Acetic Acid Market By application (Acetic anhydride, Vinyl acetate monomer (VAM)), By end-use industry (Paints and coating, Pharmaceutical, Others), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2023-2032

-

6325

-

May 2023

-

150

-

-

This report was compiled by Correspondence Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Report Overview

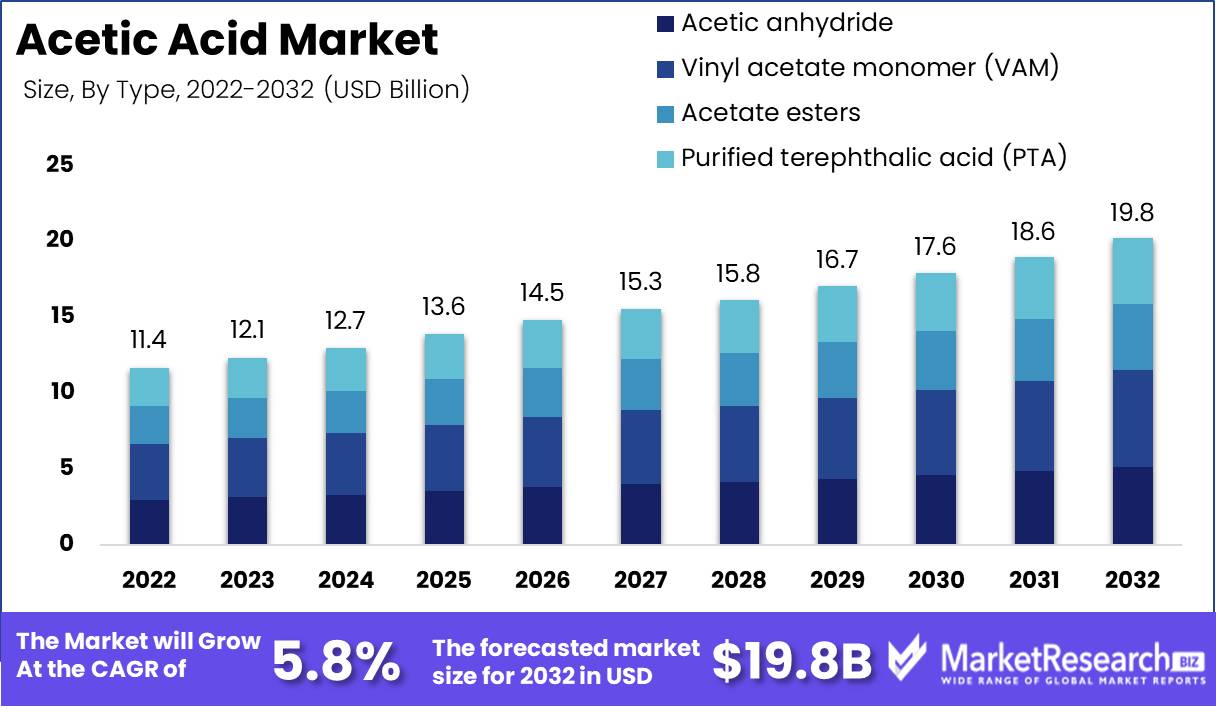

Acetic Acid Market size is expected to be worth around USD 19.8 Bn by 2032 from USD 11.4 Bn in 2022, growing at a CAGR of 5.8% during the forecast period from 2023 to 2032.

Acetic acid, also known as ethanoic acid, is an organic substance that has a pungent odor and an acidic flavor. It is a transparent liquid that is soluble in water, making it a versatile industrial chemical extensively used in a variety of industries, such as the food, textile, and paint and adhesives industries. Through a carbonylation procedure, acetic acid is primarily produced from methanol.

The adaptability of Acetic Acid makes it an indispensable component in numerous products and services. Its value derives from its chemical properties, which confer a variety of benefits, including being an outstanding solvent, disinfectant, and food preservative. Vinegar, plastics, and textiles are all produced using Acetic Acid as a raw material.

China was the largest exporter of acetic acid in 2021, with exports totaling approximately $819.22 billion USD. The United States followed as the second-largest exporter with exports worth approximately $542.27 billion USD.

With companies investing significantly in research and development, the Acetic Acid market has seen numerous innovations in recent years. The development of highly efficient and sustainable production methods, such as Bioreactor technology, which uses renewable sources such as plant refuse to produce Acetic Acid, is a notable innovation.

Acetic Acid raises ethical issues that must be addressed, just like any chemical compound. The main concern is the potential for environmental contamination, which results from severe and unsustainable production methods. To address these concerns, companies in the Acetic Acid market are emphasizing transparency, explainability, and accountability to ensure the production and use of Acetic Acid in a responsible manner.

Driving factors

Multiple Demand Drives Expansion

Acetic Acid Market experiences rapid expansion due to a variety of factors. The escalating demand for vinyl acetate monomer and purified terephthalic acid, for which acetic acid is a crucial raw material, is a key factor driving the market. The extensive use of these chemicals in industries such as automotive, electronics, and construction contributes to the expansion of the market.

The food and beverage industry contributes significantly to market expansion. Acetic acid must be used as a preservative and flavoring agent due to the increased demand for processed and packaged food products. Acetic acid remains indispensable in this industry for extending shelf life and enhancing flavor characteristics in foods such as pickles, condiments, and dressings.

Textile Industry Encourages Synthetic Fiber Production

Acetic acid is widely used in the textile industry, especially in the production of acetate fibers. These fibers are used for a variety of purposes, including garments, household furnishings, and surgical dressings. As the demand for synthetic fibers continues to rise, the reliance on acetic acid as a vital component increases, thereby contributing to the growth of the acetic acid market.

Flexible Applications Drive Market Expansion

The production of paints, coatings, and adhesives in numerous industries contributes to the demand for acetic acid. As a solvent, acetic acid is essential to these production processes. The automotive, construction, and furniture industries, among others, benefit from the superior bonding properties of acetic acid-based adhesives, which contributes to the expansion of the market.

Environmental Consciousness and Technological Progress

Acetic Acid Market is affected by altering regulations, environmental concerns, and technological progress. Due to acetic acid's potential environmental impact, regulatory bodies impose stringent regulations that emphasize the need for sustainable practices. Emerging technologies, innovative production methods, and enhanced catalysts simultaneously bring about transformative changes. In order to maintain a competitive edge and capitalize on the expanding demand for eco-friendly and sustainable alternatives, market participants must adjust to these shifting landscapes.

Restraining Factors

Health risks handling and exposure

Acetic acid, despite being a necessary component in many industries, can be harmful if not handled properly. Acetic acid produces corrosive vapors that can irritate the eyes, skin, and respiratory system. High concentrations can result in severe burns, lung injury, and even mortality. Industries that utilize acetic acid must take the necessary safety precautions and ensure that their employees are properly trained in its safe management.

Fluctuations in the prices of primary materials

Acetic acid is predominantly produced using methanol, which is derived from coal or natural gas. Any volatility in the prices of coal or natural gas can have a substantial effect on the cost of producing acetic acid. Moreover, supply chain disruptions can result in shortages and price increases. Consequently, fluctuations in the cost of basic materials have an immediate impact on the price of acetic acid.

Strict Regulations Govern the Use

As a preservative and flavoring agent, acetic acid is used extensively in the food and beverage industry. However, governments worldwide have imposed stringent restrictions on the use of acetic acid in food and drink products. The purpose of these regulations is to ensure that the use of acetic acid poses no health hazards to consumers. The stringent regulations could result in a decline in the food and beverage industry's demand for acetic acid.

Economic Downturns Reduce Demand for Products

During economic downturns, the demand for most products, including those that use acetic acid, typically decreases. As industries reduce their operations, they require fewer basic materials, which reduces the demand for acetic acid. The effects of economic recessions can be severe and long-lasting, resulting in a decline in acetic acid demand.

Application Analysis

Vinyl Acetate Monomer Segment Dominates Market for Acetic Acid. The vinyl acetate monomer segment currently dominates the Acetic Acid Market and is expected to do so for the foreseeable future. Vinyl acetate monomer (VAM) serves as a building block for numerous polymers, resins, and other chemical products. PVC, PVA, and PVAc are among the most widely used VAM-based products. It is the monomer of polyvinyl acetate. The segment's dominance can be attributed to the VAM's distinctive properties, such as superior adhesive strength, flexibility, and water resistance, which make it suitable for a wide range of end-use applications.

It is also now widely used as barrier resins for plastic bottles. The consumer trend toward eco-friendly products also drives the demand for VAM-based products, which are generally regarded as environmentally favorable. The VAM segment is anticipated to experience the highest growth rate over the next few years due to its increasing demand in a variety of end-use industries, including construction, packaging industry, and automotive. The expanding use of VAM-based products in emerging economies is anticipated to fuel the market's expansion.

End-User Industry Analysis

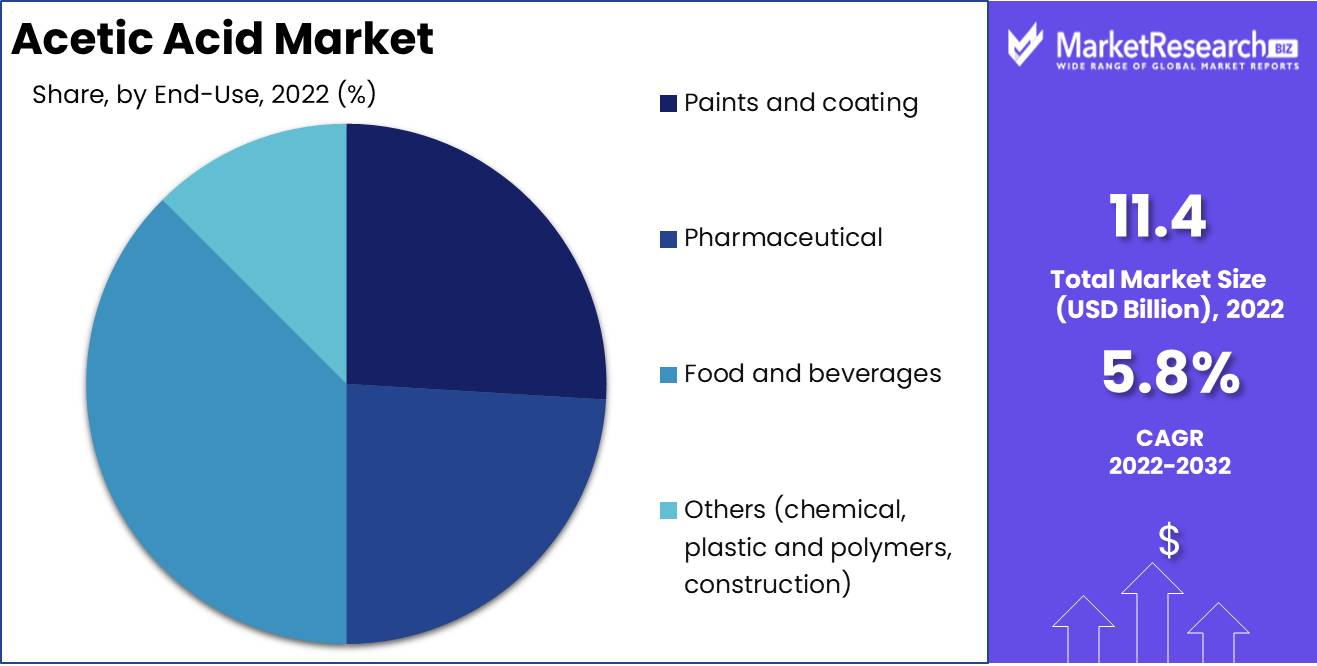

Acetic Acid Market Dominates Food and Beverage Segment. Because of its expanding use in the food and beverage industry, the food and beverage segment dominates the Acetic Acid Market. Vinegar, which is extensively utilized in the food and beverage industry, is produced using acetic acid. In recent years, the use of vinegar in cookery and salad dressing has contributed significantly to the expansion of the vinegar market. The demand for acetic acid is anticipated to remain driven by the food and beverage industry.

The increasing use of vinegar and other acetic acid-based products in the food and beverage industry is a result of rising health concerns and the growing preference for natural and organic food options among consumers. It is anticipated that the trend toward natural products in the food and beverage industry will continue to drive demand for acetic acid. Due to the increasing use of vinegar in cooking and salad dressing, as well as the rising demand for processed foods, sauces, and condiments, it is anticipated that the food and beverage segment of the Acetic Acid Market will grow at the quickest rate over the next few years.

Key Market Segments

By Application

- Acetic anhydride

- Vinyl acetate monomer (VAM)

- Acetate esters

- Purified terephthalic acid (PTA)

By End-Use industry

- Paints and coating

- Pharmaceutical

- Food and beverages

- Others (chemical, plastic and polymers, construction)

Growth Opportunity

Biodegradable Materials in High Demand

Bio-based acetic acid is a sustainable alternative to conventional acetic acid, which is derived from crude oil. Produced from renewable resources such as biomass, bio-based acetic acid is a sustainable alternative for industries requiring significant quantities of acetic acid.

The rising demand for bio-based acetic acid is driven by a number of factors, including rising environmental concerns, stricter regulations, and a growing consumer preference for environmentally responsible products. In the future years, it is anticipated that the use of acetic acid derived from renewable sources will increase as more industries adopt environmentally friendly production methods.

Demand in the Pharmaceutical Industry Is Growing

One of the main end-users of acetic acid is the pharmaceutical industry, which uses it in the production of various medications and medicines. Acetic acid is used to make aspirin, one of the most popular medications in the world. Acetic acid is also used to make a variety of antibiotics, analgesics, and sedatives.

In the future years, the pharmaceutical industry's demand for acetic acid is projected to increase as the global population continues to age, resulting in a greater demand for drugs and remedies. In addition, the expansion of the biotechnology industry is anticipated to increase demand for acetic acid, which is utilized in bioprocessing.

Increasing Quantity for the Production

Vinyl acetate monomer, ethyl acetate, and butyl acetate are just a few examples of the solvents and chemical intermediates that are made using acetic acid. These chemicals are utilized in a number of industries, including paints and coatings, textiles, and packaging.

In the coming years, the demand for solvents and chemical intermediates is anticipated to increase due to factors such as the expansion of the manufacturing sector, the rising demand for consumer products, and the rising demand for specialty chemicals. It is anticipated that this will increase the demand for acetic acid in the production of these compounds.

Production of Polyester Fibers Is Rising

Purified terephthalic acid (PTA) is a key basic material for the production of polyester fibers, which are extensively used in textiles, packaging, and automotive applications. Acetic acid is required for the production of PTA, so there is a strong correlation between the demand for acetic acid and the demand for PTA.

In the coming years, the global demand for polyester fibers is anticipated to increase due to factors such as the rising demand for textiles, increasing urbanization, and consumer preferences for eco-friendly products. This is anticipated to increase demand for PTA, and consequently, acetic acid.

Latest Trends

Adopting Eco-Friendly Substitutes

Acetic Acid Market is experiencing a rising tide of bio-based acetic acid adoption due to its eco-friendly properties. Produced through the fermentation of biomass, this environmentally friendly alternative reduces greenhouse gas emissions and makes use of renewable resources. Increasing environmental concerns drive the adoption and demand for bio-based acetic acid, thereby reshaping the market environment.

Pharmaceutical and Agrochemical Industries

With acetic acid serving as a vital precursor, the pharmaceutical and agrochemical industries become significant consumers. Acetic acid becomes indispensable in these industries for synthesizing acetate esters, such as cellulose acetate. As demand for pharmaceutical and agrochemical products continues to rise, reliance on acetic acid increases, driving market growth.

Construction Industry's Adhesive and Sealant Demand Boosts

The accelerated expansion of the construction industry, fuelled by urbanization and industrialization, generates a significant demand for adhesives and sealants. Acetic acid is a crucial component of the production of these indispensable building materials. As the construction industry grows, it is anticipated that the demand for acetic acid in adhesive and sealant production will increase significantly.

Coatings and Paints

The increasing demand for coatings and paints drives the production of acetic acid. The manufacturing of emulsion polymers requires the incorporation of acetic acid into vinyl acetate monomers (VAM). These polymers, which are derived from VAM, are essential components of paints and coatings. The demand for acetic acid is fueled by the rising demand for coatings and paints in various industries.

Growing Demand for Acetate Esters

The rising demand for acetate esters drives a surge in demand for acetic acid on the market. These esters, which are derived from acetic acid, are used to produce aromas, fragrances, and solvents. The rapid growth of the food and beverage industry and the rising demand for high-quality fragrances contribute considerably to the expansion of the market.

Regional Analysis

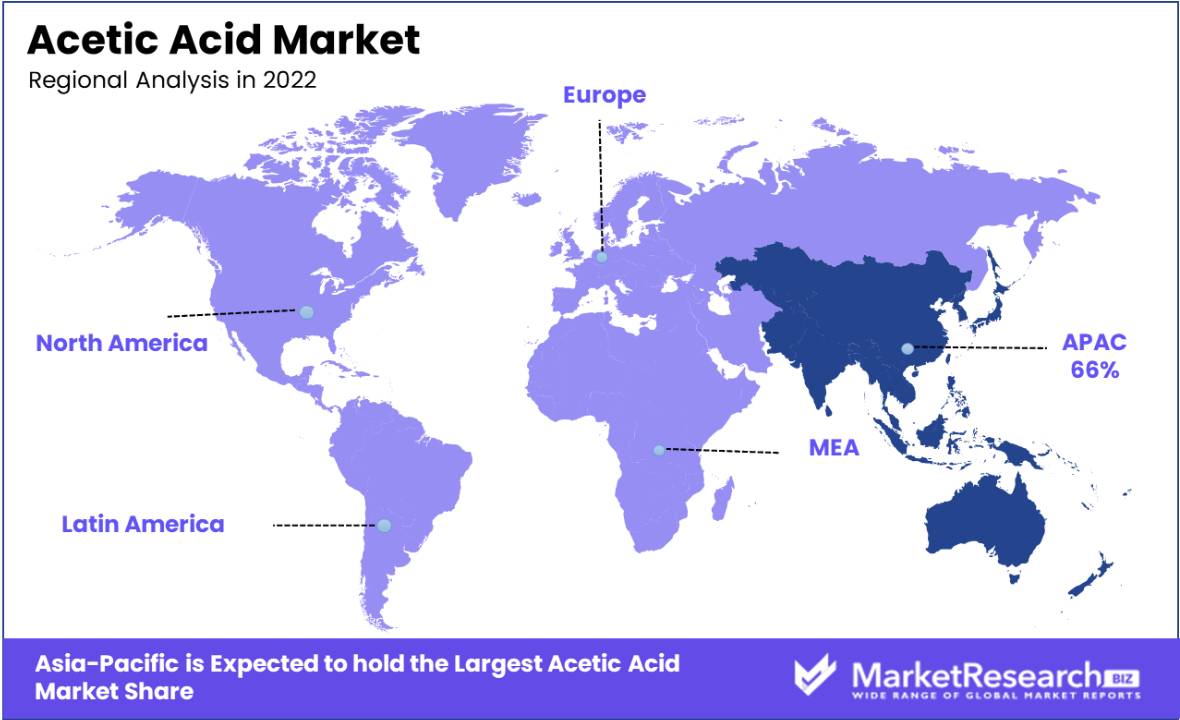

Asia Pacific dominates the global acetic acid market, constituting over 66% of the total consumption in 2022, driven by its robust industrial infrastructure and expanding population. Within the region, China leads as the largest acetic acid consumer, followed closely by India and Japan.

Asia-Pacific region boasts the world's largest population, amplifying the demand for products such as food and beverages, textiles, and more, which heavily rely on acetic acid in their production processes. Notable trends include a shift toward renewable feedstocks for acetic acid production, moving away from petroleum-based sources due to rising costs and environmental concerns, as well as a surging demand in emerging economies like China and India, attributed to their rapid economic development and subsequent need for acetic acid across various sectors.

The key players in this dynamic Asia-Pacific market encompass industry leaders such as Celanese Corporation, Jiangsu SOPO (Group) Co., Ltd., Yankuang Group, SABIC, and Mitsubishi Chemical Corporation. These market leaders are actively investing in expanding production capacities to meet the surging demand within the region.

Europe is the second-largest consumer of acetic acid after Asia Pacific. In 2022, Europe accounted for over 20% of global acetic acid consumption. The major consumers of acetic acid in Europe include Germany, the United Kingdom, and France. North America is the third-largest consumer of acetic acid after Asia Pacific and Europe. In 2022, North America accounted for over 10% of global acetic acid consumption. The major consumers of acetic acid in North America include the United States and Canada.

Key Regions and Countries

North America

- US

- Canada

- Mexico

Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

In the coming years, the global acetic acid market is anticipated to exhibit a stable growth rate, with key players dominating in terms of market share and revenue generation. It is anticipated that the dominant players in this market will maintain their position by implementing strategies such as mergers and acquisitions, expanding their product portfolios, and concentrating on developing new applications for acetic acid.

Celanese Corporation, a multinational technology and specialty materials corporation, is one of the market leaders in acetic acid. The company offers a variety of acetic acid products, such as VAM and glacial acetic acid, and is renowned for its commitment to innovation and environmentally responsible business practices.

BP Chemicals Ltd., a leading provider of acetic acid and related chemicals, is another major player in the acetic acid market. Acetic acid produced by the company is utilized in numerous industries, including textiles, plastics, and pharmaceuticals.

On the acetic acid market, LyondellBasell Industries N.V., Jiangsu Sopo Chemical Co., Ltd., and PetroChina Company Limited are also notable competitors. It is anticipated that these companies will continue to dominate the market in the coming years, contributing to the robust expansion of the global acetic acid market.

Top Key Players in Acetic Acid Market

- Celanese Corporation

- British Petroleum p.l.c.

- Jiangsu Sopo (Group) Co., Ltd.

- Eastman Chemical Company

- Sinopec Ningbo Engineering Co., Ltd.

- LyondellBasell Acetyls, LLC

- DuPont

- BASF S.E.

- PetroChina Company Limited

- Mitsubishi Chemical Corporation

- Daicel Corporation

- Shanghai Huayi (Group) Company

- Airedale Chemical Company Limited

- Kingboard Chemical Holdings Ltd.

- Shandong Hualu-Hengsheng Chemical Co. Ltd.

- HELM AG

Recent Development

- In March 2023, KBR, a US multinational engineering group, made a significant move by acquiring the Acetica technology for an undisclosed sum. Acetica, originally developed by Japan's Chiyoda, is a carbonylation technology that utilizes methanol and carbon monoxide to produce acetic acid. This aligns with the global push towards carbon capture and utilization to mitigate climate change.

- In May 2023, Sekab launched an expanded production of bio-based acetic acid, a crucial component in various industries. The company's investment in new production capacity is now operational, allowing for faster and larger deliveries, reducing carbon footprint by 50%

- In May 2023, Chemical engineers at Monash University have pioneered an industrial process for producing acetic acid that utilizes excess carbon dioxide (CO2) from the atmosphere. This groundbreaking method has the potential to achieve negative carbon emissions. The research, published in Nature Communications, introduces a novel solid catalyst made from a material called metal organic framework (MOF)

- In May 2023, Celanese, a US-based acetyls and engineered materials producer, has announced the mechanical completion of a new acetic acid plant in Clear Lake, Texas. This state-of-the-art facility has a production capacity of 1.3 million tonnes per year. The new plant's strategic location in the US will allow Celanese to capitalize on the low natural gas costs in the region.

Report Scope

Report Features Description Market Value (2022) USD 11.44 Bn Forecast Revenue (2032) USD 19.8 Bn CAGR (2023-2032) 5.8% Base Year for Estimation 2022 Historic Period 2016-2022 Forecast Period 2023-2032 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By application (Acetic anhydride, Vinyl acetate monomer (VAM), Acetate esters, Purified terephthalic acid (PTA))

By end-use industry (Paints and coating, Pharmaceutical, Food and beverages, Others (chemical, plastic and polymers, construction))Regional Analysis North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Celanese Corporation, British Petroleum p.l.c., Jiangsu Sopo (Group) Co., Ltd., Eastman Chemical Company, Sinopec Ningbo Engineering Co., Ltd., LyondellBasell Acetyls, LLC, DuPont, BASF S.E., PetroChina Company Limited, Mitsubishi Chemical Corporation, Daicel Corporation, Shanghai Huayi (Group) Company, Airedale Chemical Company Limited, Kingboard Chemical Holdings Ltd., Shandong Hualu-Hengsheng Chemical Co. Ltd., HELM AG. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Celanese Corporation

- British Petroleum p.l.c.

- Jiangsu Sopo (Group) Co., Ltd.

- Eastman Chemical Company

- Sinopec Ningbo Engineering Co., Ltd.

- LyondellBasell Acetyls, LLC

- DuPont

- BASF S.E.

- PetroChina Company Limited

- Mitsubishi Chemical Corporation

- Daicel Corporation

- Shanghai Huayi (Group) Company

- Airedale Chemical Company Limited

- Kingboard Chemical Holdings Ltd.

- Shandong Hualu-Hengsheng Chemical Co. Ltd.

- HELM AG

Our Clients

View Our Licence Options