Cardiology Pacs Market By Component (Software, Hardware, Services), By Deployment (Cloud, On-premise), By End-user (Hospitals & Clinics, Diagnostic Centres, Ambulatory Surgical Centres, Catheterisation Laboratories, Others), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

50669

-

August 2024

-

300

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

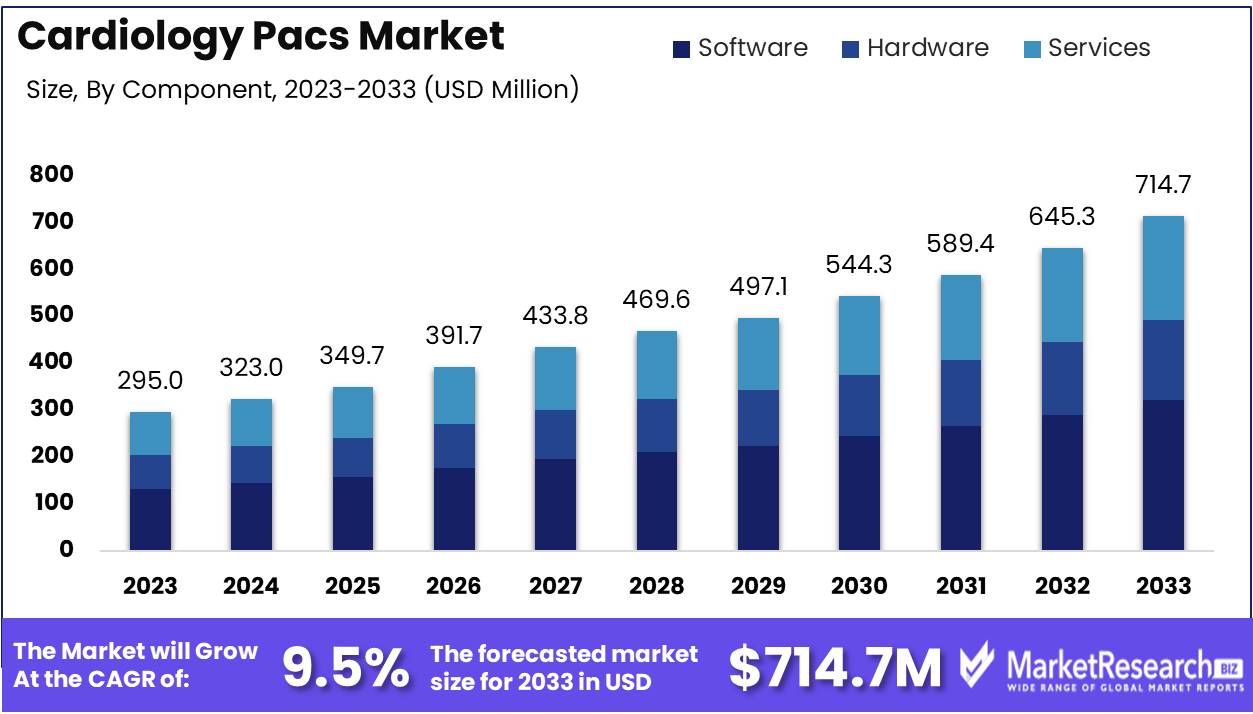

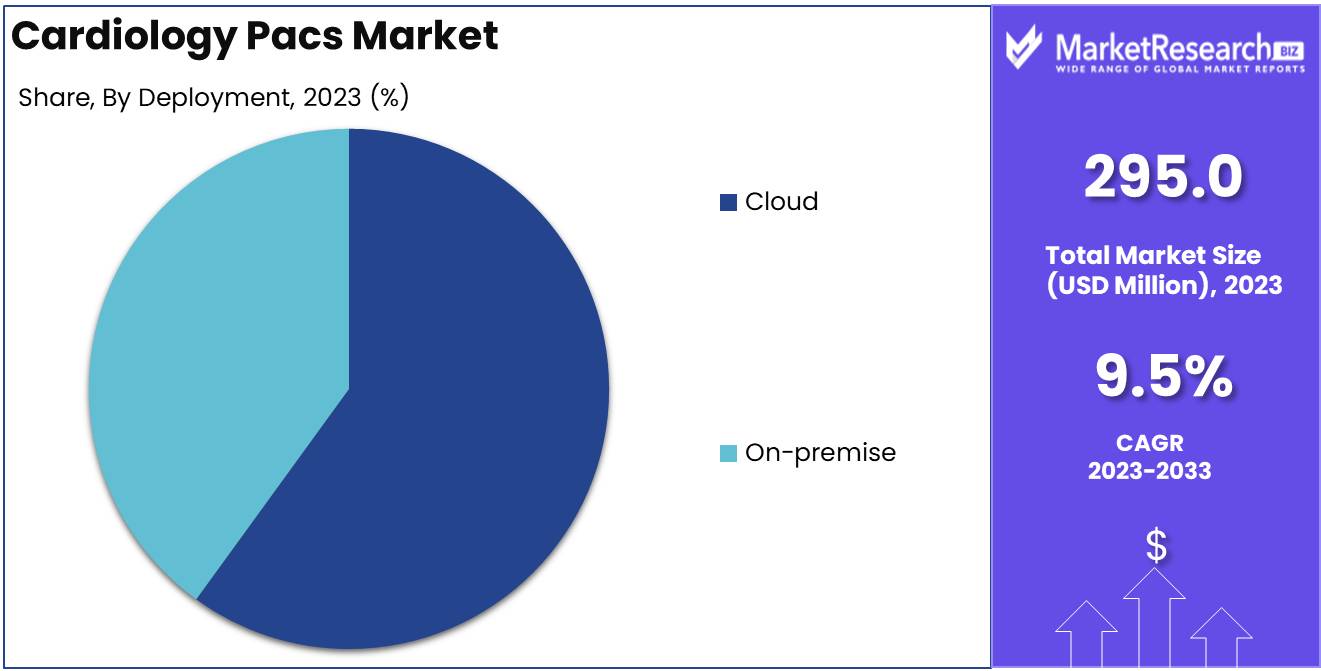

The Cardiology Pacs Market was valued at USD 295.0 million in 2023. It is expected to reach USD 714.7 million by 2033, with a CAGR of 9.5% during the forecast period from 2024 to 2033.

The Cardiology PACS (Picture Archiving and Communication System) Market refers to the specialized segment of healthcare technology that focuses on the storage, retrieval, management, and distribution of cardiac imaging data. These systems enable cardiologists to efficiently access and analyze a wide range of imaging modalities, including echocardiograms, MRIs, and CT scans, facilitating improved diagnostic test and treatment planning.

The global Cardiology PACS (Picture Archiving and Communication System) market is poised for significant growth, driven primarily by the increasing prevalence of cardiovascular diseases (CVDs) and the rapid advancements in medical imaging technologies. As the global burden of CVDs continues to rise, there is a growing demand for efficient and accurate diagnostic tools, making cardiology PACS an essential component in healthcare facilities. The integration of artificial intelligence (AI) into PACS systems is further enhancing diagnostic capabilities by enabling more precise analysis and interpretation of complex cardiac images. This technological advancement not only improves patient outcomes but also streamlines clinical workflows, reducing the burden on healthcare providers.

However, the market faces challenges, particularly around data security concerns, as the adoption of cloud-based PACS solutions grows. Ensuring the confidentiality and integrity of patient data is paramount, especially in an era where cyber threats are increasingly sophisticated. Market players must invest in robust security measures to safeguard sensitive information and maintain trust with healthcare providers. Moreover, the increasing reliance on AI and cloud technologies necessitates continuous updates and improvements to PACS systems, requiring ongoing investments in research and development. As the market evolves, companies that prioritize innovation and data security are likely to lead, capitalizing on the growing demand for advanced cardiology diagnostic tools in an increasingly digital healthcare environment.

Key Takeaways

- Market Growth: The Cardiology Pacs Market was valued at USD 295.0 million in 2023. It is expected to reach USD 714.7 million by 2033, with a CAGR of 9.5% during the forecast period from 2024 to 2033.

- By Component: Software dominated the Cardiology PACS Market's By Component segment.

- By Deployment: Cloud deployment dominated Cardiology PACS, with on-premise significant.

- By End-user: Hospitals & Clinics dominated the Cardiology PACS Market by end-user.

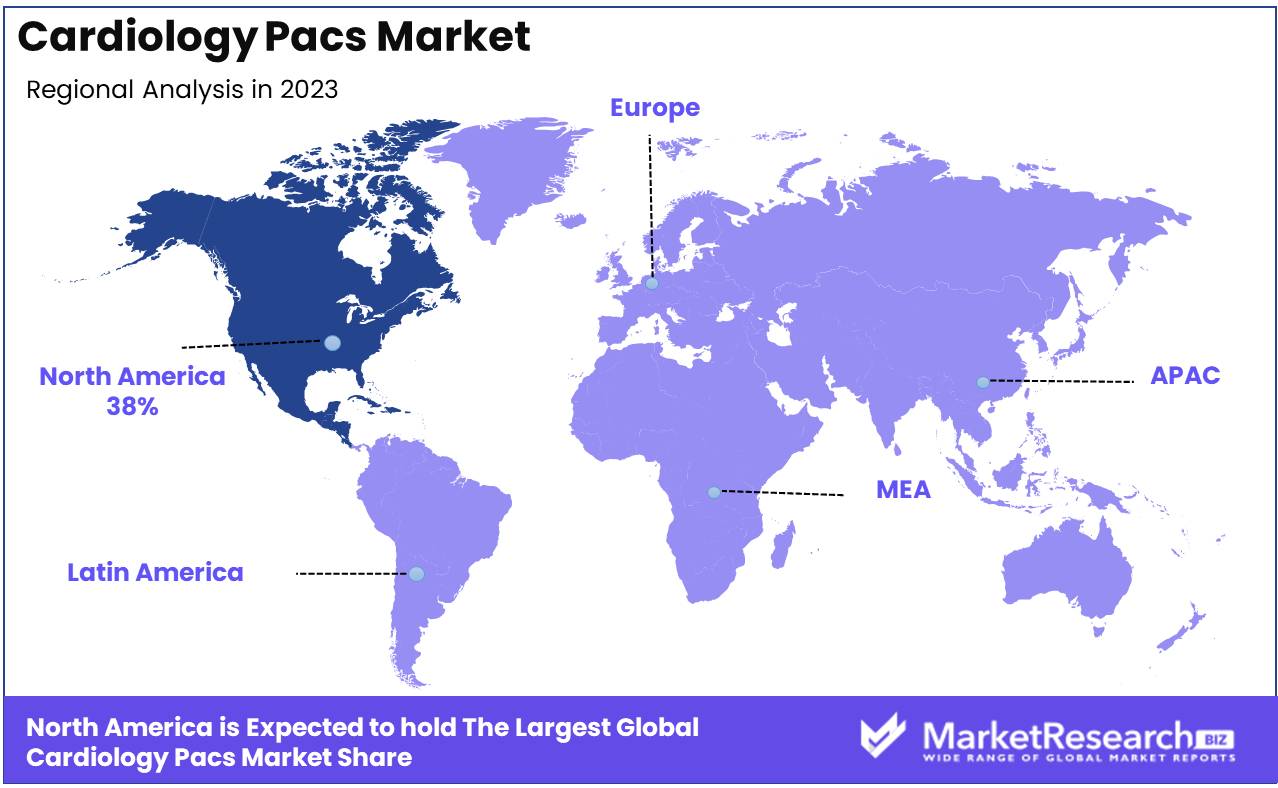

- Regional Dominance: North America dominates the global Cardiology PACS Market with a 38% largest share.

- Growth Opportunity: The Cardiology PACS market will grow significantly, driven by rising healthcare expenditure and strategic industry partnerships.

Driving factors

Rising Prevalence of Cardiovascular Diseases Fuels Demand for Cardiology PACS

The global burden of cardiovascular diseases (CVDs) has been increasing at an alarming rate, with conditions such as coronary artery disease, heart failure, and arrhythmias becoming more prevalent. According to the World Health Organization, CVDs are responsible for approximately 17.9 million deaths annually, accounting for 31% of global mortality. This rising prevalence drives the need for efficient diagnostic and treatment solutions, significantly boosting the demand for Cardiology Picture Archiving and Communication Systems (PACS). These systems offer streamlined storage, retrieval, and analysis of cardiology images, enabling healthcare providers to manage the growing number of cases effectively. As CVDs continue to rise, the Cardiology PACS market is expected to experience robust growth as healthcare facilities seek advanced technologies to manage patient data and improve diagnostic accuracy.

Integration of Artificial Intelligence Enhances the Capabilities of Cardiology PACS

Artificial Intelligence (AI) is revolutionizing the healthcare industry, particularly in the field of medical imaging. In cardiology, AI-powered PACS systems offer enhanced image analysis, automated measurements, and predictive analytics, which improve the accuracy and efficiency of diagnosing cardiovascular conditions. The integration of AI in Cardiology PACS enables the automation of routine tasks, such as image sorting and reporting, allowing cardiologists to focus on complex cases.

Moreover, AI algorithms can detect subtle patterns in imaging data that might be missed by the human eye, leading to earlier detection and intervention in CVDs. As healthcare providers increasingly recognize the value of AI in improving patient outcomes, the demand for AI-integrated Cardiology PACS is expected to surge, driving market growth.

Rising Number of Cardiology Procedures Increases Adoption of PACS Solutions

The number of cardiology procedures, including angiograms, echocardiograms, and catheterizations, has been steadily increasing due to the growing prevalence of cardiovascular diseases and the aging global population.A reports that over 48% of adults in the United States suffer from some form of cardiovascular disease, leading to a higher volume of diagnostic and interventional procedures. The increasing number of these procedures necessitates efficient and reliable systems for managing the associated imaging data.

Cardiology PACS solutions are critical in handling the large volumes of images generated during these procedures, ensuring quick access and analysis for timely decision-making. As the number of cardiology procedures continues to rise, so too will the adoption of PACS solutions, contributing significantly to market growth.

Restraining Factors

High Implementation and Maintenance Costs: A Barrier to Market Expansion

The high costs associated with the implementation and maintenance of Cardiology Picture Archiving and Communication Systems (PACS) serve as a significant restraint on the market's growth. These systems require substantial initial investment, including the costs of software, hardware, and specialized infrastructure.

Additionally, ongoing maintenance, upgrades, and training for healthcare professionals add to the financial burden on healthcare providers, particularly in smaller or underfunded institutions. This cost factor can lead to slower adoption rates, particularly in developing regions, thereby limiting the market's overall expansion. As a result, the high financial barrier is likely to constrain the widespread deployment of cardiology PACS, affecting the market's potential growth trajectory.

Data Security and Privacy Concerns: Limiting Market Adoption

Data security and privacy concerns represent another critical restraining factor for the Cardiology PACS Market. The sensitive nature of patient data managed within these systems necessitates stringent security measures, which can be both complex and costly to implement. The risk of data breaches, unauthorized access, and compliance with regulatory frameworks such as the Health Insurance Portability and

Accountability Act (HIPAA) in the U.S. or the General Data Protection Regulation (GDPR) in Europe, adds to the hesitancy of healthcare providers to fully adopt these systems. Fear of legal repercussions and potential damage to institutional reputation in case of data breaches can deter investment in PACS solutions, thus limiting market growth. The combined effect of these security and privacy concerns is a slower pace of adoption, particularly in regions with stringent regulatory environments.

By Component Analysis

In 2023, Software dominated the Cardiology PACS Market's By Component segment.

In 2023, Software held a dominant market position in the By Component segment of the Cardiology PACS Market. The widespread adoption of advanced imaging and diagnostic tools significantly contributed to the software's leadership in this segment. The software solutions offered enhanced capabilities for managing, analyzing, and storing cardiovascular imaging data, leading to improved clinical outcomes. Integration with other healthcare systems and the facilitation of real-time data sharing between clinicians also bolstered its prominence.

Hardware followed closely, driven by the demand for high-performance imaging devices and data storage systems. These hardware components are crucial for capturing and processing large volumes of cardiology-related data, ensuring precise diagnostics and efficient workflow in medical settings.

Services accounted for a smaller yet significant share of the market, reflecting the increasing need for maintenance, upgrades, and training associated with the use of software and hardware components. The service segment's growth is anticipated to continue as healthcare providers seek to optimize their PACS systems, ensuring they remain up-to-date with evolving technologies and regulatory requirements.

By Deployment Analysis

In 2023, Cloud deployment dominated Cardiology PACS, with on-premise significant.

In 2023, The Cloud deployment model held a dominant market position in the Cardiology PACS Market's "By Deployment" segment. The growing adoption of cloud-based solutions in healthcare is driven by the need for scalable, cost-effective, and easily accessible data storage and management systems. Cloud-based Cardiology PACS offers the advantage of remote access to patient data, facilitating better collaboration among healthcare professionals and improving patient care. Additionally, the lower upfront costs and reduced IT infrastructure requirements make cloud solutions attractive, particularly for small and medium-sized healthcare facilities. The flexibility and continuous software updates provided by cloud service providers further contribute to their increasing popularity.

Conversely, the On-premise deployment model remains a significant segment within the market. Despite the rise of cloud-based solutions, many large healthcare institutions prefer on-premise systems due to concerns over data security, compliance with regulatory standards, and control over IT infrastructure. On-premise Cardiology PACS allows for more customization and integration with existing hospital systems, appealing to institutions with specific needs and robust IT departments. As a result, while cloud deployment is gaining traction, on-premise systems continue to hold a substantial market share, particularly in regions with stringent data protection regulations.

By End-user Analysis

In 2023, Hospitals & Clinics dominated the Cardiology PACS Market by end-user.

In 2023, The Hospitals & Clinics segment held a dominant market position in the Cardiology PACS (Picture Archiving and Communication System) Market. This dominance can be attributed to the widespread adoption of advanced imaging technologies and the increasing number of cardiology procedures performed in hospitals. Hospitals and clinics are often the primary healthcare providers for cardiac patients, requiring efficient data management systems to handle large volumes of imaging data. The growing emphasis on improving patient outcomes, coupled with the need for seamless integration of PACS with electronic health records (EHRs), has further driven the demand in this segment. Additionally, the rising incidence of cardiovascular diseases globally has led to an increased demand for PACS in hospitals, where the majority of diagnostic and treatment procedures are conducted.

The Diagnostic Centres segment also plays a significant role, driven by the need for specialized imaging services. These centers often serve as referral hubs for complex cardiology cases, requiring high-quality imaging solutions to support accurate diagnoses.

Ambulatory Surgical Centres are gaining traction due to the shift towards outpatient procedures, while Catheterisation Laboratories remain critical for interventional cardiology.

Other segments, including academic institutions and research organizations, continue to contribute to market growth through innovation and the adoption of cutting-edge PACS technologies.

Key Market Segments

By Component

- Software

- Hardware

- Services

By Deployment

- Cloud

- On-premise

By End-user

- Hospitals & Clinics

- Diagnostic Centres

- Ambulatory Surgical Centres

- Catheterisation Laboratories

- Others

Growth Opportunity

Rising Healthcare Expenditure Fuels Growth

The global Cardiology Picture Archiving and Communication System (PACS) market is poised for significant growth, driven primarily by increasing healthcare expenditure worldwide. Governments and private sectors are investing heavily in advanced healthcare infrastructure to improve patient outcomes, with a substantial portion of these investments directed toward digital health technologies.

Cardiology PACS, being a critical component of modern cardiology departments, stands to benefit immensely from this trend. The integration of PACS with other healthcare systems enhances the efficiency of diagnosing and treating cardiovascular diseases, further solidifying its adoption in both developed and developing regions.

Strategic Partnerships and Collaborations Boost Market Expansion

Strategic partnerships and collaborations are emerging as pivotal opportunities for the expansion of the Cardiology PACS market. Leading companies are increasingly entering into alliances with healthcare providers, technology firms, and research institutions to innovate and deliver cutting-edge PACS solutions. These collaborations not only foster technological advancements but also enable market players to expand their global footprint. By leveraging shared expertise and resources, these partnerships accelerate the development of more sophisticated and interoperable PACS systems, catering to the growing demand for integrated healthcare solutions.

Latest Trends

Increasing Adoption of Cloud-based Cardiology PACS

The Cardiology PACS market is expected to witness a significant shift toward cloud-based solutions. This transition is driven by the growing need for scalable, cost-effective, and accessible data management systems. Cloud-based PACS offers several advantages, including remote access to patient data, enhanced collaboration between healthcare providers, and reduced infrastructure costs. This trend is particularly beneficial for small and medium-sized healthcare facilities that may lack the resources to maintain on-premises systems. As cybersecurity concerns are addressed with advanced encryption and compliance measures, the adoption of cloud-based PACS is anticipated to accelerate, contributing to market growth.

Emphasis on Early Disease Detection

Early detection of cardiovascular diseases is becoming a central focus in healthcare, significantly impacting the Cardiology PACS market. Advanced imaging technologies and AI-driven analytics are increasingly integrated into PACS systems to enhance diagnostic accuracy and facilitate early intervention. This trend is fueled by the rising prevalence of cardiovascular diseases globally, coupled with the demand for improved patient outcomes. As healthcare providers prioritize early diagnosis, the need for robust and efficient PACS systems that can seamlessly integrate with other diagnostic tools is expected to grow. This emphasis on early disease detection is likely to drive innovation and expansion within the market, positioning it for sustained growth and beyond.

Regional Analysis

North America dominates the global Cardiology PACS Market with a 38% largest share.

The Cardiology PACS Market demonstrates significant growth across various regions, with North America emerging as the dominant player, holding approximately 38% of the global market share. This region's leadership is attributed to advanced healthcare infrastructure, high adoption rates of digital healthcare solutions, and strong investments in medical technology. The United States, in particular, drives this growth due to its well-established healthcare system and a significant number of cardiology procedures performed annually.

In Europe, the market also exhibits robust growth, driven by increasing awareness of cardiovascular diseases and the implementation of sophisticated healthcare IT systems. The European market accounts for around 30% of the global share, with countries like Germany, the UK, and France being key contributors.

The Asia Pacific region is experiencing rapid expansion, with a focus on improving healthcare access and infrastructure in emerging economies such as China and India. This region is expected to witness the highest growth rate, with a current market share of approximately 22%, driven by rising healthcare expenditures and government initiatives.

The Middle East & Africa and Latin America, while smaller in market share, are showing steady growth due to increased investments in healthcare and growing demand for digital health solutions, contributing to the global expansion of the Cardiology PACS Market.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

In 2024, the global Cardiology PACS (Picture Archiving and Communication System) market is witnessing significant advancements driven by key players such as GE Healthcare, Fujifilm Medical Systems, Central Data Networks, AGFA Healthcare, Philips Healthcare, Medstreaming, Siemens Healthcare, Digisonics, NFINITT Healthcare, Sectra, and IBM Corporation. These companies are leading the market with innovative solutions that enhance cardiology imaging, data management, and workflow efficiency.

GE Healthcare continues to be a dominant force with its robust portfolio of cardiology PACS solutions, focusing on integrating AI to enhance diagnostic accuracy and streamline clinical workflows. Fujifilm Medical Systems and AGFA Healthcare are also making strides by offering cloud-based PACS platforms that provide scalable and secure access to cardiology images, improving collaboration among healthcare providers.

Philips Healthcare and Siemens Healthcare are leveraging their extensive experience in healthcare technology to offer comprehensive cardiology PACS systems that are seamlessly integrated with other healthcare IT systems, enabling better patient care coordination. Medstreaming and Digisonics are gaining traction with specialized cardiology PACS offerings that cater to niche markets, providing tailored solutions that meet the unique needs of smaller cardiology practices.

Meanwhile, IBM Corporation is utilizing its expertise in AI and data analytics to revolutionize the cardiology PACS landscape, offering solutions that enhance image interpretation and predictive analytics. NFINITT Healthcare and Sectra are focusing on expanding their market presence through strategic partnerships and technological innovations, ensuring their solutions remain competitive in an increasingly complex healthcare environment.

Overall, these key players are driving the growth of the cardiology PACS market by continuously evolving their offerings to meet the ever-changing demands of the healthcare industry, ensuring improved patient outcomes and operational efficiency.

Market Key Players

- GE Healthcare

- Fujifilm Medical Systems

- Central Data Networks

- AGFA Healthcare

- Philips Healthcare

- Medstreaming

- Siemens Healthcare

- Digisonics

- NFINITT Healthcare

- Sectra

- IBM Corporation

Recent Development

- In August 2024, GE HealthCare showcased its latest AI-enhanced cardiology solutions at the European Society of Cardiology (ESC) Congress 2024, held in London from August 30 to September 2. These innovations are designed to enable real-time cardiac imaging and assessments at the point of care, emphasizing the integration of AI for improving diagnostic accuracy and patient outcomes.

- In June 2024, Siemens Healthineers announced a collaboration with IBM Watson Health to integrate advanced AI algorithms into their cardiology PACS solutions. This partnership aims to enhance image analysis capabilities, streamline workflows, and provide more accurate diagnostics, particularly in cardiovascular care.

- In May 2024, Agfa HealthCare launched a new cloud-based cardiology PACS solution, designed to offer scalable, secure, and cost-effective storage and retrieval of cardiac images. This solution facilitates remote access for healthcare professionals, thereby improving collaboration and decision-making processes in cardiac care.

Report Scope

Report Features Description Market Value (2023) USD 295.0 Million Forecast Revenue (2033) USD 714.7 Million CAGR (2024-2032) 9.5% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Component (Software, Hardware, Services), By Deployment (Cloud, On-premise), By End-user (Hospitals & Clinics, Diagnostic Centres, Ambulatory Surgical Centres, Catheterisation Laboratories, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape GE Healthcare, Fujifilm Medical Systems, Central Data Networks, AGFA Healthcare, Philips Healthcare, Medstreaming, Siemens Healthcare, Digisonics, NFINITT Healthcare, Sectra and IBM Corporation Customization Scope Customization for segments at the regional/country level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- GE Healthcare

- Fujifilm Medical Systems

- Central Data Networks

- AGFA Healthcare

- Philips Healthcare

- Medstreaming

- Siemens Healthcare

- Digisonics

- NFINITT Healthcare

- Sectra

- IBM Corporation

Our Clients

View Our Licence Options