Global Plastisols Market By Resin Type(Polyvinyl Chloride (PVC) Resin, Acrylic Resin), By Application(Paints and Coatings, Adhesives and Sealants, Printing Inks, Moldings, Others), By End Use Industry(Textiles, Building and Construction, Transportation, Appliances and Machines, Others), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

44473

-

April 2024

-

300

-

-

This report was compiled by Shreyas Rokade Shreyas Rokade is a seasoned Research Analyst with CMFE, bringing extensive expertise in market research and consulting, with a strong background in Chemical Engineering. Correspondence Team Lead-CMFE Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Report Overview

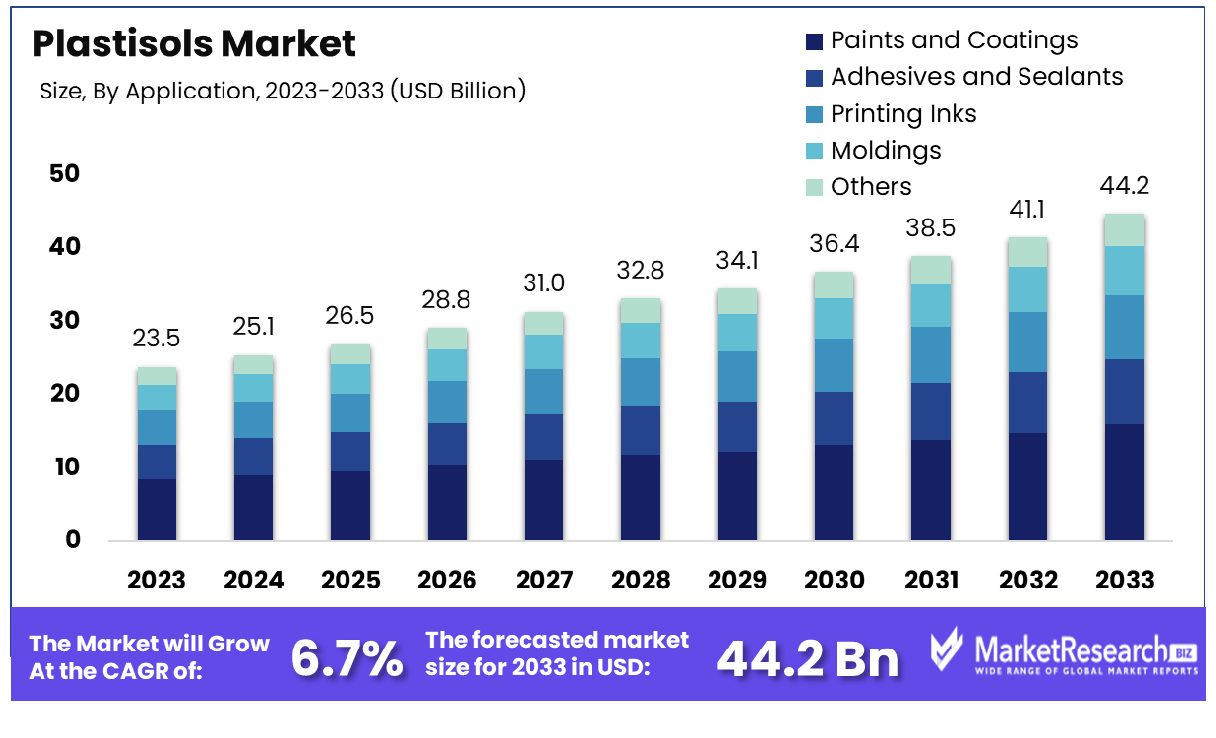

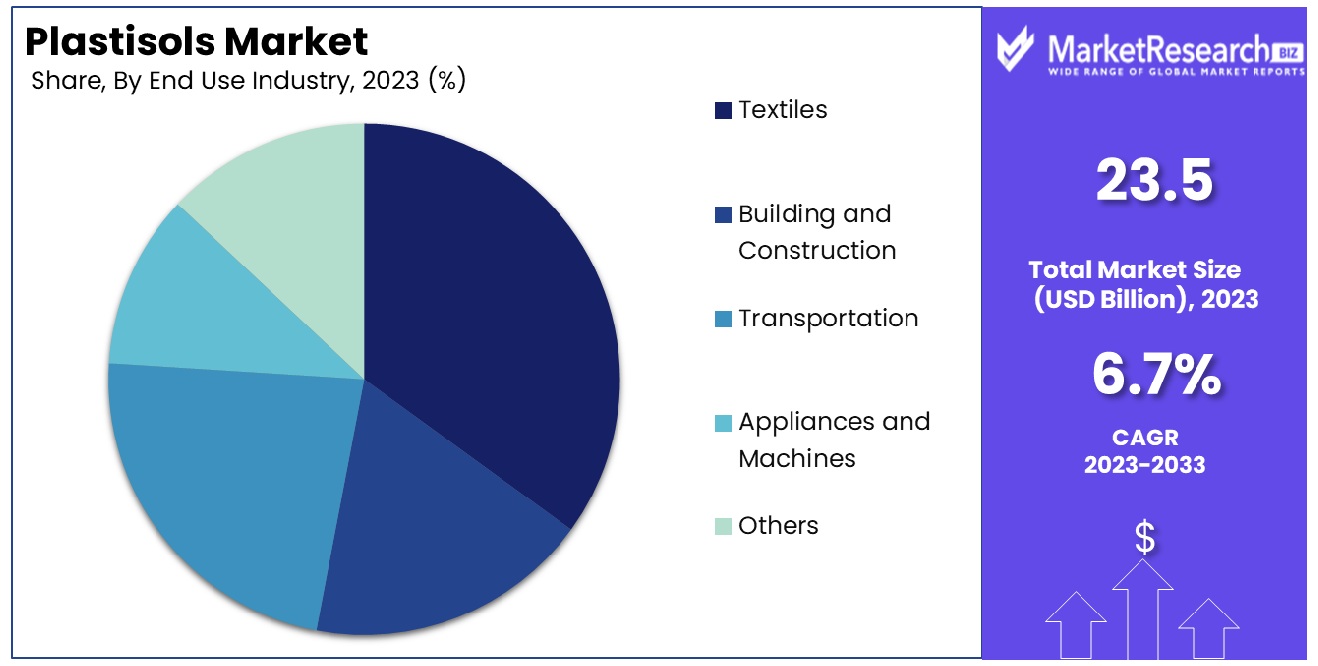

The Global Plastisols Market was valued at USD 23.5 billion in 2023. It is expected to reach USD 44.2 billion by 2033, with a CAGR of 6.7% during the forecast period from 2024 to 2033.

The Plastisols Market encompasses a specialized sector dedicated to the production and application of plastisol compounds, a type of suspension of PVC particles in plasticizers, which transforms into a flexible, durable material upon heating. This market caters to diverse industries, including automotive, textile, and consumer goods, offering solutions for coatings, sealants, and inks.

Plastisols are esteemed for their versatility, longevity, and performance under various conditions, addressing the intricate demands of high-stakes manufacturing processes. Executives and product managers leverage insights from this market to innovate in product development, enhance operational efficiencies, and navigate environmental regulations, aiming to sustain competitive advantage and drive market growth.

The Plastisols Market has witnessed a dynamic evolution, driven by diverse applications ranging from automotive coatings to textile screen printing. This versatility underscores the demand for Plastisols, which is further accentuated by their unique properties such as durability, flexibility, and resistance to weathering. However, the market's expansion is juxtaposed against an increasingly stringent regulatory landscape, aimed at mitigating environmental impacts associated with plastic use.

The adaptation to eco-friendly alternatives and innovations in recycling processes stand as pivotal major factors that could shape the future trajectory of the Plastisols Market. Stakeholders are now navigating this complex landscape, balancing operational efficiency with sustainable practices. The industry's growth is contingent upon leveraging technological advancements to enhance product formulations, thereby meeting the evolving demands of end-use sectors while adhering to environmental standards.

Incorporating the environmental context presents a nuanced understanding of the challenges faced by the Plastisols Market. According to Condor Ferries, the burgeoning issue of plastic pollution has been underscored by the staggering estimate of 75 to 199 million tons of plastic waste in the oceans, coupled with an annual influx of 33 billion pounds into the marine environment. The historical trajectory of plastic production, which surged to 460 million metric tons in 2019, highlights the escalating scale of plastic usage and its consequent environmental ramifications.

This backdrop of environmental concerns necessitates a strategic pivot within the Plastisols Market towards sustainability, underscored by innovation in product development and waste management strategies. The market's response to these challenges will be instrumental in determining its sustainability and resilience, positioning environmental stewardship as a cornerstone of future growth strategies.

Key Takeaways

- Market Growth: The Global Plastisols Market was valued at USD 23.5 billion in 2023. It is expected to reach USD 44.2 billion by 2033, with a CAGR of 6.7% during the forecast period from 2024 to 2033.

- By Resin Type: Polyvinyl Chloride (PVC) Resin emerged as the leading segment, dominating the market.

- By Application: In terms of application, the paints and coatings sector held the predominant position.

- By End-Use Industry: Within the end-use industry landscape, textiles were identified as the principal domain.

- Regional Dominance: In Asia-Pacific, the plastisols market commands a significant 44% share of the global market.

- Growth Opportunity: In 2023, the Plastisols Market is poised for growth through the integration with smart textiles and wearable technologies, and penetration into renewable energy sectors, particularly for solar panel coatings, aligning with trends towards sustainability and technological innovation.

Driving factors

Environmental Regulations and Sustainability Initiatives

The growth of the Plastisols Market can be significantly attributed to stringent environmental regulations and the escalating emphasis on sustainability initiatives. As governments and environmental bodies impose tighter controls on the emission of volatile organic compounds (VOCs) and hazardous air pollutants (HAPs), industries are compelled to adopt eco-friendly materials.

Plastisols, known for their low VOC content, emerge as a viable alternative, thus driving their increased adoption across various sectors. Furthermore, the shift towards sustainability bolsters the demand for plastisols in applications that require durable and recyclable materials. This transition not only supports environmental goals but also aligns with consumer preferences for sustainable products, further propelling the market growth.

Expansion in Construction and Architecture

The expansion in construction and architecture significantly fuels the demand for plastisols, particularly through the increased adoption of coil coatings. Plastisols serve as an essential component in the production of coil coatings due to their durability, corrosion resistance, and aesthetic versatility. As the construction and architecture sectors thrive, especially in emerging economies, the need for high-quality, resilient building materials escalates.

This uptrend directly translates to a heightened demand for plastisols in coil coatings, contributing substantially to the market's expansion. Moreover, the versatility of plastisols in color and texture customization meets the evolving architectural trends and consumer demands, further enhancing their market appeal.

Increasing Demand from the Building and Construction Industry

The building and construction industry's burgeoning demand for coil coatings directly impacts the Plastisols Market's growth trajectory. This surge is rooted in the industry's need for materials that offer extended lifespan, aesthetic appeal, and resistance to environmental growth factors. Coil coatings, enhanced with plastisols, fulfill these requirements, making them indispensable in construction projects.

As urbanization accelerates and infrastructural developments proliferate, the demand for these coatings escalates, in turn, driving the plastisols market forward. This growing demand is underpinned by the industry's pursuit of efficiency and durability, with plastisols-based coil coatings providing an effective solution to these needs.

Restraining Factors

Toxic Nature of PVC and Phthalates

The Plastisols Market faces significant challenges due to the toxic nature of polyvinyl chloride (PVC) and phthalates, which are often integral components of plastisol formulations. The health and environmental risks associated with the release of these substances during production and end-of-life disposal have led to stringent regulations and a shift in consumer preferences towards safer, more sustainable alternatives.

The presence of phthalates, known for their potential endocrine-disrupting properties, has particularly heightened concerns, prompting regulatory bodies worldwide to enforce stricter controls on their use. This regulatory environment, coupled with growing health consciousness among consumers, restrains the plastisols market growth by limiting its applicability in sensitive applications such as toys, food packaging, and medical devices. Consequently, manufacturers are compelled to explore and invest in non-toxic alternatives or phthalate-free formulations, which may incur additional costs and impact market competitiveness.

High Cure Temperatures of Plastisols

Another constraining factor for the Plastisols Market is the requirement for high cure temperatures. Plastisols necessitate elevated temperatures (typically around 160 to 200°C) to achieve the desired state of fusion and cure, which can pose significant energy consumption and efficiency challenges for manufacturers. This high thermal requirement not only increases production costs but also limits the material's compatibility with heat-sensitive substrates, thereby narrowing the scope of its applications.

In sectors where energy efficiency and low processing temperatures are prioritized, the demand for plastisols may be adversely affected, further restraining market growth. Additionally, the energy-intensive curing process contradicts the increasing industry and consumer push towards more environmentally friendly manufacturing practices, posing a contradiction to sustainability goals.

By Resin Type Analysis

In the resin type category, Polyvinyl Chloride (PVC) Resin emerged as the dominant material, leading the market significantly.

In 2023, Polyvinyl Chloride (PVC) Resin held a dominant market position in the "By Resin Type" segment of the Plastisols Market, alongside other notable resin types such as Acrylic Resin. The preeminence of PVC Resin in this market segment can be attributed to its superior characteristics, including robustness, versatility, and cost-effectiveness, which have fostered its wide adoption across various applications. The utilization of PVC Resin in the manufacturing of plastisols has been particularly pronounced in sectors such as automotive, textile, and construction, where its application in coatings, sealants, and adhesives is prevalent.

The durability and chemical resistance of PVC Resin contributes significantly to the longevity and performance of plastisols, making it a preferred choice over other resin types. Furthermore, advancements in plasticizer technology have enhanced the flexibility and workability of PVC-based plastisols, expanding their application range and reinforcing PVC Resin's market dominance.

However, Acrylic Resin has also carved out a significant niche within the Plastisols Market, attributed to its exceptional clarity, resistance to ultraviolet light, and aesthetic versatility. This resin type has found its footing in applications demanding a higher degree of transparency and color retention, thereby complementing the market presence of PVC Resin.

The competitive landscape of the "By Resin Type" segment in the Plastisols Market is characterized by ongoing research and development efforts aimed at improving the properties of both PVC and Acrylic Resins.

These endeavors are directed towards enhancing the environmental sustainability of plastisols, reducing volatile organic compound (VOC) emissions, and improving recyclability, which are critical considerations in the current market climate. The strategic focus on innovation and sustainability underscores the growth potential and evolving dynamics of the Plastisols Market, with PVC and Acrylic resin playing pivotal roles in shaping its trajectory.

By Application Analysis

Within the application segment, Paints and Coatings were the foremost choices, showcasing their widespread use across various industries.

In 2023, Paints and Coatings held a dominant market position in the "By Application" segment of the Plastisols Market, standing alongside other key application segments such as Adhesives and Sealants, Printing Inks, Moldings, and Others. This dominance is primarily attributed to the widespread adoption of plastisol-based paints and coatings across various industries, including automotive, construction, and consumer goods, where their durability, versatility, and aesthetic appeal are highly valued.

The robust demand for plastisol paints and coatings can be linked to their exceptional performance characteristics, such as resistance to corrosion, weatherability, and flexibility, which are critical for applications subjected to harsh environmental conditions. Moreover, the customization possibilities offered by plastisol coatings, in terms of colors and finishes, further solidify their preference in the market.

While Paints and Coatings command a significant share, the segments of adhesive sealants, and Printing Inks also exhibit substantial market penetration. Plastisol-based adhesives and sealants are renowned for their strong bonding capabilities and flexibility, making them indispensable in automotive and construction applications. Similarly, plastisol inks have revolutionized the textile printing industry due to their vibrant colors, durability, and stretchability, catering to the evolving demands of the fashion and apparel industry sectors.

The Moldings segment, too, showcases a notable presence, driven by the need for durable, precision-molded components in consumer electronics, healthcare, and automotive industries. The "Others" category encompasses emerging applications, reflecting the innovative use of plastisols in novel market niches.

By End Use Industry Analysis

Regarding end use, the textile sector stood out prominently, underscoring its significant consumption and application of the product.

In 2023, Textiles held a dominant market position in the "By End Use Industry" segment of the Plastisols Market, accompanied by other significant industries such as Building and Construction, Transportation, Appliances and Machines, and Others. The prominence of the Textile industry within this market can be largely ascribed to the extensive utilization of plastisols in fabric coatings, printing applications, and the manufacturing of non-woven textiles. These applications are driven by the demand for durable, flexible, and aesthetically appealing textile products, which plastisols facilitate through their unique properties.

Plastisols have become indispensable in the textile industry due to their ability to produce vibrant, durable prints that withstand multiple washes without fading. Additionally, the flexibility and water resistance offered by plastisol coatings makes them ideal for outdoor and protective textiles, further expanding their utility within the industry.

Concurrently, the Building and Construction industry represents a significant segment, where plastisols are employed in roofing materials, sealants, and coatings, contributing to their demand due to the materials' durability and resistance to environmental stressors. The Transportation sector also leverages plastisols in automotive coatings, underbody sealants, and interior finishes, valuing the material's durability and aesthetic versatility.

Moreover, in the Appliances and Machines industry, plastisols are utilized for their insulating properties and resistance to chemicals and electricity, making them suitable for coatings and components in various appliances. The "Others" category encompasses emerging industries and innovative applications, showcasing the adaptability and broad potential of plastisols across diverse end-use sectors.

Key Market Segments

By Resin Type

- Polyvinyl Chloride (PVC) Resin

- Acrylic Resin

By Application

- Paints and Coatings

- Adhesives and Sealants

- Printing Inks

- Moldings

- Others

By End Use Industry

- Textiles

- Building and Construction

- Transportation

- Appliances and Machines

- Others

Growth Opportunity

Integration with Smart Textiles and Wearable Technologies

The year 2023 marks a pivotal juncture for the global plastisol market growth, with the integration of smart textiles and wearable technologies presenting a significant opportunity. The inherent flexibility, durability, and water-resistant properties of plastisols make them an ideal candidate for embedding sensors and electronic components into textiles. This integration is poised to revolutionize the wearable technology industry by enabling the development of more comfortable, functional, and durable smart garments and accessories.

As consumer demand for health monitoring, fitness tracking, and seamless connectivity continues to rise, the use of plastisols in smart textiles and wearables offers a promising avenue for market expansion. The challenge lies in advancing the material's compatibility with electronic elements and enhancing its sustainability, yet the potential for innovation in this space remains vast.

Penetration into Renewable Energy Sectors, Especially in Solar Panel Coatings

Another notable opportunity in 2023 for the market for plastisol is its penetration into the renewable energy sectors, particularly through applications in solar panel coatings. The unique attributes of plastisols, including UV resistance and the ability to form seamless, protective layers, render them ideal for enhancing the durability and efficiency of solar panels. As the global push towards sustainable energy solutions intensifies, the demand for high-quality, long-lasting solar panels is expected to surge.

Plastisols could play a crucial role in meeting this demand by providing coatings that protect against environmental wear and tear while maintaining the panels' performance over time. This foray into the renewable energy sector not only diversifies the applications of plastisols but also aligns with the broader industry trends toward sustainability and environmental responsibility.

Latest Trends

Adoption in Consumer Goods for Enhanced Durability and Aesthetic Appeal

In 2023, the global Plastisols Market has observed a significant trend toward the adoption of plastisols in consumer goods, underscored by their enhanced durability and aesthetic appeal. This trend is driven by the material's versatility, allowing for the creation of products that are not only robust and long-lasting but also visually attractive. Plastisols offer a unique combination of properties such as flexibility, chemical resistance, and the ability to adhere to a wide range of substrates, making them ideal for various consumer goods including toys, household items, and sports equipment.

The customization potential of plastisols in terms of colors and finishes has further fueled their popularity in this sector. As consumer expectations for high-quality, durable products continue to rise, the utilization of plastisols is expected to expand, marking a vital growth avenue for the market.

Exploration of New Applications in 3D Printing Materials

Another burgeoning trend in the Plastisols Market is the exploration of its applications in 3D printing materials. The unique characteristics of plastisols, such as their viscosity and ability to be cured into a solid form, make them an intriguing option for 3D printing, offering new possibilities in terms of flexibility, durability, and detail in printed objects. This exploration is particularly relevant as the demand for more versatile 3D printing materials grows, spanning industries from healthcare to automotive.

The potential of plastisols in this innovative field could revolutionize 3D printing by providing materials that combine the ease of printing with enhanced performance characteristics. As research and development in this area advance, plastisols are poised to open new frontiers in manufacturing and design, further diversifying their applications and solidifying their position in the global market.

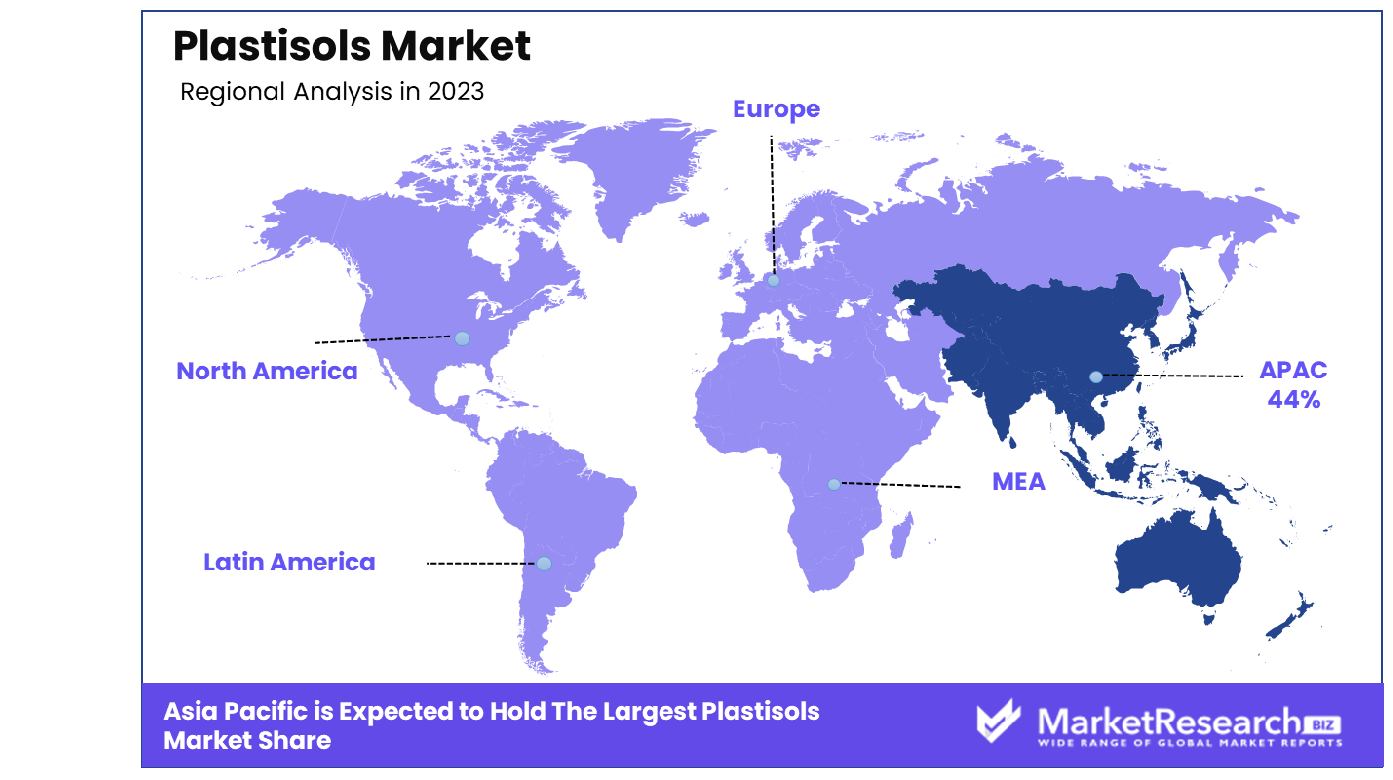

Regional Analysis

In 2023, Asia-Pacific dominated the Plastisols Market, accounting for 44% of the global share.

The global Plastisols Market exhibits substantial diversity across various regions, including North America, Europe, Asia-Pacific, the Middle East & Africa, and Latin America, each contributing uniquely to the market dynamics. Among these, Asia-Pacific emerges as the dominating region, holding a significant 44% share of the market. This dominance can be attributed to the region's expansive manufacturing base, rapid industrialization, and the growing demand in automotive, textile, and construction industries, particularly in countries like China, India, and Japan.

North America, with its advanced technological landscape and stringent environmental regulations, has been focusing on the development of eco-friendly and non-phthalate plastisol formulations, catering to the demand in the automotive and healthcare sectors. Europe follows a similar trajectory, with a strong emphasis on sustainability and innovation, driving the adoption of plastisols in renewable energy sectors, especially in solar panel coatings.

The Middle East & Africa region, although holding a smaller share, is witnessing growth in the construction and automotive sectors, which in turn fuels the demand for plastisols. The increasing infrastructural development projects in countries such as the UAE and Saudi Arabia are pivotal to this growth. Latin America, on the other hand, shows potential for market expansion through the textile and consumer goods sectors, with countries like Brazil and Mexico leading the way.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of Middle East & Africa

Key Players Analysis

In the analysis of the global Plastisols market for 2023, attention is drawn towards the performance and strategic positioning of key players, including Avient Corporation, Campbell Plastics Limited, Carlisle Plastics Company Inc., Chemionics Corporation (Chessco Industries), FUJIFILM Holdings Corporation, International Coatings, Lancer Group International, Monarch Color Corporation, Patcham FZC, PolyBlend UK Ltd, and PolySol LLC. These entities have demonstrated noteworthy contributions to market dynamics, driven by innovative product offerings, strategic expansions, and a focus on sustainability and regulatory compliance.

Avient Corporation is observed to maintain its leadership through extensive R&D investments, yielding advanced plastisol formulations catering to diverse industry requirements. The company's commitment to sustainability is evidenced by the development of eco-friendly plastisol solutions, align with global environmental standards.

Campbell Plastics Limited and Carlisle Plastics Company Inc., on the other hand, have carved niches in specialized applications of plastisols, enhancing their market presence. Their bespoke solutions for automotive and industrial applications underscore their capability to meet specific client needs, thus fostering loyalty and expanding their market footprint.

The strategic focus of Chemionics Corporation and FUJIFILM Holdings Corporation on integrating digital technologies into plastisol production processes has enhanced operational efficiencies and product quality. This technological adoption positions them favorably for future growth opportunities.

Emerging major players like PolyBlend UK Ltd and PolySol LLC have shown significant agility in responding to market trends, particularly in custom formulations, thereby enhancing their competitiveness in the market.

Collectively, these key players' strategies are geared toward innovation, customer-centric solutions, and environmental stewardship. Their actions are indicative of a mature yet evolving market landscape, where differentiation and sustainability are paramount for long-term success. The continued investment in technology, alongside a keen focus on regulatory compliance, positions these major companies well for capitalizing on the global plastisols market opportunities in 2023 and beyond.

Market Key Players

- Avient Corporation

- Campbell Plastics Limited

- Carlisle Plastics Company Inc.

- Chemionics Corporation (Chessco Industries)

- FUJIFILM Holdings Corporation

- International Coatings

- Lancer Group International

- Monarch Color Corporation

- Patcham FZC

- PolyBlend UK Ltd

- PolySol LLC

Recent Development

- In January 2024, Avient Corporation unveiled eco-friendly solutions at Impressions Expo Long Beach, including Union Ink UPLC Unimix for a flexible cure, Wilflex Revive inks with 50-59% bio-derived content, and Rutland Chill LB LC Poly Mixing Base.

- In January 2019, Progressive Coating in Chicago, led by Stephen Walters, experienced a remarkable 650% growth since 2006. Offering diverse coatings like fluidized bed powder and vinyl plastisol, the company achieved industry recognition and ISO certifications.

Report Scope

Report Features Description Market Value (2023) USD 23.5 Billion Forecast Revenue (2033) USD 44.2 Billion CAGR (2024-2032) 6.7% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Resin Type(Polyvinyl Chloride (PVC) Resin, Acrylic Resin), By Application(Paints and Coatings, Adhesives and Sealants, Printing Inks, Moldings, Others), By End Use Industry(Textiles, Building and Construction, Transportation, Appliances and Machines, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Avient Corporation, Campbell Plastics Limited, Carlisle Plastics Company Inc., Chemionics Corporation (Chessco Industries), FUJIFILM Holdings Corporation, International Coatings, Lancer Group International, Monarch Color Corporation, Patcham FZC, PolyBlend UK Ltd, PolySol LLC Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Avient Corporation

- Campbell Plastics Limited

- Carlisle Plastics Company Inc.

- Chemionics Corporation (Chessco Industries)

- FUJIFILM Holdings Corporation

- International Coatings

- Lancer Group International

- Monarch Color Corporation

- Patcham FZC

- PolyBlend UK Ltd

- PolySol LLC

Our Clients

View Our Licence Options