Companion Diagnostics Market By Product(Assays, Kits, and Reagents, Software and Services), By Technology(Polymerase Chain Reaction, Immunohistochemistry, Others), By Indication(Cancer, Neurological Disorders, Other), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2023-2032

-

41423

-

Sep 2023

-

160

-

-

This report was compiled by Correspondence Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Report Overview

Companion Diagnostics Market size is expected to be worth around USD XX by 2032 from USD XX in 2022, growing at a CAGR of XX% during the forecast period from 2023 to 2032.

Companion diagnostics, often referred to as CDx, play a crucial role in personalized medicine by matching specific treatments to patients based on their genetic makeup and individual characteristics. By utilizing cutting-edge technologies, CDx has revolutionized the healthcare field and paved the way for more targeted and effective treatments.

One of the key advantages of companion diagnostics is the ability to enhance patient outcomes by identifying those individuals who are most likely to respond positively to a particular therapy. By analyzing biomarkers, genetic mutations, and other relevant factors, CDx can identify patients who would benefit from targeted therapies and avoid unnecessary treatments, thereby reducing healthcare costs and improving patient care.

Notable innovations in the companion diagnostics market have propelled its growth and importance in recent years. Advancements in genomics, next-generation sequencing, and molecular diagnostics have significantly contributed to the development of more accurate and efficient CDx tests. These innovations have allowed for better patient stratification and selection, leading to improved treatment outcomes and personalized therapies.

The companion diagnostics market has witnessed major investments from pharmaceutical companies and diagnostics manufacturers, recognizing the immense potential of CDx in their product development and services. As more therapies are being developed, pharmaceutical companies are incorporating companion diagnostics to identify suitable patients for their treatments, enhancing the efficiency of clinical trials and drug development processes.

The applications of companion diagnostics are diverse, with industries such as oncology, cardiovascular diseases, infectious diseases, and neurology investing heavily in this field. CDx has enabled oncologists to identify specific cancer subtypes, leading to tailored treatment plans and improved patient survival rates. In cardiovascular diseases, CDx has helped in the early detection of genetic markers for increased risk, allowing for preventive interventions and personalized medication.

Driving factors

Personalized Medicine: Revolutionizing Healthcare

Personalized medicine represents a paradigm shift from the traditional one-size-fits-all approach toward a patient-centric model. It recognizes that each patient's genetic composition is unique, resulting in varied responses to medication. Through the utilization of genetic testing and molecular profiling, personalized medicine aims to determine which treatment strategies are most likely to be effective for an individual patient.

The integration of genomic sequencing technologies has further propelled the progress of personalized medicine. Recent advancements in next-generation sequencing (NGS) have made it feasible to analyze a patient's entire genome within a reasonable timeframe and cost. This allows healthcare professionals to identify specific genetic alterations that drive a patient's disease and develop tailored treatment plans accordingly.

Cancer Therapies: Precision Medicine in Oncology

One of the primary areas where personalized medicine has made remarkable strides is in the field of oncology. Cancer is a complex disease characterized by genetic heterogeneity, meaning that no two tumors are identical. By leveraging the power of companion diagnostics, oncologists can identify the precise genetic mutations present in a patient's tumor and select targeted therapies to effectively combat the disease.

Immunotherapies have revolutionized cancer treatment by harnessing the body's immune system to fight cancer cells. Companion diagnostics play a crucial role in predicting a patient's response to immunotherapies, enabling healthcare professionals to tailor treatment plans and optimize outcomes.

Regulatory Support: Navigating the Path to Approval

The successful translation of personalized medicine and companion diagnostics into clinical practice heavily relies on robust regulatory frameworks and support. Regulatory agencies such as the Food and Drug Administration (FDA) in the United States and the European Medicines Agency (EMA) in Europe play a pivotal role in evaluating the safety and efficacy of these innovative technologies.

To ensure the reliability and accuracy of companion diagnostics, regulatory bodies have established stringent guidelines and requirements. These guidelines demand rigorous analytical validation, clinical validation, and evidence demonstrating the clinical utility of the companion diagnostic test. By adhering to these guidelines, manufacturers can obtain regulatory approvals that instill confidence in healthcare providers and patients alike. Next Generation Cancer Diagnostics revolutionizes Companion Diagnostics Market with precise, personalized therapy matching for effective cancer treatment approaches.

Restraining Factors

High Development Costs

Developing companion diagnostics involves a rigorous process of scientific research, clinical validation, and regulatory approvals. This extensive process requires significant financial resources, making it a major restraining factor for many companies and academic institutions. The high costs associated with developing companion diagnostics limit the number of organizations that can actively participate in this field.

To overcome this obstacle, it is crucial for governments, healthcare systems, and funding agencies to provide adequate financial support and incentives to promote companion diagnostics development. By reducing the financial burden, more organizations will be able to invest in research and development, leading to a wider range of innovative companion diagnostics options for patients and healthcare professionals.

Reimbursement Challenges

One of the key challenges in the adoption of companion diagnostics is the issue of reimbursement. As companion diagnostics are often used in conjunction with specific therapeutics, their reimbursement is linked to the reimbursement of the corresponding therapy. This creates challenges as reimbursement policies can vary between different healthcare systems and payers.

To ensure wider access to companion diagnostics, regulatory bodies and payers need to establish clear guidelines and reimbursement policies that recognize the value of these tests in improving patient outcomes. Collaboration between diagnostic developers, pharmaceutical companies, and healthcare systems is crucial in overcoming this challenge and advocating for fair reimbursement policies that take into account the benefits of companion diagnostics.

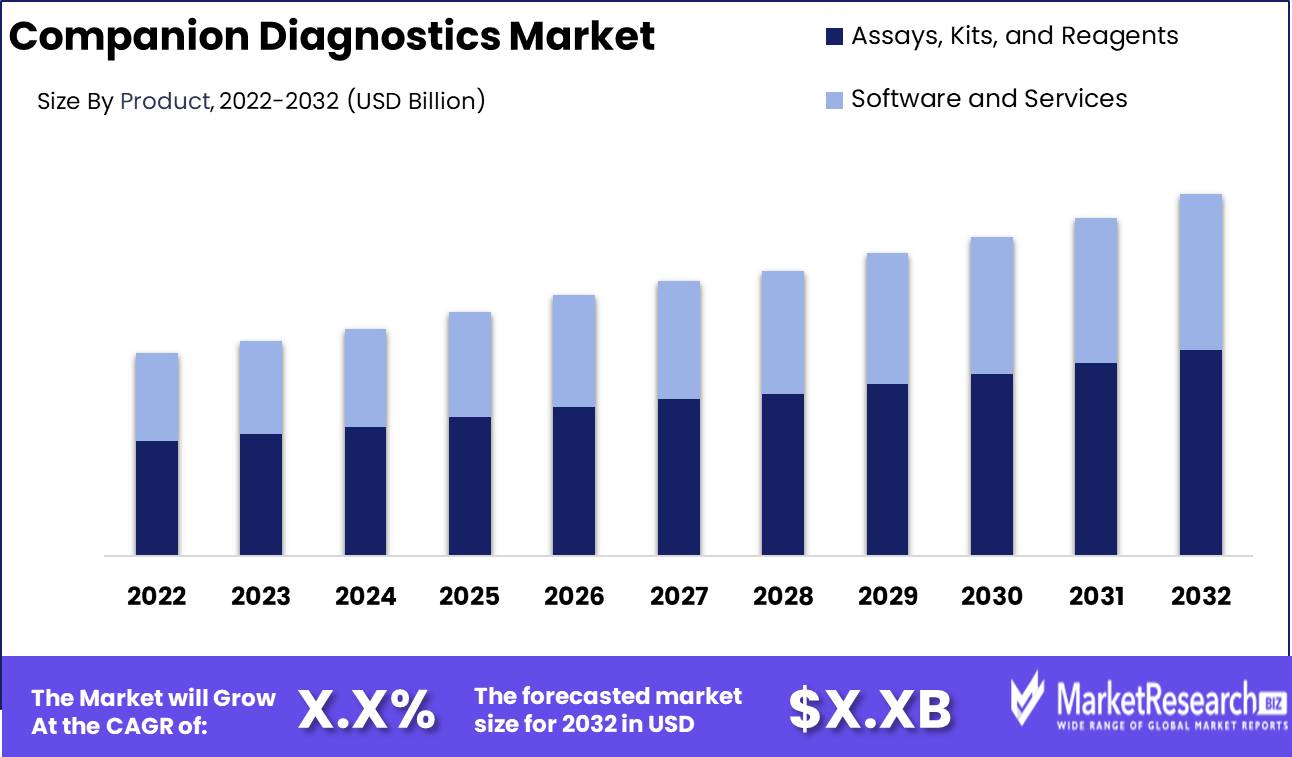

By Product Analysis

The companion diagnostics market is dominated by the Assays, Kits, and Reagents segment. This segment accounted for the largest revenue share in 2022, driven by the high demand for companion diagnostic assays and kits to identify patients who are eligible for targeted therapies. Key growth factors for assays, kits, and reagents include the continued development of targeted cancer therapies, partnerships between pharmaceutical and diagnostics companies, and the need for improved patient stratification.

This segment is expected to continue dominating the companion diagnostics market through 2032, as more assays and kits are developed alongside emerging precision medicines. Overall, the high clinical utility and recurrent use of assays and kits will sustain the dominant position of this segment in the companion diagnostics market.

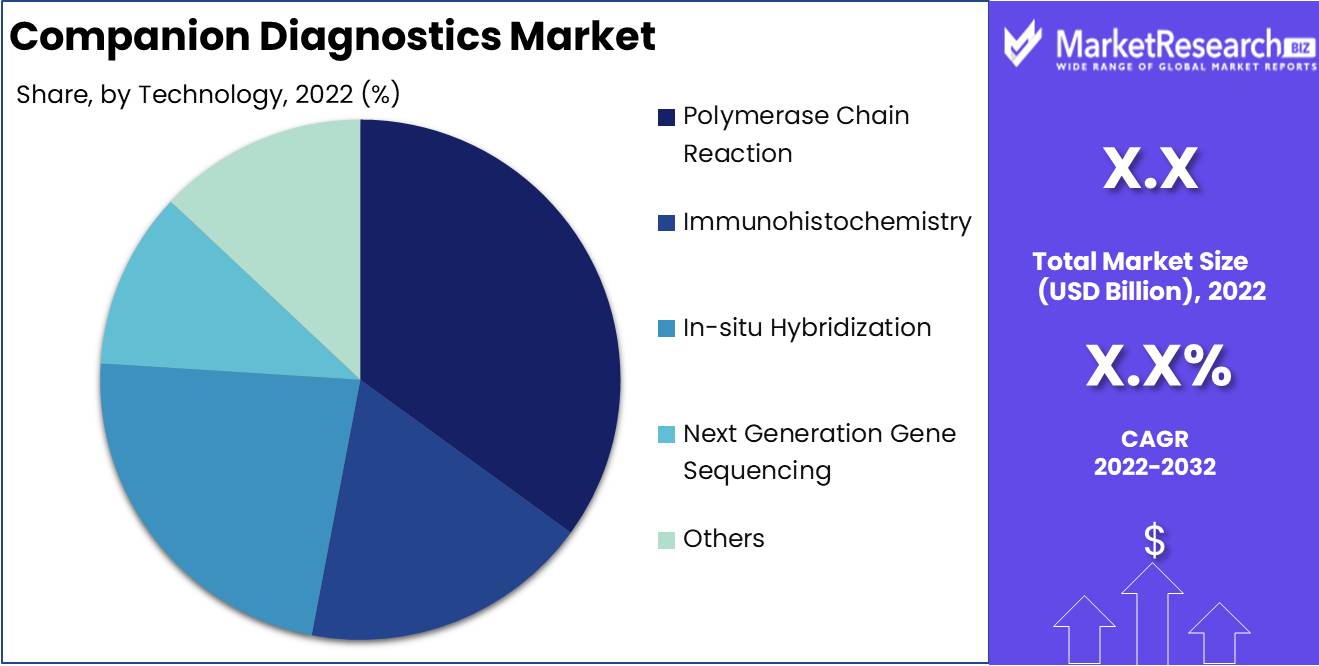

Technology Analysis

The Polymerase Chain Reaction (PCR) technology segment dominates the companion diagnostics market. This segment held the largest revenue share in 2022, attributable to PCR's speed, sensitivity and specificity for biomarker analysis. PCR-based tests enable effective patient screening and treatment selection for targeted therapies. Key growth drivers for the PCR segment include its growing utilization in liquid biopsy assays and genomic biomarker analysis.

Additionally, investments by companies to develop innovative PCR instruments, reagents, and assays for companion diagnostics are fueling growth. Going forward, continuous advances in PCR technology and its integration into next-generation sequencing workflows will ensure this segment remains dominant in the global companion diagnostics market through 2032. Overall, PCR’s operational simplicity and accurate results position it as an ideal technology for companion diagnostic testing.

Indication Analysis

The cancer indication segment dominates the global companion diagnostics market. This segment held the largest revenue share in 2022, driven by the high demand for companion diagnostics in cancer care. Companion diagnostics are widely used in cancer for biomarker testing to identify patients eligible for targeted therapies. Key growth drivers for the cancer segment include the rising prevalence of cancer, new product launches, and increased research on biomarkers.

Additionally, the high number of targeted cancer therapies awaiting companion diagnostics continues to propel segment growth. From now on, the cancer segment is poised to dominate the companion diagnostics market through 2032, fueled by the personalized medicine trend and need for effective patient stratification. Overall, companion diagnostics are becoming an integral part of cancer treatment, cementing this segment's leading position in the market.

Key Market Segments

By Product

- Assays, Kits, and Reagents

- Software and Services

By Technology

- Polymerase Chain Reaction

- Immunohistochemistry

- In-situ Hybridization

- Next Generation Gene Sequencing

- Others

By Indication

- Cancer

- Lung Cancer

- Breast Cancer

- Blood Cancer

- Colorectal Cancer

- Other Cancer Types

- Neurological Disorders

- Cardiovascular Diseases

- Infectious Diseases

- Other Indications

By End User

- Pharmaceutical and Biopharmaceutical Companies

- Reference Laboratories

- CROs

- Others

Growth Opportunity

Rising prevalence of cancer and other diseases

The increasing prevalence of various diseases like cancer, neurological disorders, and infectious diseases is driving growth in the companion diagnostics market. As more patients are diagnosed, the demand grows for companion diagnostic tests that can help guide targeted treatments based on the molecular profile of patients' diseases. This growth is further fueled by the aging population which leads to higher disease incidence.

Advances in genomic profiling and biomarkers

Technological advances in genomic profiling, biomarker discovery, and personalized medicine are propelling growth in the companion diagnostics market. The ability to identify specific biomarkers and correlate them with disease progression, drug response, and patient outcomes allows companion diagnostics to provide more accurate and effective guidance for treatment options for patients. The growth of genomic sequencing also aids in biomarker discovery.

Higher adoption of targeted therapies

The rising development and use of targeted cancer therapies and other targeted treatments is a key driver. As targeted therapies require biomarker testing to identify the right patient population, the demand for companion diagnostics essential for guiding therapy decisions increases in parallel. Regulatory policies supporting the co-development of drugs and companion diagnostics also drive adoption.

Latest Trends

Growing partnerships

There is an increasing trend of pharmaceutical and biotech companies partnering with diagnostic companies to co-develop companion diagnostic tests for their therapeutic drugs and treatments. These collaborations allow pharmaceutical companies to extend their expertise into diagnostics to identify the right patient populations for their therapies. For diagnostic companies, it helps drive demand for their offerings.

Advancements in next-generation sequencing

Next-generation sequencing (NGS) is being increasingly adopted in companion diagnostics to enable genomic profiling of tumors and the identification of biomarkers that can guide therapy decisions. NGS provides highly sensitive and comprehensive genomic data that can uncover multiple biomarkers compared to single biomarker tests. The declining costs and rapid turnaround time of NGS-based tests are also driving this trend.

Development of liquid biopsy-based tests

Liquid biopsies utilizing blood samples are an emerging trend in companion diagnostics compared to traditional tissue biopsies. Liquid biopsies are minimally invasive, provide real-time data on tumor evolution, and enable regular monitoring. Advances in circulating tumor DNA and circulating tumor cell analysis are driving liquid biopsy adoption in companion diagnostic testing for cancer.

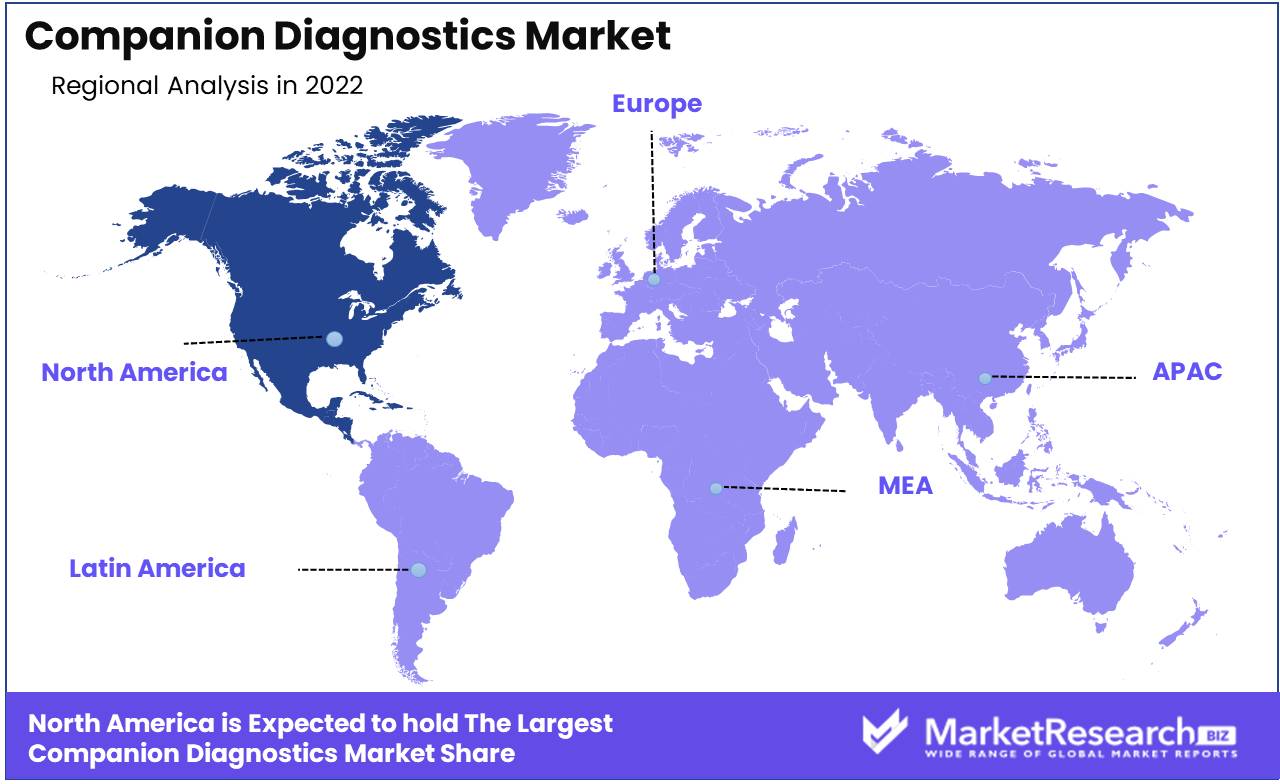

Regional Analysis

North America, particularly the United States, dominates the global companion diagnostics market. This can be attributed to several factors. Firstly, high cancer prevalence in the region coupled with favorable reimbursement policies is driving demand for targeted cancer therapies and associated companion diagnostic tests. Secondly, developed healthcare infrastructure, and presence of leading diagnostics companies like ThermoFisher, Illumina, Roche, etc along with advanced research capabilities support early adoption of novel companion diagnostics.

Moreover, strict FDA regulatory landscape, though challenging, instills confidence in companion diagnostic tests that receive simultaneous FDA drug-diagnostic approval. This is catalyzing partnerships between drug and diagnostics companies. Additionally, higher per capita healthcare expenditure compared to other regions enables payers and patients to adopt cutting-edge but expensive companion diagnostics. Lastly, rising utilization of next-generation sequencing and liquid biopsies in the U.S. is supporting the adoption of advanced companion diagnostic solutions.

North America will likely maintain market leadership, though the Asia Pacific region may expand at a higher growth rate owing to improving healthcare access and a growing middle-class population. Overall, conducive healthcare policies and rapid uptake of precision oncology in the U.S. make North America the dominant companion diagnostics market.

Key Regions and Countries

North America

- US

- Canada

- Mexico

Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

F. Hoffman-La Roche is one of the leading players in the companion diagnostics market with a broad portfolio of companion diagnostic tests for cancers and other diseases. Its key strengths include its global footprint, extensive R&D capabilities, and wide range of FDA-approved companion diagnostic tests paired with Roche's drugs like Herceptin, Perjeta, Zelboraf etc. Strategic acquisitions like Foundation Medicine and TIB Molbiol have expanded Roche's capabilities in genomic profiling and molecular assays.

Agilent Technologies holds a leading position in companion diagnostics with strength in genomic and proteomic platforms like microarrays, FISH, CISH, IHC etc. Its key focus areas are companion diagnostics for cancers, neurological disorders and infectious diseases. Strategic partnerships with pharmaceutical companies are a key driver of Agilent's growth.

QIAGEN is a leading player in sample preparation, assay technologies and bioinformatics for companion diagnostics. Its portfolio includes regulatory-approved companion diagnostic tests for cancers paired with therapies like Tykerb, Iressa etc. Collaborations with pharma companies like Amgen, Loxo Oncology, and Pfizer drive co-development of innovative companion diagnostics using QIAGEN's QCI bioinformatics solutions.

Top Key Players in Companion Diagnostics Market

- F. Hoffman-La Roche

- Agilent Technologies

- QIAGEN

- Thermo Fisher Scientific

- Illumina

- Abbott

- bioMérieux

- Myriad Genetics

- Sysmex Corporation

- Danaher

Recent Development

- In September 2022, Illumina announced the launch of its in vitro diagnostic (IVD) marked TruSight Oncology Comprehensive (EU) testing kit. This liquid biopsy test aids in treatment selection and monitoring for cancer patients by detecting key biomarkers.

- In August 2022, the FDA granted premarket approval for Foundation Medicine's FoundationOne CDx and companion diagnostic claims for Vitrakvi. This expands the panel's approved biomarker coverage for NSCLC patients.

- In June 2022, the FDA approved Guardant Health's Guardant360 CDx liquid biopsy test as a companion diagnostic to identify NSCLC patients for Amgen's Lumakras treatment. This was the first liquid biopsy CDx approval for a tissue-agnostic indication.

Report Scope

Report Features Description Market Value (2022) USD XX Forecast Revenue (2032) USD XX CAGR (2023-2032) XX% Base Year for Estimation 2022 Historic Period 2016-2022 Forecast Period 2023-2032 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product(Assays, Kits, and Reagents, Software and Services), By Technology(Polymerase Chain Reaction, Immunohistochemistry, Others), By Indication(Cancer, Neurological Disorders, Other) Regional Analysis North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape F. Hoffman-La Roche, Agilent Technologies, QIAGEN, Thermo Fisher Scientific, Illumina, Abbott, bioMérieux, Myriad Genetics, Sysmex Corporation, Danaher Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

Our Clients

View Our Licence Options