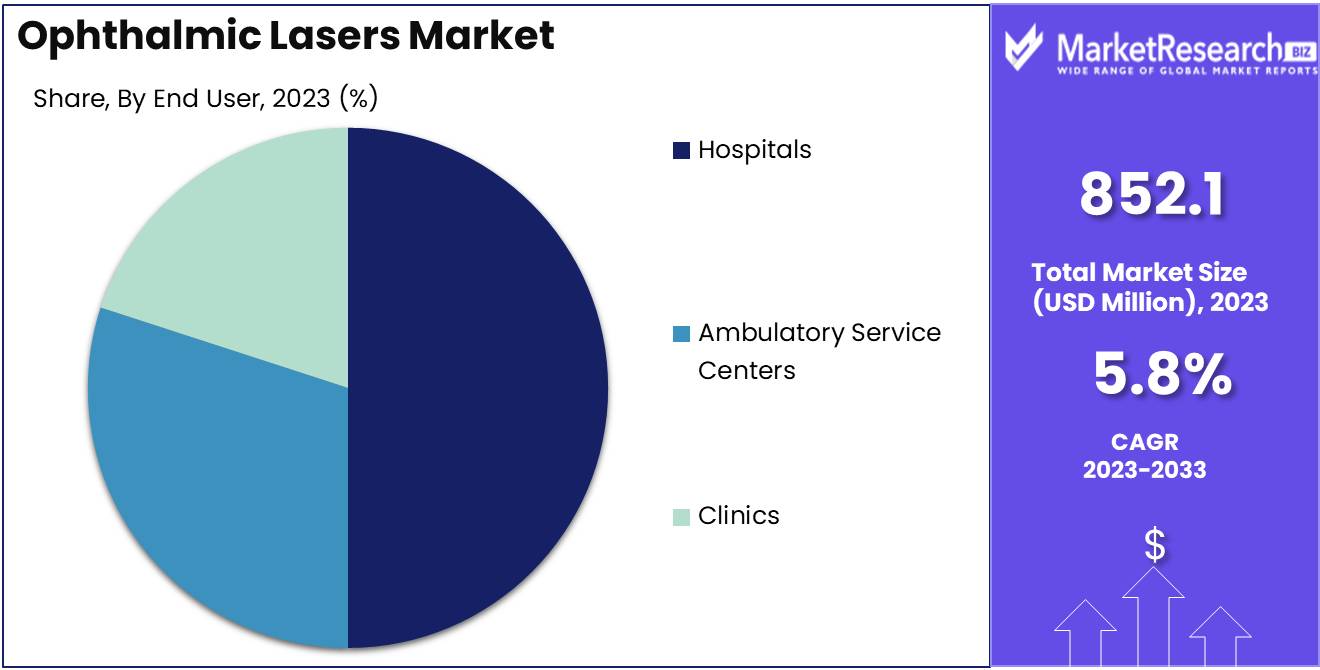

The Global Ophthalmic Lasers Market was valued at USD 852.1 Mn in 2023. It is expected to reach USD 1476.5 Mn by 2033, with a CAGR of 5.8% during the forecast period from 2024 to 2033.

The Ophthalmic Lasers Market involves the development, production, and utilization of laser technologies for eye care treatments. These lasers are used for a variety of ophthalmic procedures, including refractive error correction, cataract surgery, glaucoma treatment, and retinal disorders. The market is driven by advancements in laser technology, increasing prevalence of eye diseases, and growing demand for minimally invasive surgical procedures. Ophthalmic lasers offer precision, reduced recovery times, and improved patient outcomes, making them a preferred choice for both patients and healthcare providers. The market is supported by continuous innovation and increasing investments in the healthcare sector.

The Ophthalmic Lasers Market is poised for substantial growth, driven by technological advancements, increasing incidence of eye disorders, and a rising preference for minimally invasive procedures. Ophthalmic lasers provide unparalleled precision and effectiveness in treating various eye conditions, making them indispensable in modern ophthalmology. One of the significant drivers is the widespread adoption of LASIK procedures for refractive error correction, which has been performed on over 40 million people worldwide. This high adoption rate underscores the effectiveness and reliability of laser-based treatments.

The Ophthalmic Lasers Market is poised for substantial growth, driven by technological advancements, increasing incidence of eye disorders, and a rising preference for minimally invasive procedures. Ophthalmic lasers provide unparalleled precision and effectiveness in treating various eye conditions, making them indispensable in modern ophthalmology. One of the significant drivers is the widespread adoption of LASIK procedures for refractive error correction, which has been performed on over 40 million people worldwide. This high adoption rate underscores the effectiveness and reliability of laser-based treatments.Laser safety is a critical aspect of this market. The use of laser safety glasses, which provide an optical density (OD) of 5-7, ensures protection against specific laser wavelengths, enhancing safety protocols during procedures. This emphasis on safety complements the advanced capabilities of ophthalmic lasers, contributing to their growing popularity.

Institutions like the University Hospitals Cleveland Medical Center have reported operational efficiencies and reduced staffing needs following the implementation of advanced laser systems such as the BD Kiestra TLA. This reduction in staffing by 20% highlights the cost-effectiveness and efficiency of automated laser systems in clinical settings.

The market is also benefiting from continuous innovation and increased investments in the healthcare sector. Companies are developing new laser technologies that offer improved outcomes and expanded treatment options. The growing aging population and rising prevalence of chronic eye diseases further propel the demand for ophthalmic lasers.

Key Takeaways

- Market Growth: The Global Ophthalmic Lasers Market was valued at USD 852.1 Mn in 2023. It is expected to reach USD 1476.5 Mn by 2033, with a CAGR of 5.8% during the forecast period from 2024 to 2033.

- By Type: Photocoagulation Lasers have a 30% market share, widely used for treating retinal disorders and vision correction.

- By Application: Refractive Error Correction is a leading application, accounting for 35%, due to increasing prevalence of vision impairments.

- By End User: Hospitals are the primary users, holding 50% of the market, essential for delivering specialized ophthalmic treatments.

- Regional Dominance: North America has a 36% share, influenced by technological advancements and high healthcare spending.

- Growth Opportunity: Developing compact, cost-effective laser systems can broaden access to advanced ophthalmic care in underserved regions.

Driving factors

Increasing Prevalence of Eye Disorders

The rising incidence of eye disorders such as glaucoma, cataracts, and diabetic retinopathy is a primary driver of the ophthalmic lasers market. According to the World Health Organization, approximately 2.2 billion people globally have a vision impairment, with at least 1 billion of these cases preventable or treatable. Ophthalmic lasers offer precise and effective treatment options for these conditions, enhancing patient outcomes and driving market growth. As the prevalence of these disorders continues to rise, the demand for advanced laser treatments will correspondingly increase.

Advancements in Laser Technology

Technological advancements in laser technology significantly contribute to the growth of the ophthalmic lasers market. Innovations such as femtosecond lasers and selective laser trabeculoplasty (SLT) provide more accurate, less invasive, and highly effective treatment options. These advancements not only improve the precision and safety of ophthalmic procedures but also expand the range of treatable conditions. The continuous development of laser technology enhances its therapeutic efficacy, making it a preferred choice among ophthalmologists and patients alike.

Growing Aging Population

The global aging population is another critical factor driving the ophthalmic lasers market. As people age, the likelihood of developing eye disorders increases, leading to a higher demand for effective treatment solutions. The United Nations reports that by 2050, one in six people will be over the age of 65. This demographic shift significantly boosts the need for ophthalmic lasers, which are essential in managing age-related eye conditions, thereby driving market growth.

Restraining Factors

High Cost of Laser Treatment

The high cost of laser treatment is a notable restraining factor for the ophthalmic lasers market. Advanced laser systems and procedures are often expensive, making them less accessible to patients in lower-income regions or without adequate insurance coverage. This financial barrier can limit the widespread adoption of ophthalmic lasers, impacting market growth.

Regulatory and Safety Concerns

Regulatory and safety concerns also pose challenges to the ophthalmic lasers market. Stringent regulations governing the approval and use of medical lasers ensure patient safety but can slow down the introduction of new technologies. Additionally, concerns about the potential risks and side effects associated with laser treatments can hinder market expansion. Manufacturers must navigate these regulatory landscapes carefully to ensure compliance and maintain market growth.

By Type Analysis

Photocoagulation Lasers dominated the By Type segment of the Ophthalmic Lasers Market in 2023, capturing more than a 30% share.

In 2023, Photocoagulation Lasers held a dominant market position in the By Type segment of the Ophthalmic Lasers Market, capturing more than a 30% share. This significant market share is driven by the widespread use of photocoagulation lasers in treating retinal disorders such as diabetic retinopathy and retinal vein occlusion. The effectiveness of these lasers in preventing vision loss by sealing leaking blood vessels and reducing retinal swelling makes them a crucial tool in ophthalmology.

Nd:YAG Lasers are extensively used for posterior capsulotomy and peripheral iridotomy procedures. These lasers are valued for their precision and efficacy in treating secondary cataracts and glaucoma. Despite their importance, their market share is smaller than photocoagulation lasers due to the more specialized nature of their applications.

Excimer Lasers are primarily used in refractive surgeries such as LASIK and PRK to correct vision issues by reshaping the cornea. These lasers offer high precision and effectiveness, contributing to significant demand in the ophthalmic market.

Femtosecond Lasers are advanced lasers used in both refractive surgery and cataract surgery. They provide high precision in cutting and shaping tissues, improving surgical Lasers outcomes. While growing in adoption, their market share remains smaller due to their high cost and the need for specialized training.

Diode Lasers are used for a variety of ophthalmic treatments, including glaucoma and retinal therapies. They are appreciated for their compact size and versatility. Despite these benefits, their market share is less than photocoagulation lasers due to their specific use cases and lower overall demand.

By Application Analysis

Refractive Error Correction dominated the By Application segment of the Ophthalmic Lasers Market in 2023, capturing more than a 35% share.

In 2023, Refractive Error Correction held a dominant market position in the By Application segment of the Ophthalmic Lasers Market, capturing more than a 35% share. This leadership is driven by the high demand for corrective vision procedures such as LASIK and PRK, which use excimer and femtosecond lasers. The increasing prevalence of myopia, hyperopia, and astigmatism, along with a growing preference for laser-based correction over traditional eyeglasses or smart contact lenses, significantly contributes to the market dominance of refractive error correction.

Cataract Surgery is another crucial application to improve surgical precision and outcomes. The rising aging population and the increasing incidence of cataracts drive the demand for advanced laser technologies in cataract surgery.

Glaucoma Surgery procedures are essential for managing intraocular pressure and preventing vision loss in glaucoma patients. Despite its importance, the market share for glaucoma surgery is less than that of refractive error correction due to the chronic nature of glaucoma and the ongoing management it requires.

Posterior Capsulotomy, a procedure primarily performed to treat secondary cataracts, is vital for restoring vision clarity post-cataract surgery. While crucial, its market share is smaller compared to refractive error correction due to the specific postoperative nature of the procedure.

By End User Analysis

Hospitals dominated the By End User segment of the Ophthalmic Lasers Market in 2023, capturing more than a 50% share.

In 2023, Hospitals held a dominant market position in the By End User segment of the Ophthalmic Lasers Market, capturing more than a 50% share. This significant market share is attributed to the comprehensive range of ophthalmic treatments and surgeries performed in hospital settings. Hospitals are equipped with advanced laser technologies and have access to skilled ophthalmologists, making them primary centers for both routine and complex eye procedures. The ability to handle high patient volumes and provide specialized care supports the dominance of hospitals in the ophthalmic lasers market.

Ambulatory Service Centers (ASCs) are also key players, offering a cost-effective and efficient alternative for various eye surgeries, including laser procedures. ASCs are increasingly popular for elective surgeries such as LASIK and cataract removal due to their convenience and shorter wait times.

Clinics provide essential ophthalmic care and laser treatments, particularly for routine eye exams and minor procedures. Clinics offer personalized care and convenience, attracting a steady patient base.

Key Market Segments

By Type

- Photocoagulation Lasers

- Nd:YAG Lasers

- Excimer Lasers

- Femtosecond Lasers

- Diode Lasers

By Application

- Refractive Error Correction

- Cataract Surgery

- Glaucoma Surgery

- Posterior Capsulotomy

By End User

- Hospitals

- Ambulatory Service Centers

- Clinics

Growth Opportunity

Development of Multifunctional Lasers

The development of multifunctional lasers represents a significant growth opportunity for the ophthalmic lasers market in 2024. Multifunctional lasers capable of performing various ophthalmic procedures, such as refractive surgery, cataract removal, and glaucoma treatment, can streamline clinical workflows and reduce equipment costs. This versatility not only enhances treatment efficiency but also makes advanced laser technologies more accessible to a broader range of healthcare providers. As the demand for comprehensive and cost-effective solutions grows, multifunctional lasers will likely gain traction in the market.

Rising Demand for Minimally Invasive Surgeries

The increasing demand for minimally invasive surgeries is another key opportunity for the ophthalmic lasers market. Minimally invasive laser procedures offer numerous benefits, including reduced recovery times, lower risk of complications, and improved patient comfort. As patients and healthcare providers continue to seek out these advantages, the adoption of laser-based treatments is expected to rise. This trend towards less invasive options aligns with broader healthcare objectives of improving patient outcomes and reducing healthcare costs, driving further market growth.

Latest Trends

Adoption of Femtosecond Laser Technology

The adoption of femtosecond laser technology is a prominent trend expected to shape the ophthalmic lasers market in 2024. Femtosecond lasers provide unparalleled precision and control, enabling highly accurate corneal and lens surgeries. This technology has revolutionized procedures such as LASIK and cataract surgery, offering improved safety and outcomes. As more ophthalmic practices integrate femtosecond lasers into their offerings, the market for this advanced technology is poised for substantial growth.

Integration of Lasers with Imaging Systems

The integration of lasers with advanced imaging systems is another significant trend in the ophthalmic lasers market. Combining laser technology with imaging modalities like optical coherence tomography (OCT) enhances diagnostic accuracy and treatment precision. This integration allows for real-time visualization and feedback during procedures, improving clinical outcomes and patient satisfaction. As technology continues to evolve, the synergistic use of lasers and imaging systems will drive innovation and expand the capabilities of ophthalmic treatments.

Regional Analysis

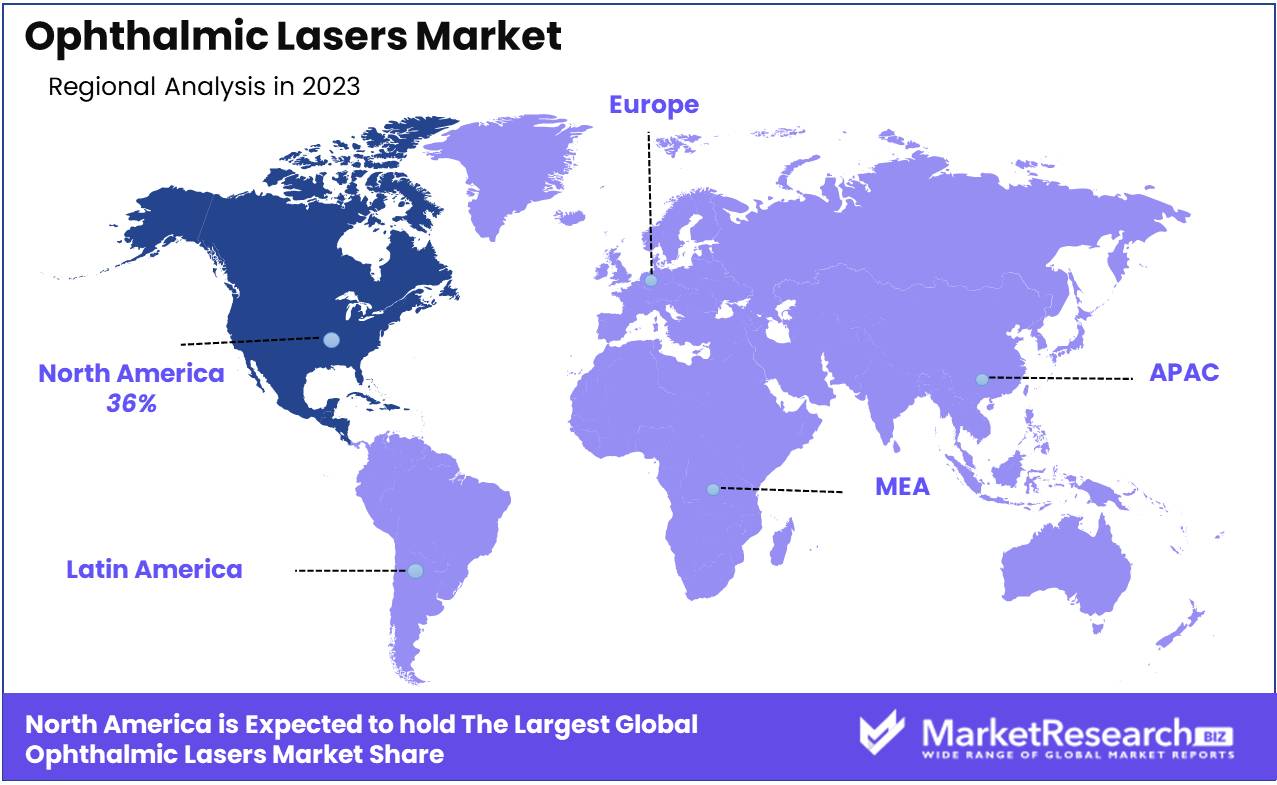

Ophthalmic Lasers Market by Region: North America, Europe, Asia Pacific, Middle East & Africa, Latin America

In 2023, North America dominated the Ophthalmic Lasers Market, capturing a substantial 36% share. This leadership is driven by the region's advanced healthcare infrastructure, high prevalence of eye disorders, and significant investment in medical technology. The United States and Canada lead the market with widespread adoption of ophthalmic lasers for procedures such as cataract surgery, glaucoma treatment, and refractive surgeries. The presence of major market players and continuous technological advancements further support market growth in this region.

Europe holds a significant share in the ophthalmic lasers market, driven by a high prevalence of eye diseases and a strong focus on healthcare innovation. The region's commitment to healthcare excellence and investment in medical research support the market's substantial share.

Asia Pacific is experiencing rapid growth in the ophthalmic lasers market, fueled by increasing healthcare investments, rising incidences of eye disorders, and improving healthcare infrastructure. The region's large population base and growing demand for advanced eye care solutions drive market expansion. Despite the fast-paced growth, Asia Pacific's market share remains developing compared to the established markets in North America and Europe.

Middle East & Africa show promising potential for growth in the ophthalmic lasers market, supported by increasing investments in healthcare infrastructure and efforts to enhance eye care services. The adoption of advanced ophthalmic laser technologies is gradually increasing, driven by the need to improve eye care outcomes.

Latin America is emerging as a growing market for ophthalmic lasers, with Brazil and Mexico leading the demand. The region benefits from improvements in healthcare infrastructure and a growing focus on enhancing eye care services.

Key Regions and Countries

North America

- US

- Canada

- Mexico

Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

The global ophthalmic lasers market is set to experience robust growth in 2024, driven by rising incidences of ocular disorders and advancements in laser technology. Key players such as Abbott Medical Optics, Inc., Alcon Inc. (Novartis AG), and Bausch & Lomb Incorporated are leading the market with their innovative products and strong market presence.

Abbott Medical Optics, Inc. remains a key player with its comprehensive range of ophthalmic lasers for various applications, including cataract surgery and refractive procedures. Their focus on product innovation and patient outcomes positions them well in the competitive market landscape.

Alcon Inc. (Novartis AG) and Bausch & Lomb Incorporated continue to dominate the market with their extensive product portfolios and strong distribution networks. Their commitment to advancing laser technology and improving patient care ensures they remain at the forefront of the ophthalmic lasers market.

LENSAR, LLC and NIDEK CO., LTD are enhancing their market presence through continuous product development and strategic partnerships. Their focus on developing advanced laser systems for cataract and refractive surgery caters to the growing demand for minimally invasive procedures.

iVIS Technologies and ZEISS International leverage their strong technological foundations to offer cutting-edge laser systems for ophthalmic applications. Their emphasis on precision and innovation ensures they remain competitive in the evolving market.

Ziemer Ophthalmic Systems AG and SCHWIND eye-tech-solutions GmbH & Co. KG are expanding their market reach through innovative product offerings and strategic collaborations. Their focus on developing advanced laser technologies for vision correction aligns with the increasing demand for effective and safe ophthalmic procedures.

Market Key Players

- Abbott Medical Optics, Inc.

- Alcon Inc. (Novartis AG)

- Bausch & Lomb Incorporated

- LENSAR, LLC

- NIDEK CO., LTD

- iVIS Technologies

- ZEISS International

- Ziemer Ophthalmic Systems AG

- SCHWIND eye-tech-solutions GmbH & Co. KG

Recent Development

- In June 2024, Alcon introduced the next-generation ARGOS biometer, enhancing precision in cataract surgery.

- In May 2024, ZEISS launched VISULAS green, a new ophthalmic laser system for retinal treatments

Report Scope

Report Features Description Market Value (2023) USD 852.1 Mn Forecast Revenue (2033) USD 1476.5 Mn CAGR (2024-2033) 5.8% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Photocoagulation Lasers, Nd:YAG Lasers, Excimer Lasers, Femtosecond Lasers, Diode Lasers), By Application (Refractive Error Correction, Cataract Surgery, Glaucoma Surgery, Posterior Capsulotomy), By End User (Hospitals, Ambulatory Service Centers, Clinics) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Abbott Medical Optics, Inc., Alcon Inc. (Novartis AG), Bausch & Lomb Incorporated, LENSAR, LLC, NIDEK CO., LTD, iVIS Technologies, ZEISS International, Ziemer Ophthalmic Systems AG, SCHWIND eye-tech-solutions GmbH & Co. KG Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Abbott Medical Optics, Inc.

- Alcon Inc. (Novartis AG)

- Bausch & Lomb Incorporated

- LENSAR, LLC

- NIDEK CO., LTD

- iVIS Technologies

- ZEISS International

- Ziemer Ophthalmic Systems AG

- SCHWIND eye-tech-solutions GmbH & Co. KG

Our Clients

View Our Licence Options