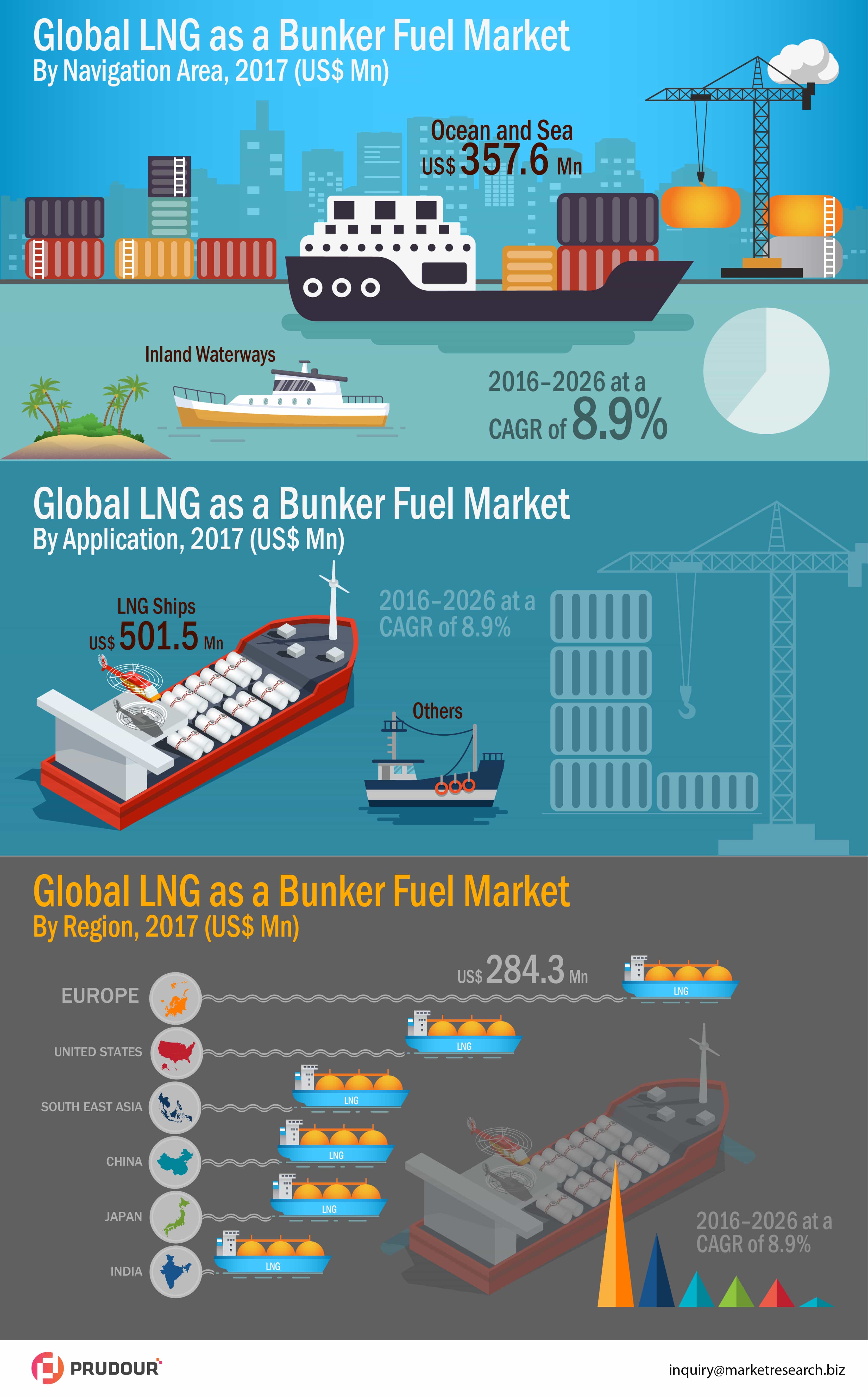

Among navigation segments, ocean and sea segment in the global LNG as a bunker fuel market is estimated to account for a majority revenue share of US$ 357.6 Mn in 2017. The first five-year cumulative revenue (2017–2021) is estimated to be US$ 1,965.6 Mn, as compared to a significantly higher cumulative revenue total of US$ 3,034.4 Mn for the latter five years of the forecast period (2022–2026).

Among the application segments, LNG ship segment is expected to account for US$ 501.5 Mn in 2017. Liquefied Natural Gas (LNG) is a clear, colourless, non-toxic and non-corrosive liquid, which is converted to liquid by cooling of natural gas at a cryogenic temperature of -162°C. It has a come up as a potential solution for meeting International Maritime Organization’s (IMO) emission norm requirements, since it has virtually no sulfur content and its combustion produces low NOx compared to fuel oil and marine diesel oil.

IMO’s latest mandate states that from 2020, ships will have to use marine fuels with a sulphur content of no more than 0.5% against the current limit of 3.5% in an effort to reduce greenhouse gas emissions. It is proven that use of LNG as ship fuel will reduce sulphur oxide (SOx ) emissions by 90% – 95%. Lower carbon content of LNG compared to conventional ship fuels enables a 20–25% reduction of carbon dioxide (CO2) emissions, which is a major driving factor. LNG is also expected to be less costly than marine gas oil (MGO), which will be required to be used within the ECAs if no other technical measures are implemented to reduce the SOx emissions. This is another key factor expected to further fuel growth of LNG as bunker fuel market globally.

Although, LNG fuel in itself may be inexpensive, but cost and time needed to retrofit or new-build a ship with a dedicated LNG propulsion system are relatively high. By comparison, SOx scrubbers require a smaller initial investment and take less time to install. LNG barrels also require more space for storage tanks and as much as 3% of a container ship’s twenty-foot equivalent unit (TEU) slots, thereby directly impacting profitability. These factors are expected to restrain growth of LNG as bunker fuel market.

Nonetheless, countries are making a strategic shift to a less carbon-intensive future owing to various regulation and mandates to reduce carbon footprint and damage to the environment. LNG bunkering infrastructure is developing globally, with China and Europe currently in the forefront for developing respective LNG bunkering facilities, with a number of projects underway, which is expected to provide lucrative opportunities for LNG producers and suppliers in the coming years. Europe market is estimated to account for US$ 284.3 Mn in 2017.

Key Players in this report are Royal Dutch Shell Plc, Gasum Oy, Statoil ASA, Barents Natural Gas AS, The Linde Group, ENGIE SA, Korea Gas Corporation, Kunlun Energy Company Ltd., Eni s.p.A, CNOOC Limited, Energize.